5 cents – United States

Add to wishlist

United States

Context

Years: 1938–2003

Issuer: United States

Period:

(since 1776)

Currency:

(since 1785)

Total mintage: 44,638,235,609

Material

References

KM: #

Numista: #44

Value

Exchange value: 0.05 USD = $0.05

Inflation-adjusted value: 1.12 USD

Obverse

Description:

Portrait of Thomas Jefferson, U.S. president from 1801 to 1809.

Inscription:

IN GOD WE TRUST

LIBERTY * 1997 P

FS

LIBERTY * 1997 P

FS

Script: Latin

Engraver: Felix Schlag

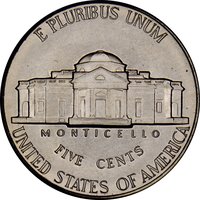

Reverse

Description:

Monticello, Thomas Jefferson's Virginia estate.

Inscription:

E PLURIBUS UNUM

MONTICELLO

FIVE CENTS

UNITED STATES OF AMERICA

MONTICELLO

FIVE CENTS

UNITED STATES OF AMERICA

Translation:

Out of many, one

Monticello

Five Cents

United States of America

Monticello

Five Cents

United States of America

Script: Latin

Engraver: Felix Schlag

Edge

Plain

Categories

| Building |

| Person> Politician |

Mints

| Name | Mark |

|---|---|

| United States Mint of Denver | — |

| United States Mint of Philadelphia | — |

| United States Mint of Denver | D |

| United States Mint of Philadelphia | P |

| United States Mint of San Francisco | S |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1938 | — | 19,496,000 | ||

