10 Shillings – Kenya

Kenya

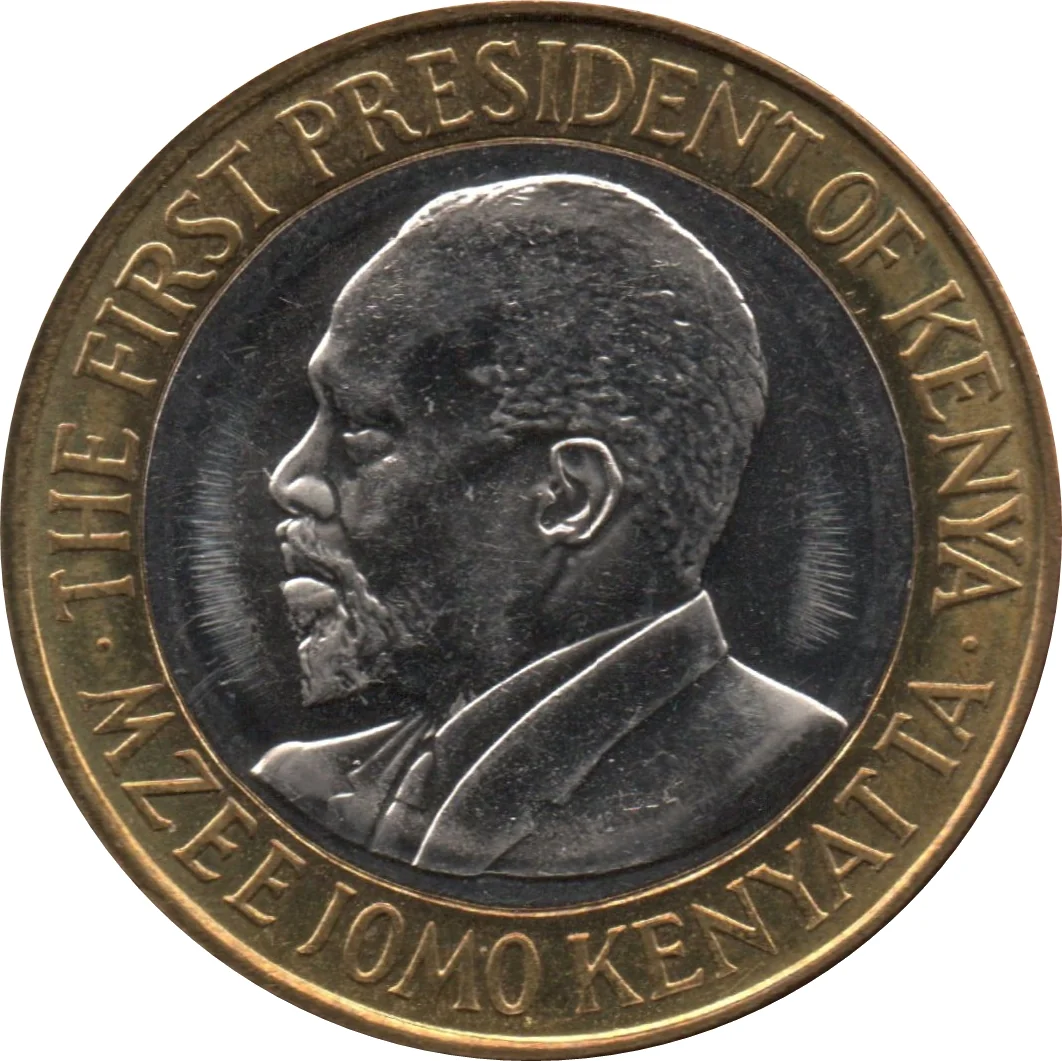

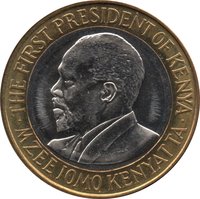

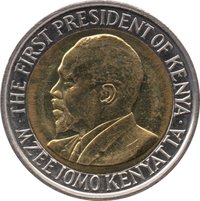

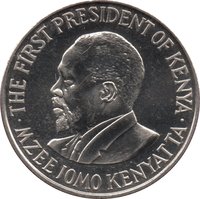

Obverse

Reverse

Description:

Bust of Jomo Kenyatta, left profile.

Inscription:

THE FIRST PRESIDENT OF KENYA

· MZEE JOMO KENYATTA ·

· MZEE JOMO KENYATTA ·

Script: Latin

Edge

Reeded

Categories

| Person> Politician |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2010 | — | — |

Historical background

In 2010, Kenya's currency situation was characterized by significant volatility and depreciation of the Kenyan Shilling (KES). The year began with relative stability, with the shilling trading at around KSh 75 to the US dollar. However, mounting internal and external pressures soon triggered a downward trend. Key factors included a widening current account deficit, driven by high global prices for imported oil and a surge in non-essential imports following a period of economic recovery from the 2007-2008 post-election crisis. This created a high demand for foreign currency that outpaced supply from key exports like tea, horticulture, and tourism.

The Central Bank of Kenya (CBK) initially pursued a policy of limited intervention, aiming to allow the shilling to find its market level and build foreign exchange reserves. However, the depreciation accelerated sharply in the second half of the year, stoking inflationary pressures by making imports more expensive. Speculative activity in the forex market exacerbated the slide, leading to public concern and political pressure for action. By October 2011, the shilling would hit a historic low of approximately KSh 107 to the dollar, though this peak was just beyond the 2010 timeframe.

Consequently, 2010 set the stage for a major policy shift. The CBK, under Governor Njuguna Ndung'u, began a more aggressive tightening cycle in late 2010, which would intensify in 2011. This included raising the Central Bank Rate (CBR) and introducing more direct measures to curb shilling liquidity and penalize speculative trading. Therefore, the currency situation in 2010 was a pivotal period of mounting strain that ultimately compelled the monetary authorities to abandon their relatively hands-off approach in favor of decisive intervention to stabilize the national currency.

The Central Bank of Kenya (CBK) initially pursued a policy of limited intervention, aiming to allow the shilling to find its market level and build foreign exchange reserves. However, the depreciation accelerated sharply in the second half of the year, stoking inflationary pressures by making imports more expensive. Speculative activity in the forex market exacerbated the slide, leading to public concern and political pressure for action. By October 2011, the shilling would hit a historic low of approximately KSh 107 to the dollar, though this peak was just beyond the 2010 timeframe.

Consequently, 2010 set the stage for a major policy shift. The CBK, under Governor Njuguna Ndung'u, began a more aggressive tightening cycle in late 2010, which would intensify in 2011. This included raising the Central Bank Rate (CBR) and introducing more direct measures to curb shilling liquidity and penalize speculative trading. Therefore, the currency situation in 2010 was a pivotal period of mounting strain that ultimately compelled the monetary authorities to abandon their relatively hands-off approach in favor of decisive intervention to stabilize the national currency.

🌱 Very Common