5 Cents – Canada

Circulating commemorative coins

Commemoration: Supporting the war effort

Canada

Context

Material

Diameter: 21.23 mm

Weight: 4.54 g

Thickness: 1.7 mm

Shape: Dodecagonal

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #Click to copy to clipboard40

Numista: #411

Value

Exchange value: 0.05 CAD = $0.04

Inflation-adjusted value: 0.92 CAD

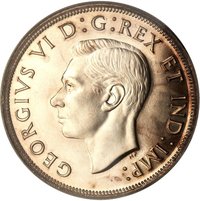

Obverse

Description:

King George VI left-facing portrait.

Inscription:

GEORGIVS VI D:G:REX ET IND:IMP:

HP

HP

Translation:

George VI by the Grace of God King and Emperor of India.

Script: Latin

Language: Latin

Engraver: Thomas Shingles

Designer: Thomas Humphrey Paget

Reverse

Description:

This design promotes the war effort with a central "V" for victory and value, flanked by maple leaves and a torch. It includes the year and country name, with a Morse code message around the rim.

Inscription:

CANADA

19 V 43

CENTS

T.S

.-- . .-- .. -. .-- .... . -. .-- . .-- --- .-. -.- .-- .. .-.. .-.. .. -. --. .-.. -.--

19 V 43

CENTS

T.S

.-- . .-- .. -. .-- .... . -. .-- . .-- --- .-. -.- .-- .. .-.. .-.. .. -. --. .-.. -.--

Translation:

CANADA

19 V 43

CENTS

T.S

WE WIN WHEN WE WORK WILLINGLY

19 V 43

CENTS

T.S

WE WIN WHEN WE WORK WILLINGLY

Languages: English, Morse Code

Designer: Thomas Shingles

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Royal Canadian Mint of Ottawa | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1943 | — | 24,760,256 | ||

| 1944 | — | 8,000 |

Historical background

In 1943, Canada's currency situation was fundamentally shaped by the exigencies of the Second World War. The nation was operating under a system of fixed exchange rate control, established at the outbreak of hostilities in 1939. The Canadian dollar was pegged at a rate of $1.10 Canadian to $1.00 U.S., a deliberate devaluation from parity to conserve U.S. dollar reserves, control capital flight, and prioritize the financing of the war effort. This "wartime peg" was managed by the Foreign Exchange Control Board (FECB), which held a monopoly over all foreign currency transactions, strictly regulating the flow of capital in and out of the country to prevent speculation and ensure that every available U.S. dollar could be used to purchase essential American war materials.

Domestically, the financial landscape was characterized by aggressive government borrowing and the management of inflation. To fund the massive cost of the war, the federal government relied heavily on victory bond campaigns, war savings certificates, and direct borrowing from the Bank of Canada. While price and wage controls had been instituted in 1941 to curb inflation, 1943 saw ongoing pressures as high employment and government spending increased consumer demand amidst strict rationing of goods. The currency in circulation was stable but subject to the overarching control of federal authorities, with monetary policy entirely subordinated to the goal of maximizing wartime production and financial stability.

This controlled environment stood in contrast to the pre-war period and set the stage for post-war financial planning. The stability provided by the FECB and the fixed rate was seen as a necessary wartime measure, but debates were beginning to emerge about the appropriate exchange rate and financial controls for the post-war reconstruction era. The experiences of 1943—with its stringent controls, managed currency, and close economic integration with the Allied war effort—directly informed the decisions that would lead to Canada's participation in the Bretton Woods system and its eventual return to a floating exchange rate in 1950.

Domestically, the financial landscape was characterized by aggressive government borrowing and the management of inflation. To fund the massive cost of the war, the federal government relied heavily on victory bond campaigns, war savings certificates, and direct borrowing from the Bank of Canada. While price and wage controls had been instituted in 1941 to curb inflation, 1943 saw ongoing pressures as high employment and government spending increased consumer demand amidst strict rationing of goods. The currency in circulation was stable but subject to the overarching control of federal authorities, with monetary policy entirely subordinated to the goal of maximizing wartime production and financial stability.

This controlled environment stood in contrast to the pre-war period and set the stage for post-war financial planning. The stability provided by the FECB and the fixed rate was seen as a necessary wartime measure, but debates were beginning to emerge about the appropriate exchange rate and financial controls for the post-war reconstruction era. The experiences of 1943—with its stringent controls, managed currency, and close economic integration with the Allied war effort—directly informed the decisions that would lead to Canada's participation in the Bretton Woods system and its eventual return to a floating exchange rate in 1950.

🌱 Very Common