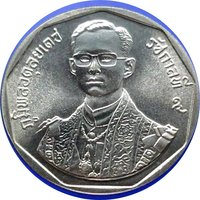

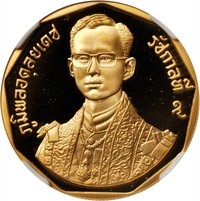

3000 Bahts (King Rama IX) – Thailand

Non-circulating coins

Commemoration: 42nd Anniversary - Reign of King Rama IX

Series: Rajamangala Celebrations

Thailand

Context

Year: 1989

Thai Year: 2531

Issuer: Thailand

Ruler: Bhumibol Adulyadej

Currency:

(since 1897)

Total mintage: 8,684

Material

References

Numista: #362221

Value

Exchange value: 3000 THB = $96.59

Bullion value: $1125.43

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1989 | — | 7,904 | ||

| 1989 | — | 780 | Proof |

Historical background

In 1989, Thailand's currency situation was characterized by a managed float of the baht, which was pegged to a basket of currencies dominated by the US dollar. This system, established in the early 1980s following a devaluation crisis, provided a crucial anchor for monetary stability and export competitiveness. The Bank of Thailand carefully managed the exchange rate within a narrow band, a policy that fostered confidence among foreign investors and supported the nation's rapidly expanding export-oriented economy, then in the midst of a historic boom often called the "Asian Tiger" period.

This period of stability, however, was beginning to encounter underlying pressures. Thailand's remarkable economic growth, averaging over 10% annually in the late 1980s, led to a large and growing current account deficit. This was fueled by strong domestic demand for imports and heavy capital investment in infrastructure and industry. Furthermore, the baht's close linkage to the appreciating US dollar made Thai exports relatively more expensive compared to those of competitors, subtly eroding the very competitiveness the peg was designed to ensure.

Consequently, 1989 stood as a pivotal calm before the storm. The managed peg was largely successful in its immediate goals, providing a stable financial environment for growth. Yet, the accumulating macroeconomic imbalances—the significant current account deficit, inflationary pressures, and the rigidity of the exchange rate—were creating vulnerabilities. These fault lines, though not yet causing crisis, would be dramatically exposed later in the 1990s when speculative pressures culminated in the 1997 Asian Financial Crisis, which forced the abandonment of the baht peg.

This period of stability, however, was beginning to encounter underlying pressures. Thailand's remarkable economic growth, averaging over 10% annually in the late 1980s, led to a large and growing current account deficit. This was fueled by strong domestic demand for imports and heavy capital investment in infrastructure and industry. Furthermore, the baht's close linkage to the appreciating US dollar made Thai exports relatively more expensive compared to those of competitors, subtly eroding the very competitiveness the peg was designed to ensure.

Consequently, 1989 stood as a pivotal calm before the storm. The managed peg was largely successful in its immediate goals, providing a stable financial environment for growth. Yet, the accumulating macroeconomic imbalances—the significant current account deficit, inflationary pressures, and the rigidity of the exchange rate—were creating vulnerabilities. These fault lines, though not yet causing crisis, would be dramatically exposed later in the 1990s when speculative pressures culminated in the 1997 Asian Financial Crisis, which forced the abandonment of the baht peg.

Series: Rajamangala Celebrations

✨ Legendary