50 colones – Costa Rica

Add to wishlist

Costa Rica

Context

Years: 1997–1999

Issuer: Costa Rica

Issuing organization: Central Bank of Costa Rica

Period:

(since 1948)

Currency:

(since 1896)

Demonetization: 1 July 2025

Total mintage: 40,000,000

Material

Diameter: 27.5 mm

Weight: 7.8 g

Thickness: 1.95 mm

Shape: Round

Composition: Copper-aluminium-nickel

Standard: Silver quarter ounce

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #

Numista: #3590

Value

Exchange value: 50 CRC

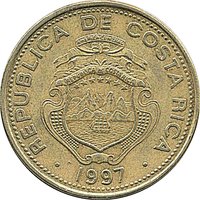

Obverse

Description:

Costa Rica's coat of arms features seven stars for its provinces, three volcanoes for its mountain ranges, two ships for its position between the Atlantic and Pacific, and a sunrise.

Inscription:

REPUBLICA DE COSTA RICA

AMERICA CENTRAL

REPUBLICA DE COSTA RICA

1997

AMERICA CENTRAL

REPUBLICA DE COSTA RICA

1997

Translation:

REPUBLIC OF COSTA RICA

CENTRAL AMERICA

REPUBLIC OF COSTA RICA

1997

CENTRAL AMERICA

REPUBLIC OF COSTA RICA

1997

Script: Latin

Language: Spanish

Reverse

Edge

Segmented (4 smooth, 4 milled)

Categories

| Geography> Mountain |

| Symbols> Coat of Arms |

| Symbol> Wreath |

| Transportation> Watercraft |

Mints

| Name | Mark |

|---|---|

| Casa de Moneda de Chile | — |

| Fábrica de Moneda de Ibagué | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1997 | — | 15,000,000 | ||

| 1999 | — | 25,000,000 |

Historical background

In 1997, Costa Rica's currency situation was characterized by a managed exchange rate regime facing significant external pressures. The country operated a crawling peg system for the colón, where the Central Bank (BCCR) would allow the currency to depreciate at a pre-announced, gradual rate (the deslizamiento) to maintain export competitiveness and manage inflation. This system had provided relative stability since the early 1990s, but by 1997, it was being tested by a growing current account deficit and substantial capital inflows, which complicated monetary policy.

The primary challenges stemmed from a combination of large-scale foreign direct investment (FDI), particularly into the booming electronics and tourism sectors, and rising public sector borrowing. These capital inflows created upward pressure on the colón, contradicting the BCCR's depreciation targets. To maintain the crawling peg, the Bank was forced to intervene heavily in the foreign exchange market, purchasing dollars and expanding the money supply. This contributed to inflationary pressures and raised concerns about the sustainability of the peg, as international reserves experienced volatility.

Consequently, 1997 was a year of transition and debate. The tensions within the managed system highlighted its limitations in a climate of financial globalization and set the stage for future reforms. While the crawling peg was maintained throughout the year, the accumulating imbalances and policy dilemmas paved the way for the more significant liberalization measures that would follow, including the move towards a crawling band system in 1999 and greater exchange rate flexibility in the early 2000s.

The primary challenges stemmed from a combination of large-scale foreign direct investment (FDI), particularly into the booming electronics and tourism sectors, and rising public sector borrowing. These capital inflows created upward pressure on the colón, contradicting the BCCR's depreciation targets. To maintain the crawling peg, the Bank was forced to intervene heavily in the foreign exchange market, purchasing dollars and expanding the money supply. This contributed to inflationary pressures and raised concerns about the sustainability of the peg, as international reserves experienced volatility.

Consequently, 1997 was a year of transition and debate. The tensions within the managed system highlighted its limitations in a climate of financial globalization and set the stage for future reforms. While the crawling peg was maintained throughout the year, the accumulating imbalances and policy dilemmas paved the way for the more significant liberalization measures that would follow, including the move towards a crawling band system in 1999 and greater exchange rate flexibility in the early 2000s.

🌱 Very Common