30 dollars – Canada

Add to wishlist

Canada

Context

Material

Diameter: 16 mm

Weight: 3.11 g

Platinum Weight:: 3.11 g

Thickness: 1.08 mm

Shape: Round

Composition: 99.95% Platinum

Standard: Gold tenth ounce

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #346522

Value

Exchange value: 30 CAD

Bullion value: $208.77

Inflation-adjusted value: 54.60 CAD

Obverse

Description:

Queen Elizabeth II at 64, wearing the royal diadem and jewels, facing right.

Inscription:

ELIZABETH II D•G•REGINA

1997

1997

Translation:

Elizabeth II, by the Grace of God, Queen

1997

1997

Script: Latin

Language: Latin

Designer and engraver: Dora de Pédery-Hunt

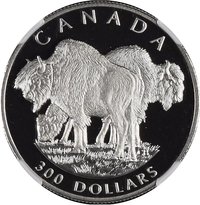

Reverse

Description:

Bison facing right, value beneath.

Inscription:

CANADA

30 DOLLARS

CB

30 DOLLARS

CB

Script: Latin

Engraver: Ago Aarand

Designer: Chris Bacon

Edge

Serrated

Mints

| Name | Mark |

|---|---|

| Royal Canadian Mint of Ottawa | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1997 | — | 469 | Proof |

Historical background

In 1997, Canada's currency situation was characterized by a period of significant weakness and heightened concern, with the Canadian dollar reaching a historic low. Throughout the year, the dollar, often colloquially called the "loonie" following the introduction of the one-dollar coin in 1987, traded at record depths against the United States dollar, briefly dipping below 69 cents US in August. This decline was part of a multi-year downtrend that had begun in the early 1990s, fueled by market perceptions of high government debt, relatively high inflation and interest rates compared to the U.S., and political uncertainty surrounding Quebec sovereignty.

The low dollar presented a classic double-edged sword for the Canadian economy. On one hand, it provided a substantial boost to the export-oriented sectors, particularly manufacturers and natural resource industries like forestry and mining, by making their goods cheaper and more competitive on the international market. This export strength was a key pillar of economic growth during the period. On the other hand, the weak currency increased the cost of imports, contributing to higher consumer prices and putting pressure on inflation. It also raised the cost of servicing Canada's substantial foreign-denominated debt.

By late 1997, the currency's fortunes began to stabilize and reverse course. This shift was driven by several factors: a marked improvement in the federal fiscal situation as the government moved toward a surplus, a narrowing interest rate differential with the U.S., and a general "flight to quality" during the Asian Financial Crisis which benefited stable economies like Canada's. Consequently, the loonie embarked on a recovery in the final quarter, closing the year near 71 cents US and setting the stage for a sustained, though gradual, appreciation over the following decade.

The low dollar presented a classic double-edged sword for the Canadian economy. On one hand, it provided a substantial boost to the export-oriented sectors, particularly manufacturers and natural resource industries like forestry and mining, by making their goods cheaper and more competitive on the international market. This export strength was a key pillar of economic growth during the period. On the other hand, the weak currency increased the cost of imports, contributing to higher consumer prices and putting pressure on inflation. It also raised the cost of servicing Canada's substantial foreign-denominated debt.

By late 1997, the currency's fortunes began to stabilize and reverse course. This shift was driven by several factors: a marked improvement in the federal fiscal situation as the government moved toward a surplus, a narrowing interest rate differential with the U.S., and a general "flight to quality" during the Asian Financial Crisis which benefited stable economies like Canada's. Consequently, the loonie embarked on a recovery in the final quarter, closing the year near 71 cents US and setting the stage for a sustained, though gradual, appreciation over the following decade.

Series: Canadian Wildlife platinum

✨ Legendary