1000 pesos – Colombia

Add to wishlist

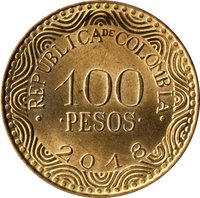

Colombia

Context

Years: 2012–2024

Issuer: Colombia

Period:

(since 1886)

Currency:

(since 1847)

Total mintage: 1,616,100,000

Material

Diameter: 26.7 mm

Weight: 9.95 g

Thickness: 2.7 mm

Shape: Round

Techniques: Latent image, Milled

Alignment: Coin alignment

flip

References

KM: #

Numista: #34775

Value

Exchange value: 1000 COP

Inflation-adjusted value: 1957.36 COP

Obverse

Description:

Country above value, date below. Latent center image shifts between "BRC" and "MIL". Microtext at bottom repeats "Take care of the water" upright and inverted.

Inscription:

· REPUBLICA DE COLOMBIA ·

1000

·PESOS·

B.R.C.

MIL

·CUIDAR EL AGUA·CUIDAR EL AGUA·CUIDAR EL AGUA·CUIDAR EL AGUA·

2015

1000

·PESOS·

B.R.C.

MIL

·CUIDAR EL AGUA·CUIDAR EL AGUA·CUIDAR EL AGUA·CUIDAR EL AGUA·

2015

Translation:

REPUBLIC OF COLOMBIA

1000

PESOS

B.R.C.

ONE THOUSAND

SAVE WATER SAVE WATER SAVE WATER SAVE WATER

2015

1000

PESOS

B.R.C.

ONE THOUSAND

SAVE WATER SAVE WATER SAVE WATER SAVE WATER

2015

Script: Latin

Language: Spanish

Engraver: José Antonio Suárez

Reverse

Description:

Loggerhead turtle facing right. Microtext "Water" repeats along the bottom, alternating upright and inverted.

Inscription:

·AGUA·AGUA·AGUA·AGUA·AGUA·AGUA·AGUA

TORTUGA·CAGUAMA

caretta caretta

TORTUGA·CAGUAMA

caretta caretta

Translation:

Water, Water, Water, Water, Water, Water, Water

Turtle, Loggerhead Turtle

Loggerhead Turtle

Turtle, Loggerhead Turtle

Loggerhead Turtle

Script: Latin

Engraver: José Antonio Suárez

Edge

Reeded security edge

Categories

| Animal> Turtle or tortoise |

Mints

| Name | Mark |

|---|---|

| Fábrica de Moneda de Ibagué | — |

| Kremnica | — |

| Mint of Finland | — |

| Mint of Poland | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2012 | — | 27,000,000 | ||

| 2013 | — | 90,700,000 | ||

| 2014 | — | 120,000,000 | ||

| 2015 | — | 167,828,000 | ||

| 2016 | — | 284,772,000 | ||

| 2017 | — | 140,900,000 | ||

| 2018 | — | 17,900,000 | ||

| 2019 | — | 153,700,000 | ||

| 2020 | — | 75,900,000 | ||

| 2021 | — | 53,200,000 | ||

| 2022 | — | 85,000,000 | ||

| 2023 | — | 232,700,000 | ||

| 2024 | — | 166,500,000 |

Historical background

In 2012, Colombia's currency situation was characterized by a period of significant and sustained appreciation of the Colombian peso (COP) against the US dollar, a trend that had been building since 2009. The peso strengthened to around 1,800 COP per USD, a level not seen in years, driven primarily by high global commodity prices, particularly for oil and coal, which are Colombia's chief exports. This influx of foreign currency was compounded by substantial foreign direct investment (FDI) flowing into the country's booming mining and energy sectors, as well as portfolio investment attracted by Colombia's strong economic growth and rising investment-grade credit ratings.

The strong peso created a complex economic dilemma. While it helped keep inflation low (around 3% for the year) and made imports cheaper, it severely hurt the competitiveness of non-commodity exporters, such as manufacturers, flower growers, and the coffee sector. Industries complained of shrinking profit margins and lost market share, leading to calls for government intervention. Furthermore, the appreciation raised concerns about "Dutch disease," where a resource-driven currency surge undermines other productive sectors of the economy, threatening long-term, diversified growth.

In response, the government and the Central Bank (Banco de la República) implemented a multi-pronged strategy to curb the peso's rise. The most notable measure was a daily dollar purchasing program, initiated in February 2012, where the Bank accumulated foreign reserves to increase demand for dollars. Additionally, the government mandated that state-owned oil company Ecopetrol and private pension funds keep a larger share of their assets abroad. These interventions aimed to moderate the pace of appreciation, provide stability, and alleviate pressure on exporters, reflecting a cautious approach to managing the side effects of robust economic inflows.

The strong peso created a complex economic dilemma. While it helped keep inflation low (around 3% for the year) and made imports cheaper, it severely hurt the competitiveness of non-commodity exporters, such as manufacturers, flower growers, and the coffee sector. Industries complained of shrinking profit margins and lost market share, leading to calls for government intervention. Furthermore, the appreciation raised concerns about "Dutch disease," where a resource-driven currency surge undermines other productive sectors of the economy, threatening long-term, diversified growth.

In response, the government and the Central Bank (Banco de la República) implemented a multi-pronged strategy to curb the peso's rise. The most notable measure was a daily dollar purchasing program, initiated in February 2012, where the Bank accumulated foreign reserves to increase demand for dollars. Additionally, the government mandated that state-owned oil company Ecopetrol and private pension funds keep a larger share of their assets abroad. These interventions aimed to moderate the pace of appreciation, provide stability, and alleviate pressure on exporters, reflecting a cautious approach to managing the side effects of robust economic inflows.

Series: 2012 Colombia circulation coins

🌱 Very Common