1 dollar (King George V) – Canada

Add to wishlist

Circulating commemorative coins

Commemoration: 25th Anniversary of the Reign of King George V

Canada

Context

Material

References

KM: #

Numista: #447

Value

Exchange value: 1 CAD

Bullion value: $45.42

Inflation-adjusted value: 22.43 CAD

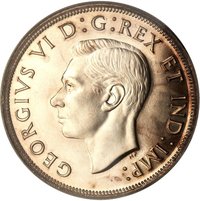

Obverse

Description:

King George V crowned, left-facing bust.

Inscription:

GEORGIVS V REX IMPERATOR ANNO REGNI XXV

Translation:

George V King Emperor In the Year of his Reign 25

Script: Latin

Language: Latin

Engraver: Percy Metcalfe

Reverse

Description:

A voyageur and an Aboriginal companion paddle a canoe with H.B. bundles, framed by the face value and "CANADA."

Inscription:

CANADA

1935

DOLLAR

EH

1935

DOLLAR

EH

Script: Latin

Engraver: Emanuel Otto Hahn

Edge

Milled

Categories

| Transportation> Watercraft |

Mints

| Name | Mark |

|---|---|

| Royal Canadian Mint of Ottawa | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1935 | — | 428,707 |

Historical background

In 1935, Canada’s currency situation was in a state of significant transition, deeply influenced by the lingering Great Depression. The nation was on the cusp of a major monetary shift: the creation of a central bank and a new, distinctly Canadian currency. Prior to this, Canada’s money was a complex patchwork of private bank notes issued by chartered banks, alongside Dominion notes issued by the federal government. This system, while functional, was seen as lacking central control, especially during the economic crisis when confidence in the banking system was fragile and exchange rates with other currencies, particularly the British pound and U.S. dollar, could be volatile.

The key development of the year was the passage of the Bank of Canada Act in July, establishing Canada’s first central bank. Its primary mandates were to regulate credit and currency, act as the government’s fiscal agent, and, crucially, "to mitigate by its influence fluctuations in the general level of production, trade, prices and employment." This was a direct response to the Depression’s deflationary spiral. Concurrently, the Currency, Mint and Exchange Fund Act was passed, authorizing the issuance of a new national currency to be issued by the new central bank, replacing the existing private and Dominion notes.

Therefore, by the end of 1935, the framework for a modern monetary system was in place, though the physical changes were yet to come. The Bank of Canada opened its doors in March 1935 as a privately owned institution (it would be nationalized in 1938), and the first series of "Bank of Canada" notes began circulating in 1935, initially alongside the old chartered bank notes, which were gradually retired. This move centralized monetary policy, provided greater stability, and was a definitive step in asserting Canada’s financial sovereignty as it moved away from a colonial-style currency system toward a managed, independent national currency.

The key development of the year was the passage of the Bank of Canada Act in July, establishing Canada’s first central bank. Its primary mandates were to regulate credit and currency, act as the government’s fiscal agent, and, crucially, "to mitigate by its influence fluctuations in the general level of production, trade, prices and employment." This was a direct response to the Depression’s deflationary spiral. Concurrently, the Currency, Mint and Exchange Fund Act was passed, authorizing the issuance of a new national currency to be issued by the new central bank, replacing the existing private and Dominion notes.

Therefore, by the end of 1935, the framework for a modern monetary system was in place, though the physical changes were yet to come. The Bank of Canada opened its doors in March 1935 as a privately owned institution (it would be nationalized in 1938), and the first series of "Bank of Canada" notes began circulating in 1935, initially alongside the old chartered bank notes, which were gradually retired. This move centralized monetary policy, provided greater stability, and was a definitive step in asserting Canada’s financial sovereignty as it moved away from a colonial-style currency system toward a managed, independent national currency.

🌱 Common