5 Yuan – People's Republic of China

Circulating commemorative coins

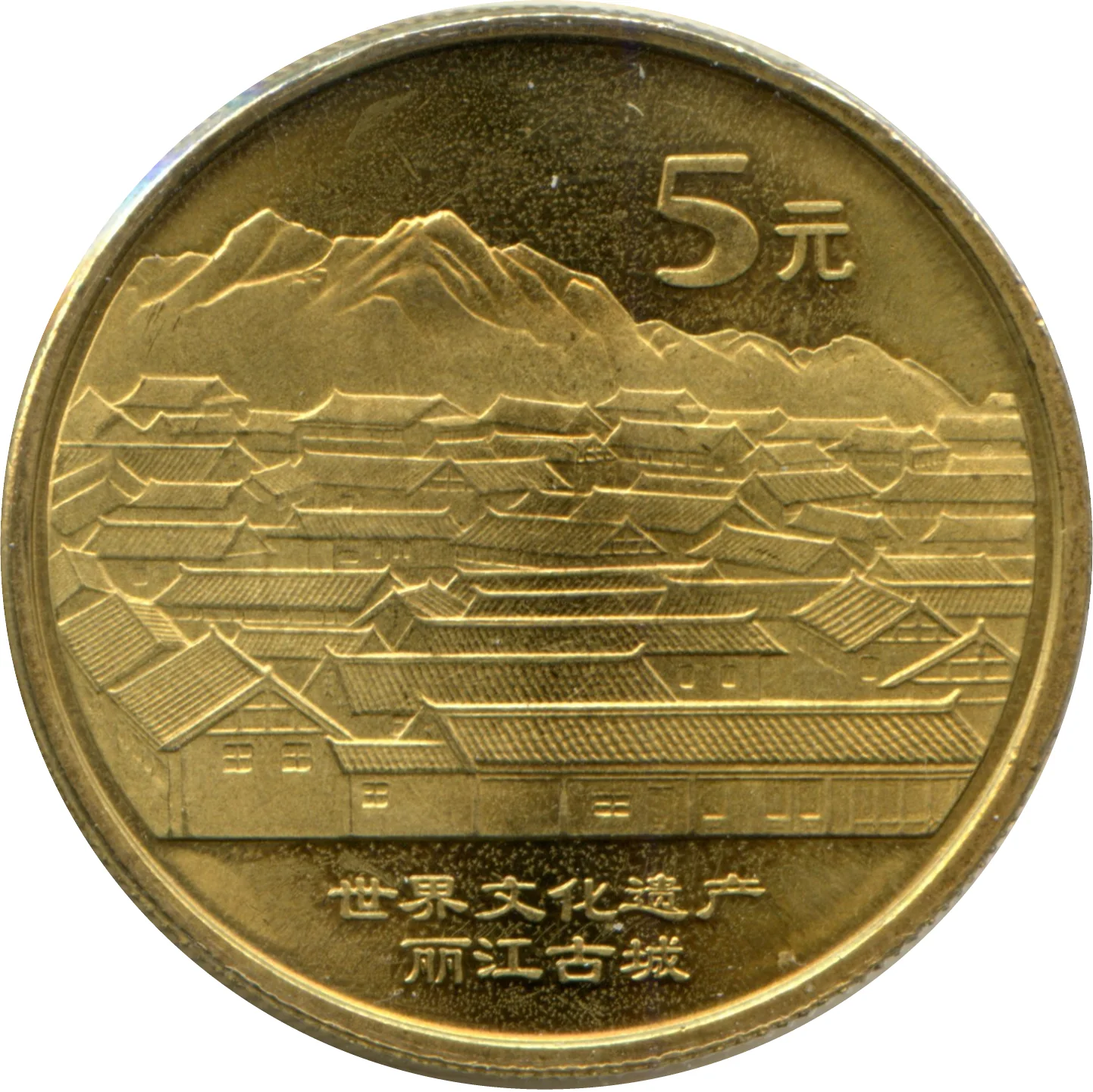

Commemoration: 1st edition - Lijiang Old Town

Series: UNESCO World Heritage

China

Context

Year: 2005

Country: China

Issuer: People's Republic of China

Period:

(since 1949)

Currency:

(since 1955)

Material

References

KM: #Click to copy to clipboard1576

Numista: #13893

Value

Exchange value: 5 CNY = $0.73

Inflation-adjusted value: 7.75 CNY

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2005 | — | — |

Historical background

In 2005, the People's Republic of China stood at a critical juncture in its monetary policy, characterized by intense international pressure and complex domestic economic considerations. Since 1994, China had maintained a de facto peg of its currency, the renminbi (RMB), to the US dollar at approximately 8.28. This policy provided stability for its export-driven growth model, fueling a massive accumulation of foreign exchange reserves and a sustained trade surplus, particularly with the United States. However, by the early 2000s, this fixed exchange rate was widely criticized by major trading partners and international institutions, which argued it was artificially undervalued, granting Chinese exports an unfair advantage and contributing to global economic imbalances.

Domestically, the situation presented a dual challenge. On one hand, maintaining the peg required constant intervention by the People's Bank of China (PBOC) to purchase incoming foreign currency, which contributed to excessive growth in the domestic money supply and heightened risks of inflation and asset bubbles. On the other hand, Chinese authorities were cautious about moving too quickly, fearing that a sharp appreciation could hurt the vast export sector, potentially causing widespread job losses and social instability. The government's primary goal was to manage the exchange rate in a controlled manner that supported macroeconomic stability and allowed its financial sector time to develop before facing full market pressures.

The pivotal moment arrived on July 21, 2005. The PBOC announced a landmark reform: revaluing the RMB by 2.1% against the dollar and, more importantly, abandoning the strict dollar peg in favor of a managed float system. The new regime referenced a basket of currencies and allowed the RMB to fluctuate within a narrow band daily. This carefully calibrated move was designed to appease international critics while asserting China's sovereign control over the pace of reform. The 2005 revaluation initiated a gradual, managed appreciation of the RMB that would continue for the next decade, marking China's cautious but definitive step towards integrating its currency into the global financial system.

Domestically, the situation presented a dual challenge. On one hand, maintaining the peg required constant intervention by the People's Bank of China (PBOC) to purchase incoming foreign currency, which contributed to excessive growth in the domestic money supply and heightened risks of inflation and asset bubbles. On the other hand, Chinese authorities were cautious about moving too quickly, fearing that a sharp appreciation could hurt the vast export sector, potentially causing widespread job losses and social instability. The government's primary goal was to manage the exchange rate in a controlled manner that supported macroeconomic stability and allowed its financial sector time to develop before facing full market pressures.

The pivotal moment arrived on July 21, 2005. The PBOC announced a landmark reform: revaluing the RMB by 2.1% against the dollar and, more importantly, abandoning the strict dollar peg in favor of a managed float system. The new regime referenced a basket of currencies and allowed the RMB to fluctuate within a narrow band daily. This carefully calibrated move was designed to appease international critics while asserting China's sovereign control over the pace of reform. The 2005 revaluation initiated a gradual, managed appreciation of the RMB that would continue for the next decade, marking China's cautious but definitive step towards integrating its currency into the global financial system.

Series: UNESCO World Heritage

🌟 Uncommon