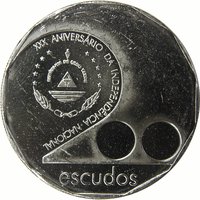

200 escudos – Cape Verde

Add to wishlist

Circulating commemorative coins

Commemoration: Entry into the World Trade Organization

Cape Verde

Context

Material

Diameter: 30 mm

Weight: 18 g

Thickness: 2.3 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #35478

Value

Exchange value: 200 CVE

Obverse

Inscription:

2008

200 ESCUDOS

RÉPUBLICA DE CABO VERDE

200 ESCUDOS

RÉPUBLICA DE CABO VERDE

Translation:

2008

200 ESCUDOS

REPUBLIC OF CAPE VERDE

200 ESCUDOS

REPUBLIC OF CAPE VERDE

Script: Latin

Language: Portuguese

Reverse

Inscription:

2008 · ADESAO A ORGANIZACAO MUNDIAL DO COMÉRCIO

Translation:

2008 · Accession to the World Trade Organization

Script: Latin

Language: Portuguese

Edge

Reeded

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2008 | — | 2,000 | ||

| 2008 | — | — | Proof |

Historical background

In 2008, Cape Verde's currency situation was defined by its long-standing and strategic peg to the euro. The country's currency, the Cape Verdean escudo (CVE), had been pegged first to the Portuguese escudo and then, since 1999, firmly fixed to the euro at a rate of 110.265 CVE to 1 euro. This arrangement was managed through a cooperation agreement with Portugal, which guaranteed convertibility and provided a crucial anchor for monetary stability and economic policy. For a small, open island nation reliant on tourism, remittances, and foreign aid, this peg was instrumental in controlling inflation, attracting foreign investment, and reducing exchange rate risk for key sectors.

The global financial crisis of 2008 presented a significant external test to this system. While the direct exposure of Cape Verde's banking sector to toxic international assets was limited, the crisis threatened its economy through secondary channels: a potential downturn in European tourism and a possible reduction in remittance flows from its large diaspora in Europe and the United States. These factors risked reducing foreign currency inflows, which were essential for maintaining the fixed exchange rate and financing the country's substantial trade deficit. The peg, therefore, placed a premium on maintaining prudent fiscal reserves and external competitiveness.

Despite the global turmoil, Cape Verde successfully maintained its currency peg throughout 2008, a testament to the perceived strength of its institutional framework and its consistent record of fiscal discipline. The fixed exchange rate was viewed not just as a monetary tool, but as a cornerstone of the country's overall economic stability and its integration with the European Union, its main trading and development partner. Consequently, the central focus of monetary policy remained unwavering support for the peg, with domestic interest rates largely aligned with those of the European Central Bank to prevent destabilizing capital flows, even as the world economy entered a profound recession.

The global financial crisis of 2008 presented a significant external test to this system. While the direct exposure of Cape Verde's banking sector to toxic international assets was limited, the crisis threatened its economy through secondary channels: a potential downturn in European tourism and a possible reduction in remittance flows from its large diaspora in Europe and the United States. These factors risked reducing foreign currency inflows, which were essential for maintaining the fixed exchange rate and financing the country's substantial trade deficit. The peg, therefore, placed a premium on maintaining prudent fiscal reserves and external competitiveness.

Despite the global turmoil, Cape Verde successfully maintained its currency peg throughout 2008, a testament to the perceived strength of its institutional framework and its consistent record of fiscal discipline. The fixed exchange rate was viewed not just as a monetary tool, but as a cornerstone of the country's overall economic stability and its integration with the European Union, its main trading and development partner. Consequently, the central focus of monetary policy remained unwavering support for the peg, with domestic interest rates largely aligned with those of the European Central Bank to prevent destabilizing capital flows, even as the world economy entered a profound recession.

🌟 Uncommon