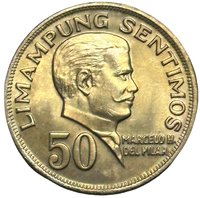

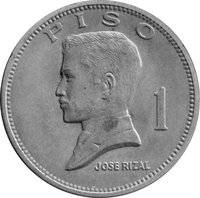

10 sentimos – Philippines

Add to wishlist

Philippines

Context

Years: 1967–1974

Issuer: Philippines

Issuing organization: Central Bank of the Philippines

Period:

(since 1946)

Currency:

(since 1967)

Demonetization: 2 January 1998

Total mintage: 461,608,000

Material

References

KM: #

Numista: #3752

Value

Exchange value: 0.10 PHP

Obverse

Reverse

Edge

Reeded

Categories

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| United States Mint of Denver | — |

| United States Mint of San Francisco | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1967 | — | 50,000,000 | ||

| 1968 | — | 60,000,000 | ||

| 1969 | — | 40,000,000 | ||

| 1970 | — | 50,000,000 | ||

| 1971 | — | 80,000,000 | ||

| 1972 | — | 121,390,000 | ||

| 1974 | — | 10,000 | Proof | |

| 1974 | — | 60,208,000 |

Historical background

In 1967, the Philippines operated under a managed currency system with the Philippine peso (₱) pegged to the United States dollar at a fixed rate of 2 pesos to 1 dollar. This arrangement was a legacy of the country's colonial history and its close post-war economic ties with the US, formalized under the Bretton Woods system. The Central Bank of the Philippines, established in 1949, was responsible for maintaining this peg, which provided notable stability for foreign trade and investment. However, this fixed exchange rate also constrained monetary policy and required significant reserves of foreign currency, primarily US dollars, to defend the official rate.

The economy during this period was facing underlying pressures that would later challenge the currency regime. President Ferdinand Marcos, in his first term, pursued an aggressive program of infrastructure spending and industrialization, funded by increasing government debt and a growing money supply. While the peso appeared stable on the surface, inflationary pressures were building, and the country's balance of payments position was becoming precarious. The trade deficit was widening as imports for development projects surged, steadily eroding the foreign exchange reserves needed to maintain the peso's dollar peg.

Consequently, 1967 represented the calm before a significant monetary storm. The rigid 2:1 peg, while a symbol of stability, was growing increasingly disconnected from the economic realities of rising debt and trade imbalances. These mounting pressures would culminate just three years later, in 1970, when the Philippines was forced to devalue the peso and shift to a floating exchange rate system, marking the end of this era of fixed parity. Thus, 1967 can be seen as the final chapter of a seemingly stable but ultimately unsustainable currency policy.

The economy during this period was facing underlying pressures that would later challenge the currency regime. President Ferdinand Marcos, in his first term, pursued an aggressive program of infrastructure spending and industrialization, funded by increasing government debt and a growing money supply. While the peso appeared stable on the surface, inflationary pressures were building, and the country's balance of payments position was becoming precarious. The trade deficit was widening as imports for development projects surged, steadily eroding the foreign exchange reserves needed to maintain the peso's dollar peg.

Consequently, 1967 represented the calm before a significant monetary storm. The rigid 2:1 peg, while a symbol of stability, was growing increasingly disconnected from the economic realities of rising debt and trade imbalances. These mounting pressures would culminate just three years later, in 1970, when the Philippines was forced to devalue the peso and shift to a floating exchange rate system, marking the end of this era of fixed parity. Thus, 1967 can be seen as the final chapter of a seemingly stable but ultimately unsustainable currency policy.

Series: Pilipino Series

🌱 Very Common