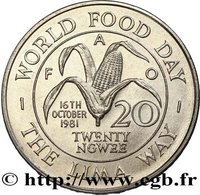

20 Ngwee (Bank of Zambia) – Zambia

Circulating commemorative coins

Commemoration: 20th Anniversary of Bank of Zambia

Zambia

Context

Material

Diameter: 28.5 mm

Weight: 11.3 g

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #Click to copy to clipboard23

Numista: #4441

Value

Exchange value: 0.20 ZMK

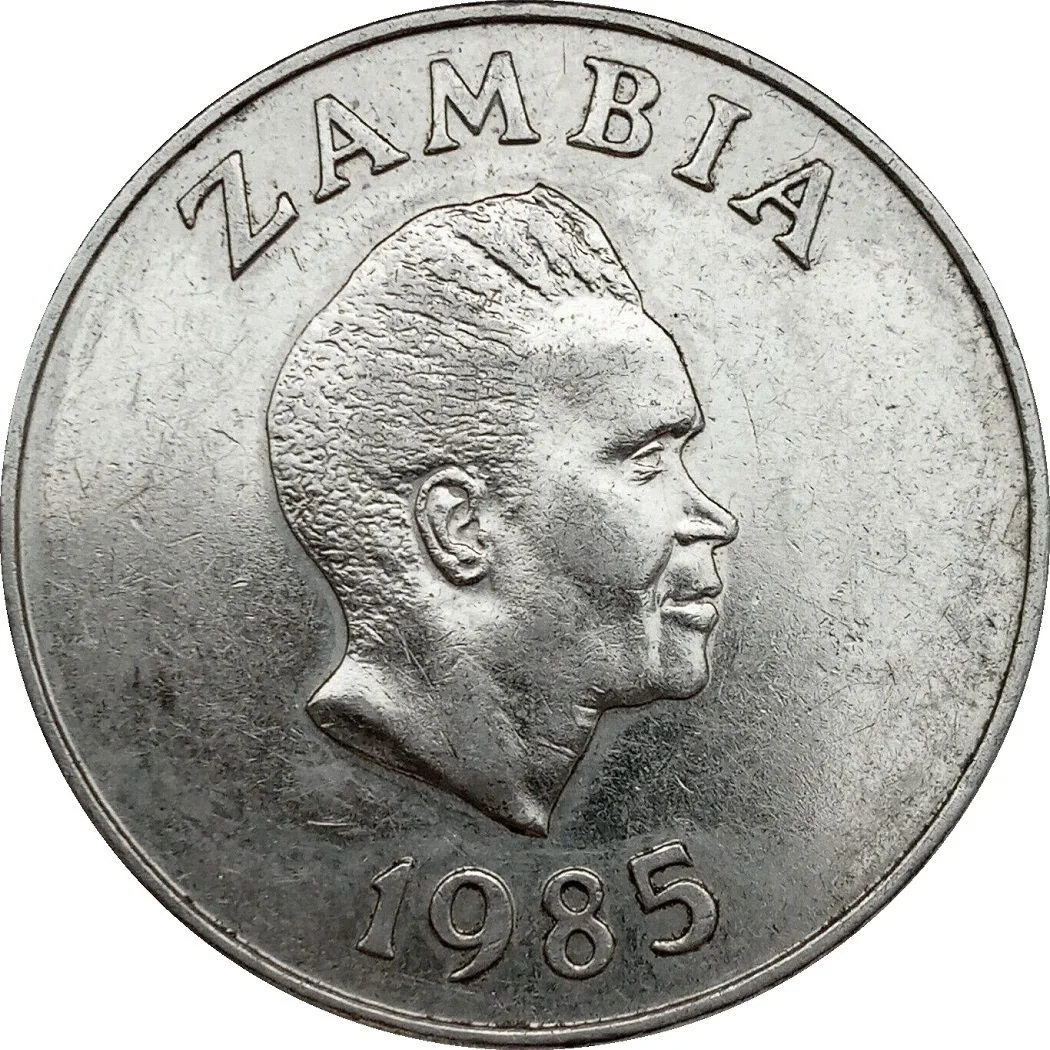

Obverse

Description:

Kenneth Kaunda, Zambian president, facing right. Date below.

Inscription:

