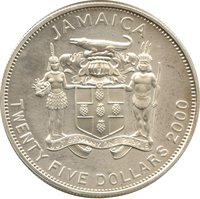

10 Dollars – Jamaica

Jamaica

Context

Material

References

KM: #Click to copy to clipboard196

Numista: #146989

Value

Exchange value: 10 JMD

Bullion value: $73.84

Obverse

Reverse

Edge

Categories

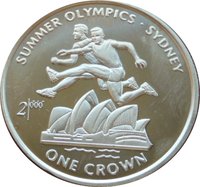

| Sport> Summer Olympic Games |

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2000 | — | — | Proof |

Historical background

In the year 2000, Jamaica's currency situation was characterized by a managed float of the Jamaican dollar (JMD) under significant pressure. Following the financial sector crisis of the mid-1990s, the government had abandoned a fixed exchange rate regime. However, consistent macroeconomic imbalances—notably a large current account deficit, high public debt exceeding 120% of GDP, and reliance on volatile capital inflows—led to persistent depreciation. The Bank of Jamaica (BOJ) intervened regularly in the foreign exchange market to smooth volatility, but the JMD still lost substantial value, eroding purchasing power and contributing to imported inflation.

This depreciation was driven by fundamental structural weaknesses. The economy was heavily import-dependent for fuel, food, and consumer goods, creating constant demand for US dollars, while key export sectors like bauxite/alumina and tourism generated earnings that were often insufficient to cover the import bill. Furthermore, high domestic interest rates, used to attract portfolio investment and curb inflation, created a costly cycle where debt servicing consumed a large portion of government revenue and foreign exchange reserves. Public skepticism and a strong preference for holding US dollars as a store of value further fueled depreciation pressures.

Consequently, the currency instability of 2000 presented a major policy challenge. The government, under Prime Minister P.J. Patterson, was engaged in a difficult balancing act with the International Monetary Fund (IMF), implementing stabilization programs aimed at fiscal discipline and inflation control to restore confidence. The primary goals were to stabilize the exchange rate, rebuild foreign reserves, and curb inflation, which remained in double digits. The situation underscored the deep-rooted link between Jamaica's fiscal health, its balance of payments, and the value of its currency, setting the stage for continued economic challenges in the decade ahead.

This depreciation was driven by fundamental structural weaknesses. The economy was heavily import-dependent for fuel, food, and consumer goods, creating constant demand for US dollars, while key export sectors like bauxite/alumina and tourism generated earnings that were often insufficient to cover the import bill. Furthermore, high domestic interest rates, used to attract portfolio investment and curb inflation, created a costly cycle where debt servicing consumed a large portion of government revenue and foreign exchange reserves. Public skepticism and a strong preference for holding US dollars as a store of value further fueled depreciation pressures.

Consequently, the currency instability of 2000 presented a major policy challenge. The government, under Prime Minister P.J. Patterson, was engaged in a difficult balancing act with the International Monetary Fund (IMF), implementing stabilization programs aimed at fiscal discipline and inflation control to restore confidence. The primary goals were to stabilize the exchange rate, rebuild foreign reserves, and curb inflation, which remained in double digits. The situation underscored the deep-rooted link between Jamaica's fiscal health, its balance of payments, and the value of its currency, setting the stage for continued economic challenges in the decade ahead.

Series: 2000 Summer Olympics, Sydney

✨ Legendary