600 Bahts (King Rama IX Reign) – Thailand

Non-circulating coins

Commemoration: 42nd Anniversary of Reign of King Rama IX

Series: Rajamangala Celebrations

Thailand

Context

Year: 1988

Thai Year: 2531

Issuer: Thailand

Ruler: Bhumibol Adulyadej

Currency:

(since 1897)

Total mintage: 9,950

Material

References

Y: #Click to copy to clipboard215

Numista: #190876

Value

Exchange value: 600 THB = $19.32

Bullion value: $78.88

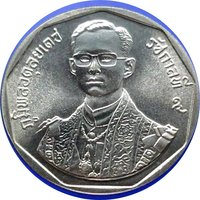

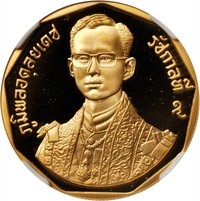

Obverse

Description:

King Rama IX statue

Script: Thai

Reverse

Description:

Crowned initials

Script: Thai

Edge

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1988 | — | 8,840 | ||

| 1988 | — | 1,110 | Proof |

Historical background

In 1988, Thailand's currency situation was characterized by relative stability and strength, underpinned by a period of robust economic growth and prudent monetary policy. The Thai baht (THB) was pegged to a basket of currencies, heavily weighted toward the US dollar, a managed exchange rate regime administered by the Bank of Thailand. This system provided predictability for trade and investment, which was crucial as Thailand was rapidly transforming into a newly industrialized economy, fueled by strong exports, foreign direct investment, and a burgeoning tourism sector. Inflation was under control, and the country's foreign exchange reserves were growing, reflecting a healthy balance of payments.

This stability, however, existed within a context of mounting external pressures and internal economic imbalances. Thailand's "economic miracle" led to a significant current account deficit, as the demand for imported capital goods and machinery to fuel industrialization outpaced export earnings. Furthermore, large-scale capital inflows, attracted by high domestic interest rates and a booming stock and property market, began to create challenges for monetary management. The fixed exchange rate peg, while stable, made the baht potentially vulnerable to speculative pressures if investor sentiment were to shift.

Consequently, 1988 stands as a pivotal calm before the storm. The apparent strength of the baht and the managed regime masked underlying vulnerabilities that would intensify in the coming years. The very success of the export-led growth model, combined with liberalized financial markets, was creating conditions of overheating and over-reliance on short-term foreign capital. These unresolved tensions would eventually culminate in the 1997 Asian Financial Crisis, which forced the abandonment of the baht peg. Thus, the currency situation in 1988 was one of surface-level stability, quietly setting the stage for a profound financial reckoning a decade later.

This stability, however, existed within a context of mounting external pressures and internal economic imbalances. Thailand's "economic miracle" led to a significant current account deficit, as the demand for imported capital goods and machinery to fuel industrialization outpaced export earnings. Furthermore, large-scale capital inflows, attracted by high domestic interest rates and a booming stock and property market, began to create challenges for monetary management. The fixed exchange rate peg, while stable, made the baht potentially vulnerable to speculative pressures if investor sentiment were to shift.

Consequently, 1988 stands as a pivotal calm before the storm. The apparent strength of the baht and the managed regime masked underlying vulnerabilities that would intensify in the coming years. The very success of the export-led growth model, combined with liberalized financial markets, was creating conditions of overheating and over-reliance on short-term foreign capital. These unresolved tensions would eventually culminate in the 1997 Asian Financial Crisis, which forced the abandonment of the baht peg. Thus, the currency situation in 1988 was one of surface-level stability, quietly setting the stage for a profound financial reckoning a decade later.

Series: Rajamangala Celebrations

✨ Legendary