ZAMBIA

1985

1985

Script: Latin

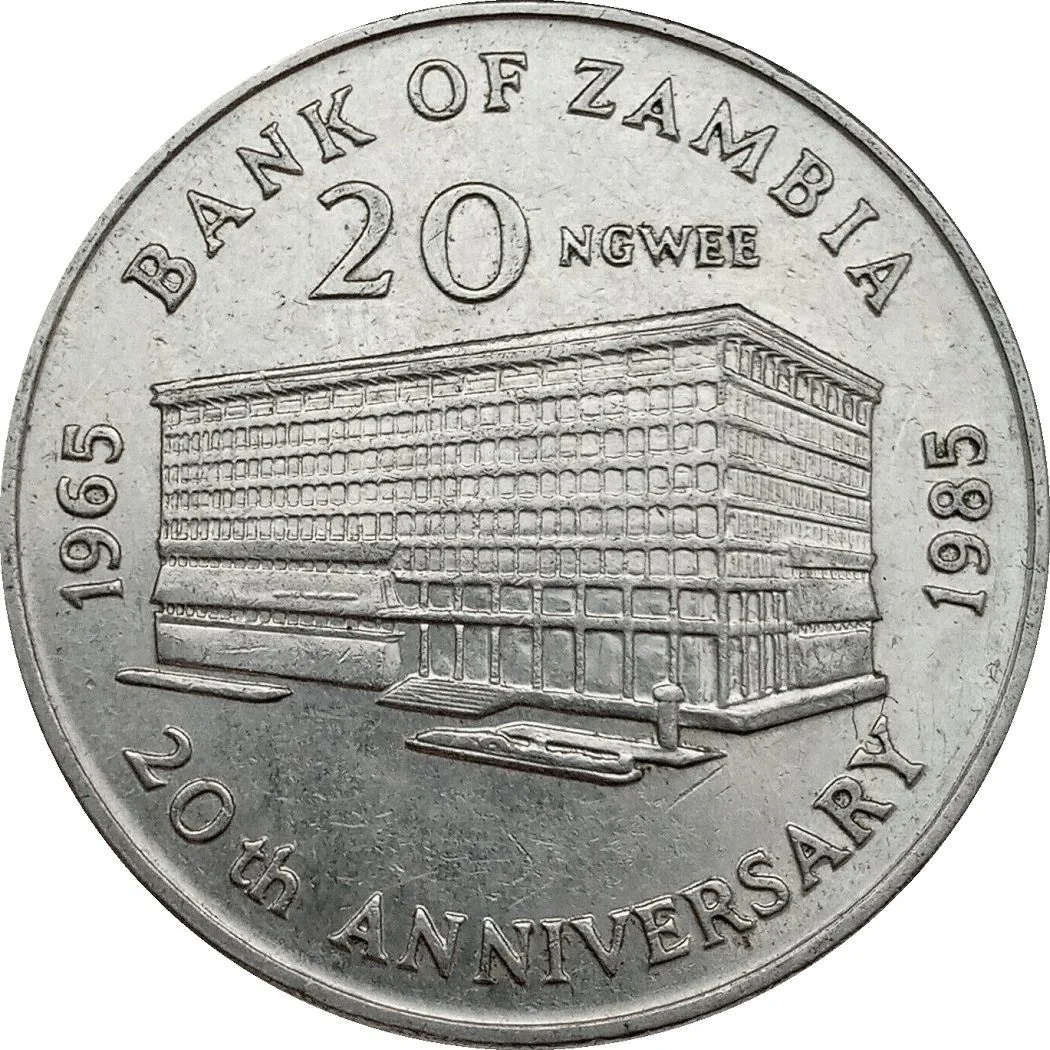

Reverse

Description:

Bank of Zambia encircled by text.

Inscription:

1965 BANK OF ZAMBIA 1985

20 NGWEE

20TH ANNIVERSARY

20 NGWEE

20TH ANNIVERSARY

Script: Latin

Edge

Reeded

Categories

| Building |

| Person> Politician |

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1985 | — | — |

Historical background

In 1985, Zambia's currency situation was a critical symptom of its profound economic crisis, rooted in a decade of falling copper prices, unsustainable debt, and structural imbalances. The country's overvalued official exchange rate for the Kwacha, maintained through strict controls, created a vast disparity with the black market, where the currency traded at a fraction of its official value. This dual system fueled rampant smuggling, crippled formal exports, and led to severe shortages of foreign exchange, which was desperately needed to import essential goods like medicines, spare parts, and fuel.

The government, under President Kenneth Kaunda and adhering to International Monetary Fund (IMF) guidance, attempted a major reform in October 1985. This involved a sharp devaluation of the Kwacha by nearly 80% and the introduction of a weekly auction system to determine the exchange rate, aiming to unify the official and parallel markets and attract donor support. Initially, the auction succeeded in stabilizing the currency and generating a modest inflow of foreign exchange, but the devaluation also triggered an immediate and severe spike in inflation, dramatically increasing the cost of living for the already struggling population.

Ultimately, the 1985 reforms proved unsustainable. The auction system was poorly managed and lacked transparency, leading to accusations of favouritism in the allocation of scarce foreign exchange. Furthermore, the government failed to implement necessary complementary measures, such as fiscal discipline and the removal of subsidies, which undermined confidence. By 1987, facing intense public pressure from soaring prices and empty shelves, President Kaunda abandoned the IMF program, reintroduced price controls, and effectively suspended the auction, plunging the currency regime back into disarray and deepening the economic isolation.

The government, under President Kenneth Kaunda and adhering to International Monetary Fund (IMF) guidance, attempted a major reform in October 1985. This involved a sharp devaluation of the Kwacha by nearly 80% and the introduction of a weekly auction system to determine the exchange rate, aiming to unify the official and parallel markets and attract donor support. Initially, the auction succeeded in stabilizing the currency and generating a modest inflow of foreign exchange, but the devaluation also triggered an immediate and severe spike in inflation, dramatically increasing the cost of living for the already struggling population.

Ultimately, the 1985 reforms proved unsustainable. The auction system was poorly managed and lacked transparency, leading to accusations of favouritism in the allocation of scarce foreign exchange. Furthermore, the government failed to implement necessary complementary measures, such as fiscal discipline and the removal of subsidies, which undermined confidence. By 1987, facing intense public pressure from soaring prices and empty shelves, President Kaunda abandoned the IMF program, reintroduced price controls, and effectively suspended the auction, plunging the currency regime back into disarray and deepening the economic isolation.

🌟 Uncommon