| 1938 | — | 19,365 | Proof | |

| 1938 | D | 5,376,000 | ||

| 1938 | S | 4,105,000 | ||

| 1939 | — | — | ||

| 1939 | — | — | Proof | |

| 1939 | D | — | ||

| 1939 | S | — | ||

| 1940 | — | 14,158 | Proof | |

| 1940 | — | 176,485,000 | ||

| 1940 | D | 43,540,000 | ||

| 1940 | S | 39,690,000 | ||

| 1941 | D | 53,432,000 | ||

| 1941 | S | — | ||

| 1941 | — | 18,720 | Proof | |

| 1941 | — | 203,265,000 | ||

| 1942 | — | 49,789,000 | ||

| 1942 | — | 29,600 | Proof | |

| 1942 | D | 13,938,000 | ||

| 1946 | — | 161,116,000 | ||

| 1946 | D | 45,292,200 | ||

| 1946 | S | 13,560,000 | ||

| 1947 | D | 37,822,000 | ||

| 1947 | S | 24,720,000 | ||

| 1947 | — | 95,000,000 | ||

| 1948 | — | 89,348,000 | ||

| 1948 | D | 44,734,000 | ||

| 1948 | S | 11,300,000 | ||

| 1949 | — | 60,652,000 | ||

| 1949 | D | 36,498,000 | ||

| 1949 | S | 9,716,000 | ||

| 1950 | — | 9,796,000 | ||

| 1950 | — | 51,386 | Proof | |

| 1950 | D | 2,630,030 | ||

| 1951 | D | 20,460,000 | ||

| 1951 | S | 7,776,000 | ||

| 1951 | — | 28,552,000 | ||

| 1951 | — | 57,500 | Proof | |

| 1952 | — | 63,988,000 | ||

| 1952 | — | 81,980 | Proof | |

| 1952 | D | 30,638,000 | ||

| 1952 | S | 20,572,000 | ||

| 1953 | — | 46,644,000 | ||

| 1953 | — | 128,800 | Proof | |

| 1953 | D | 59,878,600 | ||

| 1953 | S | 19,210,900 | ||

| 1954 | S | 29,384,000 | ||

| 1954 | — | 47,684,050 | ||

| 1954 | — | 233,300 | Proof | |

| 1954 | D | 117,183,060 | ||

| 1955 | — | 7,888,000 | ||

| 1955 | — | 378,200 | Proof | |

| 1955 | D | 74,464,100 | ||

| 1956 | — | 35,216,000 | ||

| 1956 | — | 669,384 | Proof | |

| 1956 | D | 67,222,940 | ||

| 1957 | — | 38,408,000 | ||

| 1957 | — | 1,247,952 | Proof | |

| 1957 | D | 136,828,900 | ||

| 1958 | — | 17,088,000 | ||

| 1958 | — | 875,652 | Proof | |

| 1958 | D | 168,249,120 | ||

| 1959 | — | 1,149,291 | Proof | |

| 1959 | D | 160,738,240 | ||

| 1959 | — | 27,248,000 | ||

| 1960 | — | 55,416,000 | ||

| 1960 | — | 1,691,602 | Proof | |

| 1960 | D | 192,582,180 | ||

| 1961 | — | 73,640,100 | ||

| 1961 | — | 3,028,144 | Proof | |

| 1961 | D | 229,342,760 | ||

| 1962 | — | 97,384,000 | ||

| 1962 | — | 3,218,019 | Proof | |

| 1962 | D | 280,195,720 | ||

| 1963 | — | 3,075,645 | Proof | |

| 1963 | — | 175,776,000 | ||

| 1963 | D | 276,829,460 | ||

| 1964 | — | 1,024,672,000 | ||

| 1964 | — | 3,950,762 | Proof | |

| 1964 | D | 1,787,297,160 | ||

| 1965 | — | 136,131,380 | ||

| 1966 | — | 156,208,283 | ||

| 1967 | — | 107,325,800 | ||

| 1968 | D | 91,227,860 | ||

| 1968 | S | 100,396,004 | ||

| 1968 | S | 3,041,506 | Proof | |

| 1969 | S | 120,165,000 | ||

| 1969 | S | 2,934,631 | Proof | |

| 1969 | D | 202,807,500 | ||

| 1970 | D | 515,485,380 | ||

| 1970 | S | 238,832,004 | ||

| 1970 | S | 2,632,810 | Proof | |

| 1971 | — | — | ||

| 1971 | D | 316,144,800 | ||

| 1971 | S | 3,220,733 | Proof | |

| 1972 | — | 202,036,000 | ||

| 1972 | D | 351,694,600 | ||

| 1972 | S | 3,260,996 | Proof | |

| 1973 | — | 384,396,000 | ||

| 1973 | D | 261,405,000 | ||

| 1973 | S | 2,760,339 | Proof | |

| 1974 | D | 277,373,000 | ||

| 1974 | S | 2,612,568 | Proof | |

| 1974 | — | 601,752,000 | ||

| 1975 | — | 181,772,000 | ||

| 1975 | D | 401,875,300 | ||

| 1975 | S | 2,845,450 | Proof | |

| 1976 | — | 367,124,000 | ||

| 1976 | D | 563,964,147 | ||

| 1976 | S | 4,149,730 | Proof | |

| 1977 | — | 585,376,000 | ||

| 1977 | D | 297,313,422 | ||

| 1977 | S | 3,251,152 | Proof | |

| 1978 | — | 391,308,000 | ||

| 1978 | D | 313,092,780 | ||

| 1978 | S | 3,127,781 | Proof | |

| 1979 | S | — | Proof | |

| 1979 | — | 463,188,000 | ||

| 1979 | D | 325,867,672 | ||

| 1980 | D | 502,323,448 | ||

| 1980 | S | 3,554,806 | Proof | |

| 1980 | P | 593,004,000 | ||

| 1981 | S | — | Proof | |

| 1981 | D | 364,801,843 | ||

| 1981 | P | 657,504,000 | ||

| 1982 | D | 373,726,544 | ||

| 1982 | P | 292,355,000 | ||

| 1982 | S | 3,857,479 | Proof | |

| 1983 | D | 536,726,276 | ||

| 1983 | P | 561,615,000 | ||

| 1983 | S | 3,279,126 | Proof | |

| 1984 | D | 517,675,146 | ||

| 1984 | P | 746,769,000 | ||

| 1984 | S | 3,065,110 | Proof | |

| 1985 | D | 459,747,446 | ||

| 1985 | P | 647,114,962 | ||

| 1985 | S | 3,362,821 | Proof | |

| 1986 | D | 361,819,140 | ||

| 1986 | P | 536,883,483 | ||

| 1986 | S | 3,010,497 | Proof | |

| 1987 | P | 371,499,481 | ||

| 1987 | S | 4,227,728 | Proof | |

| 1987 | D | 410,590,604 | ||

| 1988 | S | 3,262,948 | Proof | |

| 1988 | P | 771,360,000 | ||

| 1988 | D | 663,771,652 | ||

| 1989 | D | 570,842,474 | ||

| 1989 | P | 898,812,000 | ||

| 1989 | S | 3,220,194 | Proof | |

| 1990 | P | 661,636,000 | ||

| 1990 | S | 3,299,559 | Proof | |

| 1990 | D | 663,938,503 | ||

