200 escudos (Independence of Cape Verde) – Cape Verde

Add to wishlist

Circulating commemorative coins

Commemoration: 30th Anniversary of the Independence of Cape Verde

Cape Verde

Context

Material

Diameter: 29.5 mm

Weight: 18.05 g

Thickness: 3.5 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #11928

Value

Exchange value: 200 CVE

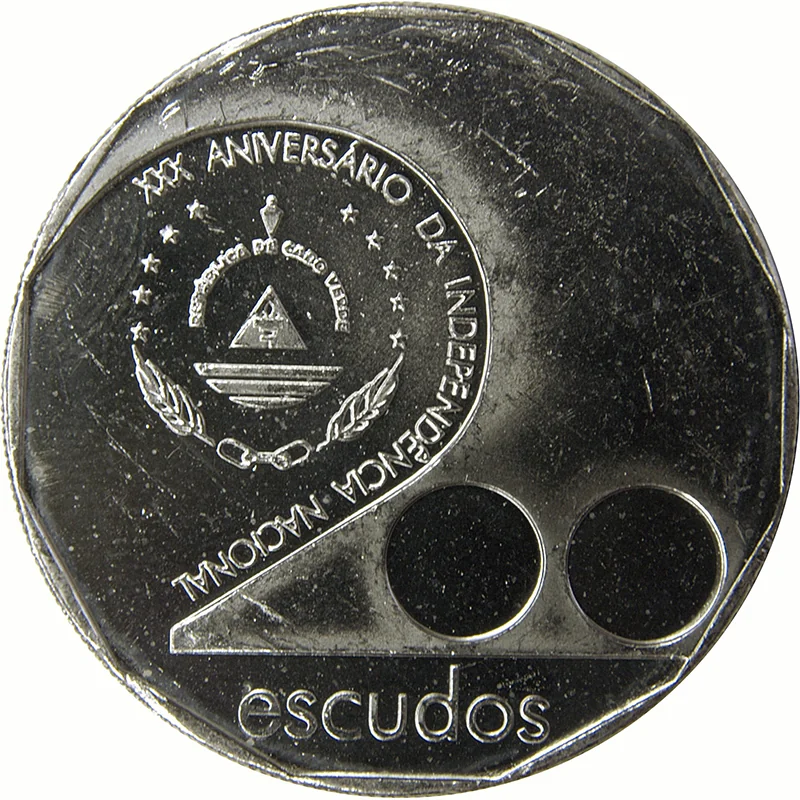

Obverse

Description:

National emblem, Article 2 of 200.

Inscription:

XXX ANIVERSARIO DA INDEPENDENCIA NACIONAL

200

escudos

200

escudos

Translation:

Thirtieth Anniversary of National Independence

200

Escudos

200

Escudos

Script: Latin

Language: Portuguese

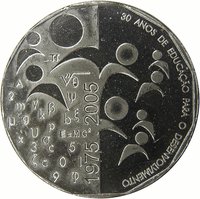

Reverse

Description:

Symbolic learning design

Inscription:

30 ANOS DE EDUCACAO PARA O DESENVOLVIMENTO

1975 2005

1975 2005

Translation:

30 Years of Education for Development

1975 2005

1975 2005

Script: Latin

Language: Portuguese

Edge

Reeded

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2005 | — | — |

Historical background

In 2005, the currency situation in Cape Verde was defined by a pivotal and successful monetary policy framework: the escudo (CVE) was pegged to the euro at a fixed and stable rate of 110.265 CVE to 1 EUR. This arrangement, established in 1999 following Portugal's adoption of the euro, replaced the previous peg to the Portuguese escudo. The peg was not merely a technicality but a cornerstone of national economic strategy, providing critical stability for an import-dependent island nation with a small, open economy. It anchored inflation, fostered investor confidence, and facilitated predictable transactions for the vital tourism sector and a large diaspora sending remittances.

This stability was hard-won and actively managed. The peg was backed by substantial foreign exchange reserves, which the Banco de Cabo Verde (BCV) diligently maintained, often exceeding six months of import cover. Monetary policy was entirely subordinated to defending the fixed exchange rate, meaning the BCV's primary tool was adjusting interest rates to manage liquidity and ensure the escudo's credibility. This discipline, supported by prudent fiscal policies and structural reforms, had successfully tamed the high inflation of previous decades, with rates falling to low single digits by the mid-2000s.

Consequently, the dominant narrative in 2005 was one of consolidation and confidence. The escudo was considered a bedrock of macroeconomic stability, a significant achievement that distinguished Cape Verde from many of its regional peers. Discussions were less about currency crisis and more about leveraging this stability for further development. The government and central bank were focused on maintaining the discipline required for the peg while exploring avenues for sustainable growth, a policy track that would soon lead to Cape Verde's graduation from Least Developed Country status in 2007. The fixed exchange rate was the linchpin of its economic credibility.

This stability was hard-won and actively managed. The peg was backed by substantial foreign exchange reserves, which the Banco de Cabo Verde (BCV) diligently maintained, often exceeding six months of import cover. Monetary policy was entirely subordinated to defending the fixed exchange rate, meaning the BCV's primary tool was adjusting interest rates to manage liquidity and ensure the escudo's credibility. This discipline, supported by prudent fiscal policies and structural reforms, had successfully tamed the high inflation of previous decades, with rates falling to low single digits by the mid-2000s.

Consequently, the dominant narrative in 2005 was one of consolidation and confidence. The escudo was considered a bedrock of macroeconomic stability, a significant achievement that distinguished Cape Verde from many of its regional peers. Discussions were less about currency crisis and more about leveraging this stability for further development. The government and central bank were focused on maintaining the discipline required for the peg while exploring avenues for sustainable growth, a policy track that would soon lead to Cape Verde's graduation from Least Developed Country status in 2007. The fixed exchange rate was the linchpin of its economic credibility.

🌟 Uncommon