100 Kroner – Norway

Non-circulating coins

Commemoration: 1994 Olympics in Lillehammer

Norway

Context

Material

References

KM: #Click to copy to clipboard441

Numista: #42908

Value

Exchange value: 100 NOK = $10.46

Bullion value: $88.00

Inflation-adjusted value: 219.61 NOK

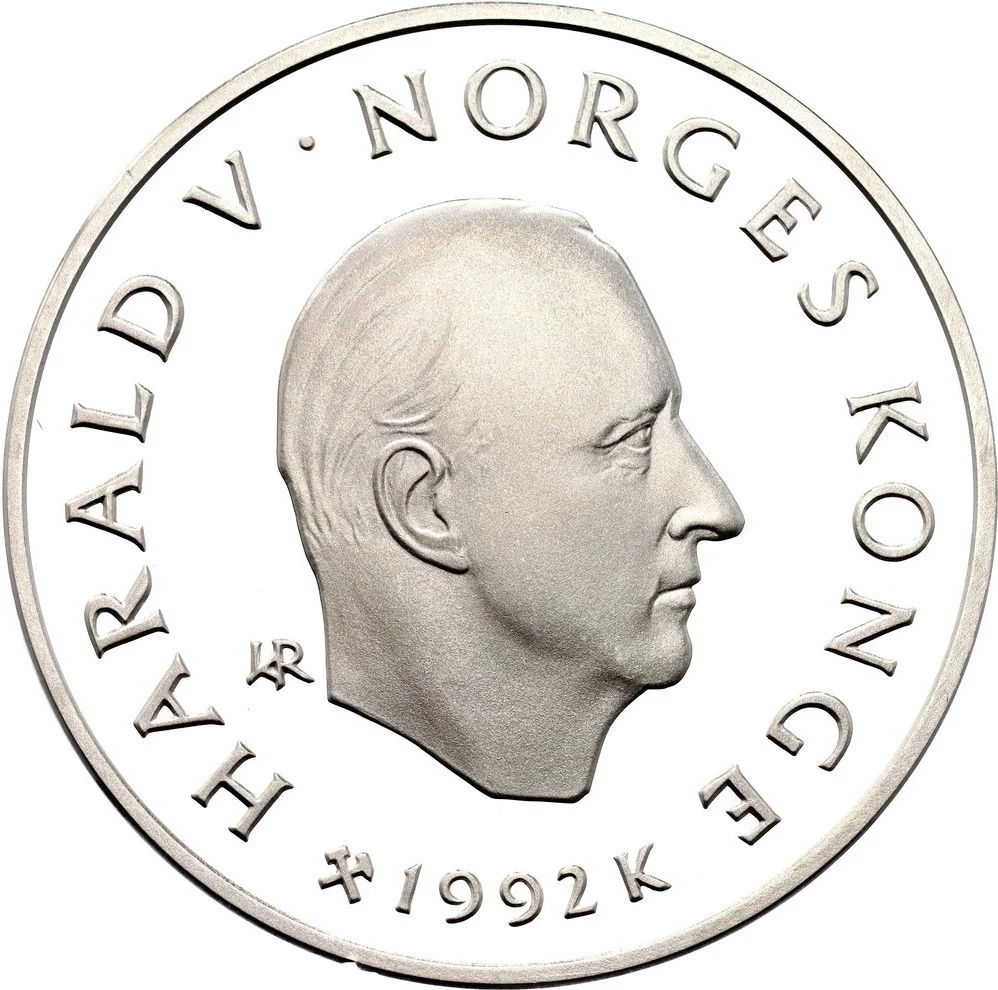

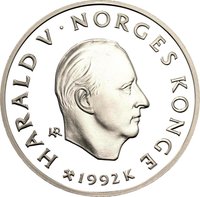

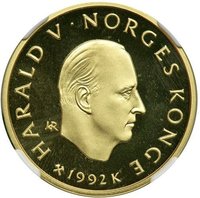

Obverse

Description:

King Harald V facing right, engraver's initials behind bust. Inscription surrounds. Mintmark, date, and mintmaster's initial below. Solid rim ring.

Inscription:

HARALD V · NORGES KONGE

IAR

⚒ 1992 K

IAR

⚒ 1992 K

Translation:

Harald V, Norway's King

IAR

⚒ 1992 K

IAR

⚒ 1992 K

Script: Latin

Engraver: Ingrid Austlid Rise

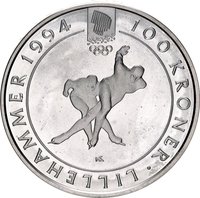

Reverse

Description:

Two hockey players facing off. Designer initials left of players, inside a solid ring broken only by the sticks at top and bottom. Olympic logo inside. Value and inscription surround a solid rim.

Inscription:

100 KRONER | LILLEHAMMER 1994

KN

KN

Script: Latin

Engraver: Ingrid Austlid Rise

Designer: Krzysztof Nasilowski

Categories

| Sport> Winter Olympic Games |

| Sport> Hockey |

Mints

| Name | Mark |

|---|---|

| Norwegian Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1992 | — | 53,858 | Proof |

Historical background

In 1992, Norway's currency situation was defined by its participation in a European Exchange Rate Mechanism (ERM), albeit a unilateral and adapted version. Following the collapse of the Bretton Woods system, Norway had sought exchange rate stability by pegging its currency, the krone (NOK), to a trade-weighted basket of currencies. In 1990, this was formally changed to a peg exclusively against the European Currency Unit (ECU), effectively shadowing the ERM. This policy was driven by Norway's deep economic ties with Europe and aimed to import low inflation and provide predictability for its vital export sectors, particularly oil and gas.

However, this peg came under severe strain in 1992 due to turbulent international financial markets. The period was marked by the European currency crisis, where speculative attacks forced several ERM currencies to devalue or abandon their pegs altogether. While Norway was not a full ERM member, the krone was caught in the crossfire. Speculators, witnessing the success of attacks on currencies like the British pound and Italian lira, also targeted the Norwegian krone, doubting the central bank's willingness to maintain the peg amidst differing economic conditions. Domestic interest rates were raised dramatically—at one point to 500% overnight—to defend the currency, creating significant economic tension.

Ultimately, the defense proved too costly. On December 10, 1992, Norges Bank, the Norwegian central bank, surrendered to market pressure and allowed the krone to float freely. This decision was taken to prioritize domestic economic stability over the exchange rate anchor, freeing monetary policy to address rising unemployment and a banking crisis. The float was initially turbulent but was later followed by the adoption of a formal inflation-targeting regime in 2001, marking a definitive end to the era of fixed exchange rates in Norway.

However, this peg came under severe strain in 1992 due to turbulent international financial markets. The period was marked by the European currency crisis, where speculative attacks forced several ERM currencies to devalue or abandon their pegs altogether. While Norway was not a full ERM member, the krone was caught in the crossfire. Speculators, witnessing the success of attacks on currencies like the British pound and Italian lira, also targeted the Norwegian krone, doubting the central bank's willingness to maintain the peg amidst differing economic conditions. Domestic interest rates were raised dramatically—at one point to 500% overnight—to defend the currency, creating significant economic tension.

Ultimately, the defense proved too costly. On December 10, 1992, Norges Bank, the Norwegian central bank, surrendered to market pressure and allowed the krone to float freely. This decision was taken to prioritize domestic economic stability over the exchange rate anchor, freeing monetary policy to address rising unemployment and a banking crisis. The float was initially turbulent but was later followed by the adoption of a formal inflation-targeting regime in 2001, marking a definitive end to the era of fixed exchange rates in Norway.

⭐ Somewhat Rare