| 1991 | D | 436,496,678 | ||

| 1991 | P | 614,104,000 | ||

| 1991 | S | 2,867,787 | Proof | |

| 1992 | D | 450,565,113 | ||

| 1992 | P | 399,552,000 | ||

| 1992 | S | 4,176,560 | Proof | |

| 1993 | D | 406,084,135 | ||

| 1993 | P | 412,076,000 | ||

| 1993 | S | 3,394,792 | Proof | |

| 1994 | D | 715,762,110 | ||

| 1994 | P | 722,160,000 | ||

| 1994 | P | 167,703 | Proof | |

| 1994 | S | 3,269,923 | Proof | |

| 1995 | D | 888,112,000 | ||

| 1995 | P | 774,156,000 | ||

| 1995 | S | 2,797,481 | Proof | |

| 1996 | S | 2,525,265 | Proof | |

| 1996 | D | 817,736,000 | ||

| 1996 | P | 829,332,000 | ||

| 1997 | D | 466,640,000 | ||

| 1997 | P | 25,000 | Proof | |

| 1997 | S | 2,796,678 | Proof | |

| 1997 | P | 470,972,000 | ||

| 1998 | D | 635,360,000 | ||

| 1998 | P | 688,272,000 | ||

| 1998 | S | 2,086,507 | Proof | |

| 1999 | D | 1,066,720,000 | ||

| 1999 | P | 1,212,000,000 | ||

| 1999 | S | 3,347,966 | Proof | |

| 2000 | D | 1,509,520,000 | ||

| 2000 | P | 846,240,000 | ||

| 2000 | S | 4,047,993 | Proof | |

| 2001 | S | 3,184,606 | Proof | |

| 2001 | D | 627,680,000 | ||

| 2001 | P | 675,704,000 | ||

| 2002 | P | 539,280,000 | ||

| 2002 | D | 691,200,000 | ||

| 2002 | S | 3,211,995 | Proof | |

| 2003 | D | 383,040,000 | ||

| 2003 | P | 441,840,000 | ||

| 2003 | S | 3,298,439 | Proof |

Historical background

In 1938, the United States was grappling with the lingering effects of the Great Depression under President Franklin D. Roosevelt's New Deal. The currency situation was defined by a managed and devalued dollar, a direct result of the 1934 Gold Reserve Act. This legislation had devalued the dollar by nearly 40% by resetting the price of gold from $20.67 to $35 per ounce, a policy intended to combat deflation by raising domestic prices and stimulating economic activity. The U.S. was effectively off the classical gold standard for domestic transactions, as citizens could no longer redeem dollars for gold coins, though the government still maintained a fixed gold price for international settlements with other central banks.

Monetary policy was in a state of cautious tension. The Federal Reserve, having raised reserve requirements in 1936-37 in a premature move to curb potential inflation, had inadvertently helped trigger the severe "Roosevelt Recession" of 1937-38. This policy error left banks with little excess liquidity and contributed to a sharp economic downturn. Consequently, by 1938, the Fed shifted to a more accommodative stance, lowering reserve requirements and keeping interest rates near zero to promote lending and recovery. The money supply, however, remained constrained by weak bank lending and continued public wariness following the widespread bank failures of the early 1930s.

Internationally, the dollar's fixed gold price made it a relatively stable and strong currency in a world of fluctuating exchange rates, attracting gold inflows to Fort Knox. This stability contrasted with the economic turmoil and competitive devaluations seen in Europe. Domestically, the currency regime supported gradual recovery but also reflected the New Deal's philosophy of active government management of the economy. The system established in this period—a dollar convertible for foreign governments but not for citizens—would form the bedrock of the Bretton Woods international monetary system established after World War II.

Monetary policy was in a state of cautious tension. The Federal Reserve, having raised reserve requirements in 1936-37 in a premature move to curb potential inflation, had inadvertently helped trigger the severe "Roosevelt Recession" of 1937-38. This policy error left banks with little excess liquidity and contributed to a sharp economic downturn. Consequently, by 1938, the Fed shifted to a more accommodative stance, lowering reserve requirements and keeping interest rates near zero to promote lending and recovery. The money supply, however, remained constrained by weak bank lending and continued public wariness following the widespread bank failures of the early 1930s.

Internationally, the dollar's fixed gold price made it a relatively stable and strong currency in a world of fluctuating exchange rates, attracting gold inflows to Fort Knox. This stability contrasted with the economic turmoil and competitive devaluations seen in Europe. Domestically, the currency regime supported gradual recovery but also reflected the New Deal's philosophy of active government management of the economy. The system established in this period—a dollar convertible for foreign governments but not for citizens—would form the bedrock of the Bretton Woods international monetary system established after World War II.

🌱 Very Common