100 Escudos – Portugal

Portugal

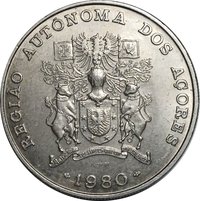

Obverse

Description:

Face value, Portugal's coat of arms.

Inscription:

REGIAO AUTONOMA DES ACORES 1980

Translation:

Autonomous Region of the Azores 1980

Script: Latin

Language: Portuguese

Reverse

Description:

Azores weaponry.

Inscription:

REPÚBLICA PORTUGUESA

100 ESCUDOS

AÇORES

100 ESCUDOS

AÇORES

Translation:

PORTUGUESE REPUBLIC

100 ESCUDOS

AZORES

100 ESCUDOS

AZORES

Script: Latin

Language: Portuguese

Edge

Locks

Mints

| Name | Mark |

|---|---|

| Imprensa Nacional - Casa da Moeda | incm |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1980 | — | 12,000 | Proof |

Historical background

In 1980, Portugal's currency situation was defined by the escudo navigating a complex period of economic transition and political change. Following the 1974 Carnation Revolution, the country grappled with the economic fallout of decolonization, nationalizations, and significant social upheaval, which led to high inflation, large public deficits, and a growing external debt. The escudo, while not freely convertible, was managed within a crawling peg system, where its value was periodically devalued against a basket of currencies to maintain export competitiveness, albeit at the cost of imported inflation.

This monetary policy occurred under the auspices of the International Monetary Fund (IMF), as Portugal had entered its first IMF stabilization program in 1977 and a second in 1978. These programs imposed strict austerity measures, including credit ceilings and fiscal discipline, in exchange for financial assistance to address balance of payments crises. Consequently, the Central Bank of Portugal's control over the escudo was heavily influenced by the need to meet IMF targets, limiting domestic policy flexibility and keeping interest rates high to attract foreign capital and support the currency.

Looking forward, the currency landscape was also being shaped by Portugal's geopolitical aspirations. Having applied for membership in the European Economic Community (EEC) in 1977, policymakers were already looking toward eventual European Monetary System (EMS) participation and the long-term goal of exchange rate stability within Europe. Thus, the escudo's management in 1980 was a balancing act between immediate crisis containment under IMF guidance and the nascent preparations for deeper European integration, which would ultimately redefine Portugal's monetary future.

This monetary policy occurred under the auspices of the International Monetary Fund (IMF), as Portugal had entered its first IMF stabilization program in 1977 and a second in 1978. These programs imposed strict austerity measures, including credit ceilings and fiscal discipline, in exchange for financial assistance to address balance of payments crises. Consequently, the Central Bank of Portugal's control over the escudo was heavily influenced by the need to meet IMF targets, limiting domestic policy flexibility and keeping interest rates high to attract foreign capital and support the currency.

Looking forward, the currency landscape was also being shaped by Portugal's geopolitical aspirations. Having applied for membership in the European Economic Community (EEC) in 1977, policymakers were already looking toward eventual European Monetary System (EMS) participation and the long-term goal of exchange rate stability within Europe. Thus, the escudo's management in 1980 was a balancing act between immediate crisis containment under IMF guidance and the nascent preparations for deeper European integration, which would ultimately redefine Portugal's monetary future.

Series: System 1969-1980

⭐ Rare