20 Ngwee – Zambia

Circulating commemorative coins

Commemoration: FAO - World Food Day 1981

Zambia

Context

Material

Diameter: 28.5 mm

Weight: 11.3 g

Thickness: 2.35 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #Click to copy to clipboard22

Numista: #4440

Value

Exchange value: 0.20 ZMK

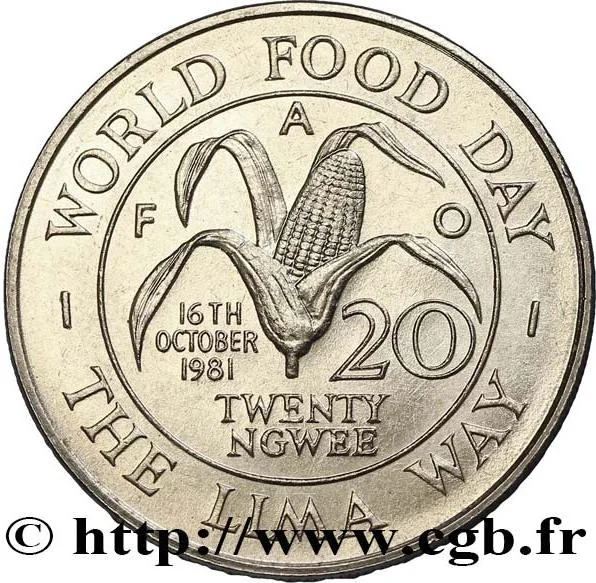

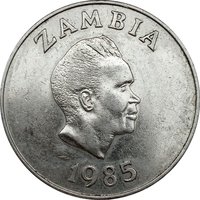

Obverse

Description:

Kenneth Kaunda, Zambian president, facing right. Date below.

Inscription:

ZAMBIA

1981

1981

Script: Latin

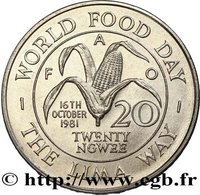

Reverse

Description:

Corn in center circle with date and denomination.

Inscription:

WORLD FOOD DAY

FAO 16TH OCTOBER 1981

20 TWENTY NGWEE

THE LIMA WAY

FAO 16TH OCTOBER 1981

20 TWENTY NGWEE

THE LIMA WAY

Script: Latin

Edge

Reeded

Categories

| Person> Politician |

| Organization> FAO |

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1981 | — | 970,000 |

Historical background

In 1981, Zambia was grappling with a severe economic crisis that placed immense pressure on its currency, the kwacha. The nation's heavy dependence on copper exports, which accounted for over 90% of foreign exchange earnings, proved catastrophic as global copper prices collapsed in the mid-1970s. This was compounded by rising oil import costs, costly regional commitments, and persistent fiscal deficits. By 1981, the economy was in recession, foreign reserves were nearly depleted, and the official exchange rate had become wildly overvalued, creating a thriving black market for foreign currency.

The government of President Kenneth Kaunda, adhering to a socialist-oriented model of "humanism," was initially resistant to structural reforms or devaluation advocated by the International Monetary Fund (IMF). Price controls, subsidies on essential goods, and a fixed exchange rate were maintained to protect citizens, but these measures distorted the economy. The overvalued kwacha made imports artificially cheap, draining reserves, while making non-copper exports uncompetitive. This led to severe shortages of imported goods, including vital machinery, spare parts, and medicines, crippling industrial and agricultural productivity.

Consequently, 1981 represented a critical juncture of mounting disequilibrium. The currency situation was unsustainable, with a significant gap between the official and black-market rates signalling a loss of confidence. While a formal devaluation and an agreement with the IMF would not be finalized until 1983, the pressures of 1981 made it clear that Zambia's existing economic policies were untenable, setting the stage for a painful period of structural adjustment that would fundamentally alter the country's economic landscape.

The government of President Kenneth Kaunda, adhering to a socialist-oriented model of "humanism," was initially resistant to structural reforms or devaluation advocated by the International Monetary Fund (IMF). Price controls, subsidies on essential goods, and a fixed exchange rate were maintained to protect citizens, but these measures distorted the economy. The overvalued kwacha made imports artificially cheap, draining reserves, while making non-copper exports uncompetitive. This led to severe shortages of imported goods, including vital machinery, spare parts, and medicines, crippling industrial and agricultural productivity.

Consequently, 1981 represented a critical juncture of mounting disequilibrium. The currency situation was unsustainable, with a significant gap between the official and black-market rates signalling a loss of confidence. While a formal devaluation and an agreement with the IMF would not be finalized until 1983, the pressures of 1981 made it clear that Zambia's existing economic policies were untenable, setting the stage for a painful period of structural adjustment that would fundamentally alter the country's economic landscape.

🌱 Fairly Common