10 milliemes – Egypt

Add to wishlist

Egypt

Context

Years: 1929–1935

Issuer: Egypt

Ruler: Ahmed Fuad I

Currency:

(since 1916)

Demonetized: Yes

Total mintage: 7,000,000

Material

Diameter: 23 mm

Weight: 5.3 g

Thickness: 1.58 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #10253

Value

Exchange value: 0.010 EGP

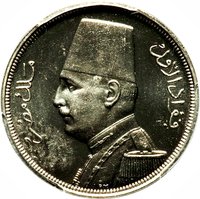

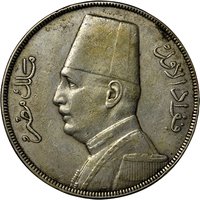

Obverse

Description:

Portrait of King Fuad I of Egypt in a fez, facing left.

Inscription:

فواد الأول

ملك مصر

ملك مصر

Translation:

Fuad I

King of Egypt

King of Egypt

Script: Arabic

Language: Arabic

Engraver: Percy Metcalfe

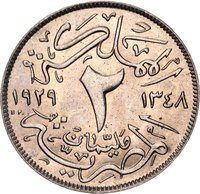

Reverse

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Hungarian mint | BP |

| Heaton and Sons / The Mint Birmingham | H |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1929 | — | 1,500,000 | ||

| 1933 | — | 1,500,000 | ||

| 1935 | — | 4,000,000 |

Historical background

In 1929, Egypt’s currency situation was defined by its adherence to the gold standard through the Egyptian pound (EE), which was pegged to and fully backed by British sterling. This system, formalized in the 1885 Currency Reform, ensured stability and facilitated trade, but it also tightly bound Egypt’s economy to that of Britain. The Egyptian pound was managed by the privately-owned National Bank of Egypt, which acted as the quasi-central bank, holding substantial sterling reserves in London to guarantee convertibility. This linkage provided credibility and attracted foreign investment, but it also meant that Egypt’s monetary policy was largely dictated by the Bank of England’s decisions, limiting autonomous economic management.

The year 1929 itself marked a critical juncture, as the global onset of the Great Depression began to expose the vulnerabilities of this dependent system. While the immediate shockwaves from the Wall Street Crash were somewhat buffered by Egypt’s agricultural export economy, the subsequent collapse in global commodity prices would soon have severe consequences. The sterling peg, while a source of prior stability, meant Egypt would import the deflationary pressures and economic contraction from Britain, with no independent mechanism to devalue its currency to boost exports.

Consequently, the period directly following 1929 set the stage for a severe economic crisis. The plummeting value of Egypt’s primary exports—cotton and agricultural products—led to a dramatic fall in national income and government revenue. Pressure on the pound grew as the trade balance deteriorated, testing the gold-standard convertibility. This unsustainable position would force Egypt to abandon the gold standard in 1931, shortly after Britain did so, culminating in the establishment of a central bank and a more managed currency system in the following decade.

The year 1929 itself marked a critical juncture, as the global onset of the Great Depression began to expose the vulnerabilities of this dependent system. While the immediate shockwaves from the Wall Street Crash were somewhat buffered by Egypt’s agricultural export economy, the subsequent collapse in global commodity prices would soon have severe consequences. The sterling peg, while a source of prior stability, meant Egypt would import the deflationary pressures and economic contraction from Britain, with no independent mechanism to devalue its currency to boost exports.

Consequently, the period directly following 1929 set the stage for a severe economic crisis. The plummeting value of Egypt’s primary exports—cotton and agricultural products—led to a dramatic fall in national income and government revenue. Pressure on the pound grew as the trade balance deteriorated, testing the gold-standard convertibility. This unsustainable position would force Egypt to abandon the gold standard in 1931, shortly after Britain did so, culminating in the establishment of a central bank and a more managed currency system in the following decade.

Series: 1929 Egypt circulation coins

🌱 Common