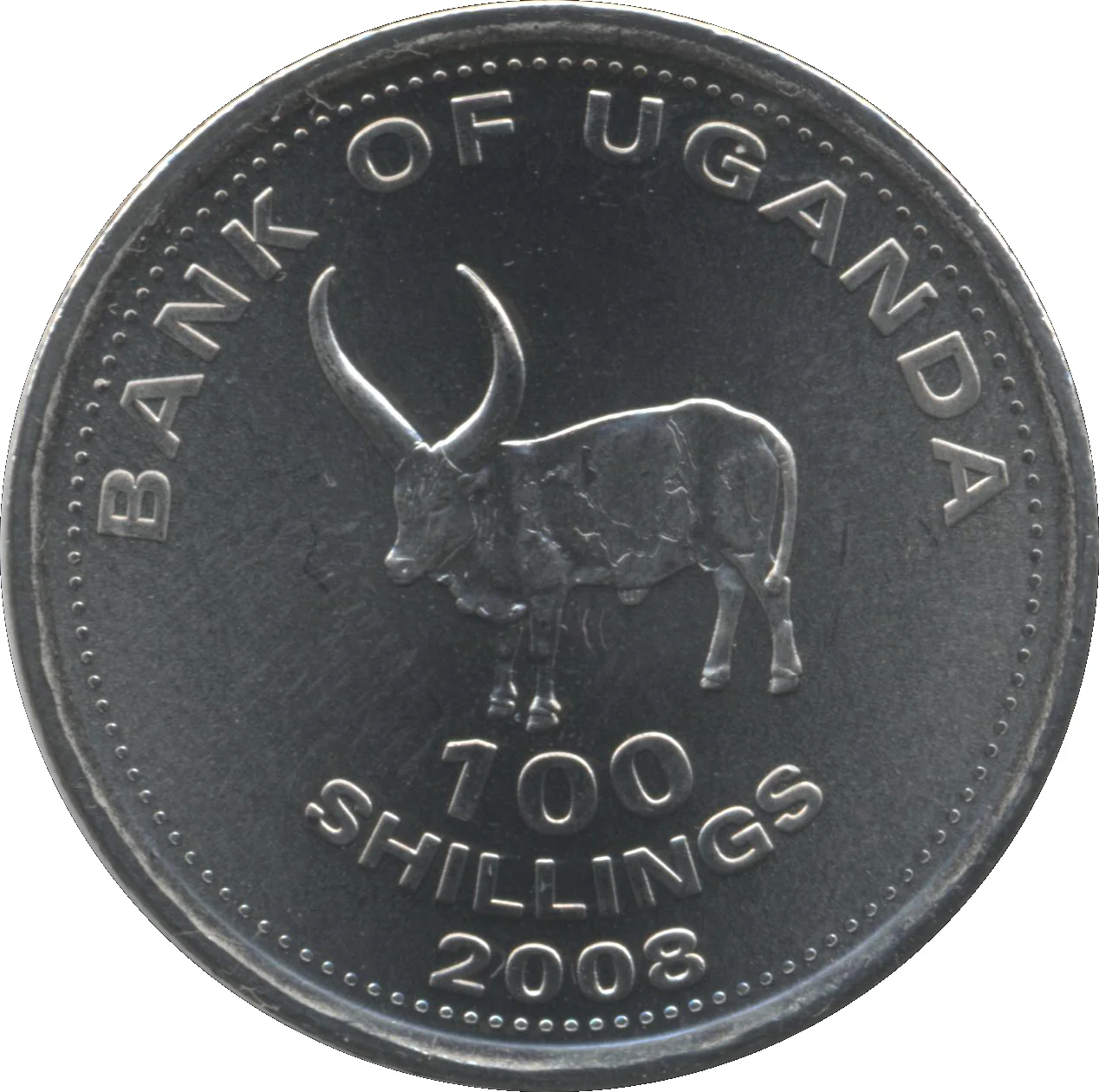

100 shillings – Uganda

Add to wishlist

Uganda

Context

Years: 2007–2022

Issuer: Uganda

Issuing organization: Bank of Uganda

Period:

(since 1962)

Currency:

(since 1987)

Material

References

KM: #

Numista: #44644

Value

Exchange value: 100 UGX

Obverse

Reverse

Description:

Sanga cattle (Bos taurus africanus), left-facing.

Inscription:

BANK OF UGANDA

100

SHILLINGS

2008

100

SHILLINGS

2008

Script: Latin

Engraver: Stan Witten

Edge

Reeded

Categories

| Animal> Cow |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Royal Canadian Mint of Winnipeg | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2007 | — | — | ||

| 2008 | — | — | ||

| 2012 | — | — | ||

| 2015 | — | — | ||

| 2019 | — | — | ||

| 2022 | — | — |

Historical background

In 2007, Uganda's currency situation was characterized by relative stability and cautious optimism, underpinned by a decade of strong economic growth and disciplined fiscal management. The Ugandan Shilling (UGX) traded within a managed float regime, with the Bank of Uganda (BoU) intervening to smooth excessive volatility. This period followed the successful stabilization efforts of the late 1990s and early 2000s, which had tamed hyperinflation and established macroeconomic credibility. The shilling exhibited general stability against the US dollar for much of the year, supported by robust inflows from donor aid, rising coffee exports, and growing remittances from the Ugandan diaspora.

However, underlying pressures were building. A significant challenge was the widening current account deficit, driven by a high import bill for oil, machinery, and manufactured goods against a still-narrow export base. Furthermore, the government's increasing domestic borrowing to fund infrastructure projects began to raise concerns about crowding out the private sector and exerting upward pressure on interest rates. While inflation was contained for most of the year, it began to show an upward creep towards the final quarter, fueled by rising global food and fuel prices, which would emerge as a major concern in 2008.

Overall, 2007 represented a calm before the storm. The currency stability was seen as an achievement of the inflation-targeting framework adopted by the BoU, but the economy remained vulnerable to external shocks and structural imbalances. The subsequent year, 2008, would test this stability severely, as the global financial crisis and domestic inflationary pressures led to a sharp depreciation of the shilling, pushing the central bank to tighten monetary policy significantly. Thus, 2007's relative calm allowed for continued economic planning but also masked the vulnerabilities that would soon be exposed.

However, underlying pressures were building. A significant challenge was the widening current account deficit, driven by a high import bill for oil, machinery, and manufactured goods against a still-narrow export base. Furthermore, the government's increasing domestic borrowing to fund infrastructure projects began to raise concerns about crowding out the private sector and exerting upward pressure on interest rates. While inflation was contained for most of the year, it began to show an upward creep towards the final quarter, fueled by rising global food and fuel prices, which would emerge as a major concern in 2008.

Overall, 2007 represented a calm before the storm. The currency stability was seen as an achievement of the inflation-targeting framework adopted by the BoU, but the economy remained vulnerable to external shocks and structural imbalances. The subsequent year, 2008, would test this stability severely, as the global financial crisis and domestic inflationary pressures led to a sharp depreciation of the shilling, pushing the central bank to tighten monetary policy significantly. Thus, 2007's relative calm allowed for continued economic planning but also masked the vulnerabilities that would soon be exposed.

Series: 2007 series

🌱 Very Common