5 córdobas – Nicaragua

Add to wishlist

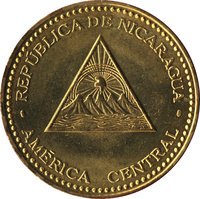

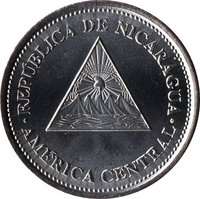

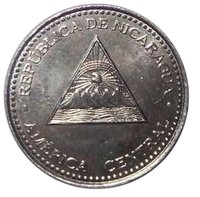

Nicaragua

Obverse

Reverse

Edge

Reeded

Categories

| Symbols> Coat of Arms |

| Symbol> Wreath |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2007 | — | — | ||

| 2014 | — | — |

Historical background

In 2007, Nicaragua's currency situation was characterized by a managed dual-exchange-rate system and relative stability under the government of President Daniel Ortega, who had returned to power in January of that year. The country operated with two official currencies: the Córdoba (C$) and the U.S. dollar, both legal tender for all transactions. The Central Bank of Nicaragua (BCN) maintained a crawling peg exchange rate regime for the córdoba, allowing it to depreciate slowly and predictably against the dollar to maintain export competitiveness. This stability was supported by Heavily Indebted Poor Countries (HIPC) Initiative debt relief, strong remittance inflows (which accounted for over 10% of GDP), and generally prudent fiscal and monetary policies that helped control inflation.

However, underlying vulnerabilities persisted. Dollarization remained high, with a significant portion of bank loans and deposits denominated in U.S. dollars, creating a currency mismatch risk for the economy. While inflation was moderate (around 9-11% for the year), it was primarily driven by high global oil and food prices, putting pressure on purchasing power for the population. The economic model remained heavily dependent on external factors—remittances, foreign aid (particularly from Venezuela under the Petrocaribe agreement), and commodity prices—making it sensitive to external shocks.

Overall, 2007 represented a period of calm before subsequent storms. The Ortega administration initially maintained the established economic framework, leading to macroeconomic stability and growth above 4%. This stability provided a foundation, but the high degree of dollarization and external dependence highlighted structural fragilities. These vulnerabilities would later be tested by the global financial crisis of 2008-2009 and, more profoundly, by the political and social crisis that erupted in Nicaragua in 2018.

However, underlying vulnerabilities persisted. Dollarization remained high, with a significant portion of bank loans and deposits denominated in U.S. dollars, creating a currency mismatch risk for the economy. While inflation was moderate (around 9-11% for the year), it was primarily driven by high global oil and food prices, putting pressure on purchasing power for the population. The economic model remained heavily dependent on external factors—remittances, foreign aid (particularly from Venezuela under the Petrocaribe agreement), and commodity prices—making it sensitive to external shocks.

Overall, 2007 represented a period of calm before subsequent storms. The Ortega administration initially maintained the established economic framework, leading to macroeconomic stability and growth above 4%. This stability provided a foundation, but the high degree of dollarization and external dependence highlighted structural fragilities. These vulnerabilities would later be tested by the global financial crisis of 2008-2009 and, more profoundly, by the political and social crisis that erupted in Nicaragua in 2018.

Series: 2007 series

🌱 Common