20 centésimos – Uruguay

Add to wishlist

Uruguay

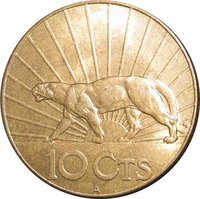

Obverse

Reverse

Edge

Reeded

Categories

| Person> Military leader |

| Person> Politician |

| Symbols> Coat of Arms |

| Symbol> Sun |

| Symbol> Wreath |

Mints

| Name | Mark |

|---|---|

| Casa de Moneda de Chile | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1920 | — | 2,500,000 |

Historical background

In 1920, Uruguay's currency situation was characterized by instability and inflationary pressures, a direct legacy of the economic disruptions caused by the First World War. Prior to the war, Uruguay, like many nations, adhered to the gold standard, which provided monetary stability. However, the war severed global financial links and caused a dramatic decline in international trade. For Uruguay, a primary exporter of meat and wool, this resulted in a sharp fall in export revenues and government income, financed largely by customs duties. To cover budget deficits, the government under President Baltasar Brum increasingly resorted to issuing paper money without metallic backing, leading to a growing divergence between the paper peso and the gold peso.

This period saw the emergence of a severe dual-currency system. The gold peso (peso oro), used for international transactions and as a stable unit of account, maintained its value. Meanwhile, the circulating paper peso (peso moneda nacional) depreciated significantly on the free market. This created immense complexity for commerce and banking, with prices, contracts, and debts often specified in one currency or the other, requiring constant conversion at fluctuating rates. The inflation eroded purchasing power, particularly hurting urban workers and fixed-income earners, while benefiting certain export sectors whose costs were in devalued paper pesos.

The situation in 1920 was a point of acute concern, prompting serious debate about monetary reform. The government recognized that restoring stability was essential for long-term investment and growth. While a definitive return to the gold standard was discussed, it was not immediately feasible given the global monetary uncertainty and the nation's depleted gold reserves. Consequently, 1920 represented a transitional and turbulent phase, setting the stage for the major monetary reforms that would follow later in the decade, culminating in the creation of the Bank of the Republic (Banco de la República) in 1924 and the eventual stabilization of the currency.

This period saw the emergence of a severe dual-currency system. The gold peso (peso oro), used for international transactions and as a stable unit of account, maintained its value. Meanwhile, the circulating paper peso (peso moneda nacional) depreciated significantly on the free market. This created immense complexity for commerce and banking, with prices, contracts, and debts often specified in one currency or the other, requiring constant conversion at fluctuating rates. The inflation eroded purchasing power, particularly hurting urban workers and fixed-income earners, while benefiting certain export sectors whose costs were in devalued paper pesos.

The situation in 1920 was a point of acute concern, prompting serious debate about monetary reform. The government recognized that restoring stability was essential for long-term investment and growth. While a definitive return to the gold standard was discussed, it was not immediately feasible given the global monetary uncertainty and the nation's depleted gold reserves. Consequently, 1920 represented a transitional and turbulent phase, setting the stage for the major monetary reforms that would follow later in the decade, culminating in the creation of the Bank of the Republic (Banco de la República) in 1924 and the eventual stabilization of the currency.

🌱 Fairly Common