100 kroner – Norway

Add to wishlist

Non-circulating coins

Commemoration: 1994 Olympics in Lillehammer

Norway

Material

References

KM: #

Numista: #58142

Value

Exchange value: 100 NOK

Bullion value: $79.27

Inflation-adjusted value: 227.16 NOK

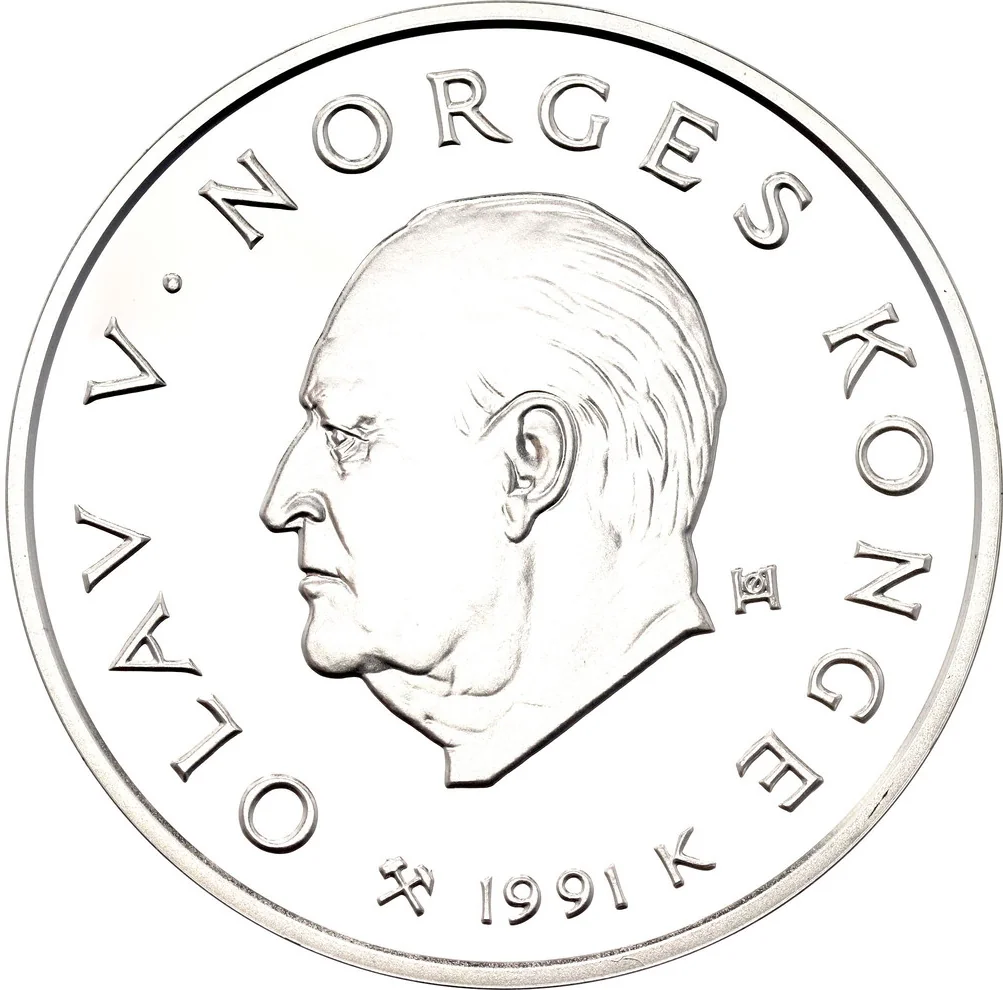

Obverse

Description:

King Olav V left-facing bust. Engraver's initials behind head. Inscription surrounds. Mintmark, date, and mintmaster initial below. Solid rim ring.

Inscription:

OLAV V · NORGES KONGE

ØH

⚒ 1991 K

ØH

⚒ 1991 K

Translation:

Olav V, Norway's King

ØH

⚒ 1991 K

ØH

⚒ 1991 K

Script: Latin

Engraver: Øivind Hansen

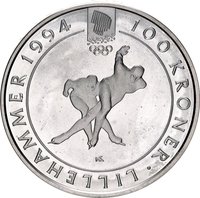

Reverse

Description:

Cross-country skier facing left inside a solid ring, broken at the top by the Olympic logo. Designer's initials at bottom right. Surrounded by value and inscription, with a solid ring on the rim.

Inscription:

100 KRONER · LILLEHAMMER 1994

HW

HW

Script: Latin

Engraver: Grażyna Nasilowska

Designer: Harald Wårvik

Categories

| Sport> Ski |

| Sport> Winter Olympic Games |

Mints

| Name | Mark |

|---|---|

| Norwegian Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1991 | — | 60,181 | Proof |

Historical background

In 1991, Norway's currency situation was defined by its managed exchange rate regime, where the Norwegian krone (NOK) was pegged to a trade-weighted basket of currencies, primarily the European Currency Unit (ECU). This system, established in the 1970s, aimed to provide stability for the small, open economy by tethering the krone to its major trading partners, thus reducing uncertainty for exporters and importers. However, maintaining this peg required continuous intervention by Norges Bank, the central bank, which used interest rate adjustments and foreign currency reserves to defend the krone's value against market pressures.

The period was marked by significant economic strain following a domestic banking crisis and a sharp recession, which put the fixed exchange rate under severe stress. High interest rates, necessary to support the krone and curb inflation, exacerbated the downturn by increasing debt-servicing costs for businesses and households. Furthermore, the international context was volatile, with European currencies facing turbulence in the lead-up to the Maastricht Treaty, creating additional speculative pressures on the krone peg.

This precarious situation ultimately proved unsustainable. In December 1992, in the wake of the European Exchange Rate Mechanism (ERM) crisis, Norway was forced to abandon its fixed exchange rate, allowing the krone to float. While this decisive shift occurred just after 1991, the entire year was a critical prelude, characterized by mounting market skepticism, dwindling foreign reserves, and the growing realization that the defensive high-interest rate policy was causing unacceptable damage to the real economy.

The period was marked by significant economic strain following a domestic banking crisis and a sharp recession, which put the fixed exchange rate under severe stress. High interest rates, necessary to support the krone and curb inflation, exacerbated the downturn by increasing debt-servicing costs for businesses and households. Furthermore, the international context was volatile, with European currencies facing turbulence in the lead-up to the Maastricht Treaty, creating additional speculative pressures on the krone peg.

This precarious situation ultimately proved unsustainable. In December 1992, in the wake of the European Exchange Rate Mechanism (ERM) crisis, Norway was forced to abandon its fixed exchange rate, allowing the krone to float. While this decisive shift occurred just after 1991, the entire year was a critical prelude, characterized by mounting market skepticism, dwindling foreign reserves, and the growing realization that the defensive high-interest rate policy was causing unacceptable damage to the real economy.

⭐ Somewhat Rare