1 pound – Jersey

Add to wishlist

Context

Year: 1983

Country: British Crown dependencies

Issuer: Jersey

Ruler: Elizabeth II

Currency:

(since 1971)

Demonetized: Yes

Total mintage: 773

Material

References

KM: #

Numista: #346627

Value

Exchange value: 1 JEP

Bullion value: $2768.25

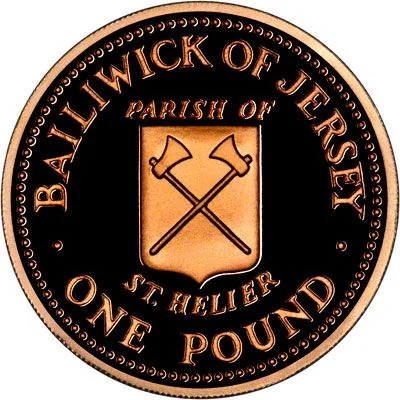

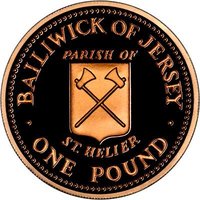

Obverse

Description:

Queen Elizabeth II in profile, wearing the Girls of Great Britain tiara.

Inscription:

QUEEN ELIZABETH THE SECOND

1983

1983

Script: Latin

Engraver: Arnold Machin

Reverse

Description:

Shield of St. Helier with crossed axes.

Inscription:

BAILIWICK OF JERSEY

PARISH OF

ST. HELIER

· ONE POUND ·

PARISH OF

ST. HELIER

· ONE POUND ·

Script: Latin

Edge

Milled with inscription

Legend:

CAESAREA INSULA

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1983 | — | 773 | Proof |

Historical background

In 1983, the currency situation in Jersey was characterised by its continued use of the Jersey pound, which operated in a long-standing one-to-one parity with the British pound sterling. As a British Crown Dependency, Jersey was not part of the United Kingdom, but its economy and banking system were deeply integrated with Britain's. The island issued its own banknotes and coins, which were legal tender only in Jersey, while UK sterling notes and coins also circulated freely and were accepted interchangeably. This system provided stability but meant Jersey's monetary policy was effectively set by the Bank of England, with no independent mechanism to address local economic conditions.

The period was one of economic transition for the island. Jersey was actively developing its finance sector, moving beyond its traditional agricultural and tourism bases. This growth increased the volume and complexity of financial transactions, all conducted in sterling. There was no serious consideration of deviating from the sterling link, as it provided crucial confidence for the burgeoning banking and trust industries, which relied on the stability and international recognition of the UK currency. The fixed parity was a cornerstone of Jersey's economic identity.

However, the arrangement also meant Jersey was exposed to UK monetary conditions, including the high interest rates of the early 1980s used to combat inflation in Britain. While these policies were designed for the UK economy, they directly impacted borrowing costs in Jersey, affecting local businesses and mortgages. This highlighted the inherent tension in the currency union: it offered stability and convenience but at the cost of ceding monetary sovereignty. By 1983, this was a settled and largely unchallenged reality, forming the bedrock upon which Jersey's modern financial centre would be built.

The period was one of economic transition for the island. Jersey was actively developing its finance sector, moving beyond its traditional agricultural and tourism bases. This growth increased the volume and complexity of financial transactions, all conducted in sterling. There was no serious consideration of deviating from the sterling link, as it provided crucial confidence for the burgeoning banking and trust industries, which relied on the stability and international recognition of the UK currency. The fixed parity was a cornerstone of Jersey's economic identity.

However, the arrangement also meant Jersey was exposed to UK monetary conditions, including the high interest rates of the early 1980s used to combat inflation in Britain. While these policies were designed for the UK economy, they directly impacted borrowing costs in Jersey, affecting local businesses and mortgages. This highlighted the inherent tension in the currency union: it offered stability and convenience but at the cost of ceding monetary sovereignty. By 1983, this was a settled and largely unchallenged reality, forming the bedrock upon which Jersey's modern financial centre would be built.

Series: Parishes of Jersey

✨ Legendary