10 rubles – Russian Federation

Add to wishlist

Russia

Context

Year: 2024

Country: Russia

Issuer: Russian Federation

Period:

(since 1991)

Currency:

(since 1998)

Total mintage: 1,000,000

Material

References

Numista: #433303

CBR: #5714-0101

Value

Exchange value: 10 RUB

Inflation-adjusted value: 10.37 RUB

Obverse

Description:

Center: '10 РУБЛЕЙ'. Inside the '0', a hidden '10' and 'РУБ' appear at different angles. Flanked by stylized laurel (left) and oak (right) branches. Top rim: 'БАНК РОССИИ'. Bottom: '2024' with mint mark.

Inscription:

БАНК РОССИИ

10

РУБЛЕЙ

2024 ММД

10

РУБЛЕЙ

2024 ММД

Translation:

BANK OF RUSSIA

10

RUBLES

2024 MMD

10

RUBLES

2024 MMD

Script: Cyrillic

Language: Russian

Designer and engraver: Alexander Vasilyevich Baklanov

Reverse

Description:

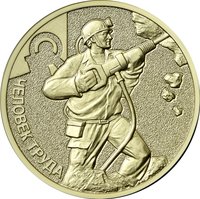

The reverse shows a teacher at a blackboard and desk, with the inscription ‘ЧЕЛОВЕК ТРУДА’ (THE MAN OF LABOUR) above.

Inscription:

ЧЕЛОВЕК ТРУДА

Translation:

THE WORKING MAN

Script: Cyrillic

Language: Russian

Engraver: Alexandra Arsenyevna Dolgopolova

Designer: Andrey Anatolyevich Brynza

Edge

Categories

| Education |

Mints

| Name | Mark |

|---|---|

| Moscow Mint | (ММД) |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2024 | ММД | 1,000,000 |

Historical background

In 2024, the currency situation in the Russian Federation is defined by a state of managed stability under persistent pressure. The ruble's value is primarily dictated by a complex system of capital controls, mandatory foreign currency revenue sales for exporters, and high central bank interest rates (held at 16% for much of the year to combat inflation). This artificial stability has been engineered to shield the economy from the immediate shocks of extensive Western sanctions, particularly those targeting the financial system and energy exports. However, this stability is underpinned by a fundamental shift in trade flows and a sustained decline in imports, rather than robust economic health or investor confidence.

The underlying pressures are significant and structural. The country's current account surplus has sharply narrowed, primarily due to the effective G7 oil price cap and the costly re-routing of energy exports to alternative markets like India and China, which increases transportation costs and discounts. Simultaneously, military-related imports and "parallel imports" of consumer goods to replace departed Western brands have kept demand for foreign currency high. This creates a constant tug-of-war: export revenues in foreign currency are being squeezed while import needs persist, applying a steady depreciatory force on the ruble that requires continuous administrative measures to contain.

Looking forward, the currency regime remains a critical vulnerability. The stability is costly, relying on draining reserves and stringent controls that deter foreign investment and distort the domestic economy. The central bank faces a difficult balancing act between controlling inflation (fueled by high military spending and labor shortages) and avoiding excessive tightening that could stifle economic activity. Consequently, the ruble's trajectory in 2024 is less a reflection of market sentiment and more a direct barometer of the state's ability to enforce its financial defenses, the efficacy of sanctions evasion, and the long-term fiscal burden of the war in Ukraine.

The underlying pressures are significant and structural. The country's current account surplus has sharply narrowed, primarily due to the effective G7 oil price cap and the costly re-routing of energy exports to alternative markets like India and China, which increases transportation costs and discounts. Simultaneously, military-related imports and "parallel imports" of consumer goods to replace departed Western brands have kept demand for foreign currency high. This creates a constant tug-of-war: export revenues in foreign currency are being squeezed while import needs persist, applying a steady depreciatory force on the ruble that requires continuous administrative measures to contain.

Looking forward, the currency regime remains a critical vulnerability. The stability is costly, relying on draining reserves and stringent controls that deter foreign investment and distort the domestic economy. The central bank faces a difficult balancing act between controlling inflation (fueled by high military spending and labor shortages) and avoiding excessive tightening that could stifle economic activity. Consequently, the ruble's trajectory in 2024 is less a reflection of market sentiment and more a direct barometer of the state's ability to enforce its financial defenses, the efficacy of sanctions evasion, and the long-term fiscal burden of the war in Ukraine.

Series: Man of Labour

🌟 Uncommon