10 kroner (Universal Suffrage) – Norway

Add to wishlist

Circulating commemorative coins

Commemoration: 100th Anniversary of Universal Suffrage

Norway

Context

Material

References

KM: #

Numista: #44927

Value

Exchange value: 10 NOK

Inflation-adjusted value: 14.48 NOK

Obverse

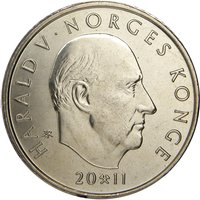

Description:

King Harald V bust facing right. Engraver's initials behind bust. Inscription surrounds. Date split by mintmark below. Solid rim ring.

Inscription:

HARALD V · NORGES KONGE

IAR

20 ⚒ 13

IAR

20 ⚒ 13

Translation:

Harald V, Norway's King

20th Anniversary

20 · 13

20th Anniversary

20 · 13

Script: Latin

Engraver: Ingrid Austlid Rise

Reverse

Description:

Four women pushing a large object. Inscription, value, and date at right. Designer's initials below. Solid ring on rim.

Inscription:

STEMMERETTSJUBILEET

KR 10

1913-2013

SD

KR 10

1913-2013

SD

Translation:

The Centenary of Women's Suffrage

10 Kroner

1913-2013

Sd

10 Kroner

1913-2013

Sd

Script: Latin

Language: Norwegian

Engraver: Ingrid Austlid Rise

Designer: Siri Dokken

Edge

Segmented reeding.

Categories

| Human rights |

Mints

| Name | Mark |

|---|---|

| Norwegian Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2013 | — | 2,025,111 | ||

| 2013 | — | 2,894 | Proof |

Historical background

In 2013, Norway's currency situation was dominated by the persistent strength of the Norwegian krone (NOK), a phenomenon often referred to as the "krone paradox." Despite historically low interest rates from Norges Bank, the central bank, the krone remained robust, trading at high levels against major currencies like the euro and the US dollar. This strength was fundamentally driven by Norway's strong economic position, fueled by high oil and gas prices, substantial foreign exchange reserves, and a sovereign wealth fund (the Government Pension Fund Global) that was the largest in the world. The country's AAA credit rating and fiscal stability made the krone a sought-after safe-haven currency.

This strong krone presented a significant challenge for Norway's non-oil export industries, particularly manufacturing, fisheries, and tourism. Companies in these sectors faced intense competitive pressure in international markets, as their goods and services became more expensive for foreign buyers. The situation sparked considerable debate between industry leaders, who called for intervention to weaken the currency, and the central bank, which emphasized its mandate for price stability. Norges Bank's main policy tool was the key policy rate, which it had cut to 1.5% by March 2013 in part to temper krone appreciation, but with limited effect.

Consequently, 2013 was a year of strategic patience and limited tools for Norwegian monetary authorities. Norges Bank explicitly stated it would not engage in direct currency intervention, relying instead on interest rate policy and verbal guidance. The bank's forward guidance in its monetary policy reports consistently signaled that rates would remain low for an extended period, a stance aimed at capping the krone's rise. The year ended with the currency strength largely unabated, underscoring the complex disconnect between domestic interest rate policy and a currency valuation overwhelmingly shaped by global hydrocarbon markets and macroeconomic stability.

This strong krone presented a significant challenge for Norway's non-oil export industries, particularly manufacturing, fisheries, and tourism. Companies in these sectors faced intense competitive pressure in international markets, as their goods and services became more expensive for foreign buyers. The situation sparked considerable debate between industry leaders, who called for intervention to weaken the currency, and the central bank, which emphasized its mandate for price stability. Norges Bank's main policy tool was the key policy rate, which it had cut to 1.5% by March 2013 in part to temper krone appreciation, but with limited effect.

Consequently, 2013 was a year of strategic patience and limited tools for Norwegian monetary authorities. Norges Bank explicitly stated it would not engage in direct currency intervention, relying instead on interest rate policy and verbal guidance. The bank's forward guidance in its monetary policy reports consistently signaled that rates would remain low for an extended period, a stance aimed at capping the krone's rise. The year ended with the currency strength largely unabated, underscoring the complex disconnect between domestic interest rate policy and a currency valuation overwhelmingly shaped by global hydrocarbon markets and macroeconomic stability.

🌱 Common