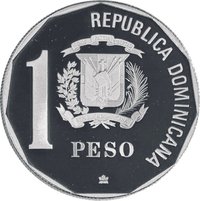

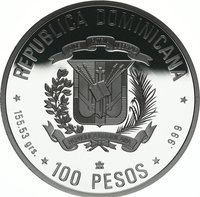

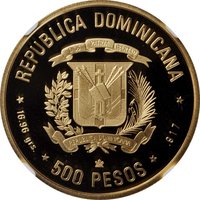

1 Peso – Dominican Republic

Non-circulating coins

Commemoration: Columbus' Presentation of an Amerindian

Dominican Republic

Context

Material

References

KM: #Click to copy to clipboardP37

Numista: #365956

Value

Exchange value: 1 DOP

Bullion value: $119.25

Obverse

Reverse

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Royal Canadian Mint of Ottawa | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1990 | — | — | Proof |

Historical background

In 1990, the Dominican Republic was navigating a fragile economic recovery under President Joaquín Balaguer, who had returned to power in 1986. The decade prior had been marked by severe crisis, characterized by high inflation, stagnant growth, and a heavy burden of external debt. By 1990, the country was operating under a stabilization program agreed with the International Monetary Fund (IMF), which aimed to correct macroeconomic imbalances. A central feature of this program was a managed exchange rate regime for the Dominican peso, which was pegged to the US dollar but subject to periodic devaluations to address overvaluation and boost exports.

The currency situation was one of controlled tension. The official exchange rate was fixed by the Central Bank, but a significant parallel black market for US dollars thrived, reflecting persistent pressure on the peso and a lack of confidence in the official policy. This duality created distortions, with the black market rate often significantly higher than the official rate, encouraging capital flight and complicating business operations. The government's focus was on maintaining stability through strict fiscal and monetary measures to curb inflation, which had been rampant in the 1980s but was being gradually tamed.

Overall, 1990 represented a transitional year where the foundations for future relative stability were being laid, but at a social cost. The tight monetary policy and devaluation strategy succeeded in improving the trade balance and rebuilding foreign reserves, setting the stage for the economic liberalization and more flexible exchange rate mechanisms that would follow in the mid-1990s. However, for the average Dominican, the immediate reality was one of a constrained economy, with the complex dual currency system underscoring the challenges of transitioning from a period of profound crisis to one of tentative stabilization.

The currency situation was one of controlled tension. The official exchange rate was fixed by the Central Bank, but a significant parallel black market for US dollars thrived, reflecting persistent pressure on the peso and a lack of confidence in the official policy. This duality created distortions, with the black market rate often significantly higher than the official rate, encouraging capital flight and complicating business operations. The government's focus was on maintaining stability through strict fiscal and monetary measures to curb inflation, which had been rampant in the 1980s but was being gradually tamed.

Overall, 1990 represented a transitional year where the foundations for future relative stability were being laid, but at a social cost. The tight monetary policy and devaluation strategy succeeded in improving the trade balance and rebuilding foreign reserves, setting the stage for the economic liberalization and more flexible exchange rate mechanisms that would follow in the mid-1990s. However, for the average Dominican, the immediate reality was one of a constrained economy, with the complex dual currency system underscoring the challenges of transitioning from a period of profound crisis to one of tentative stabilization.

✨ Legendary