½ dollar – United States

Add to wishlist

United States

Context

Years: 1948–1963

Issuer: United States

Period:

(since 1776)

Currency:

(since 1785)

Subdivision: ½ dollar = 50 Cents

Total mintage: 484,141,139

Material

References

KM: #

Numista: #2835

Value

Exchange value: ½ USD = $0.50

Bullion value: $27.38

Inflation-adjusted value: 7.19 USD

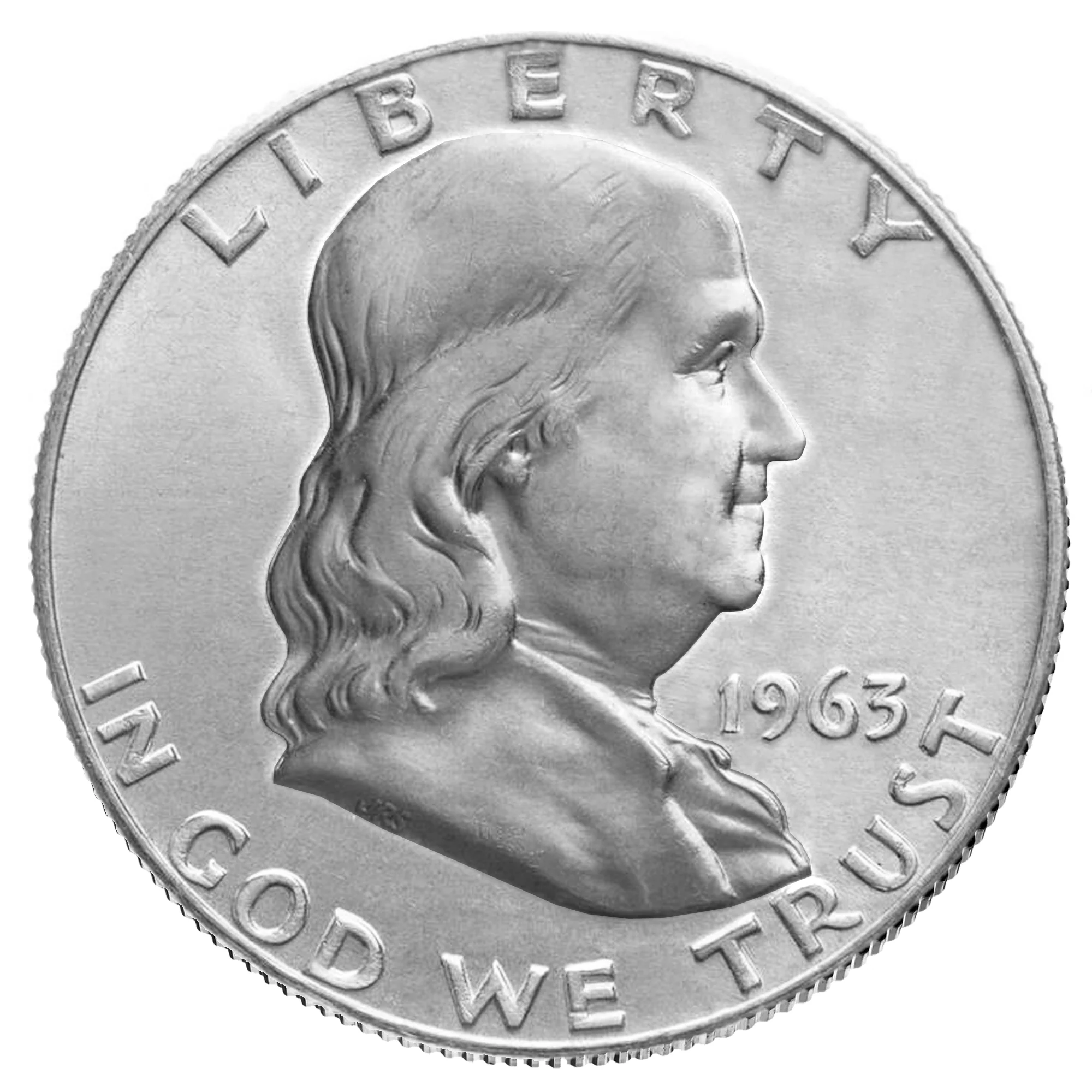

Obverse

Description:

Benjamin Franklin, right profile.

Inscription:

LIBERTY

1953

JRS

IN GOD WE TRUST

1953

JRS

IN GOD WE TRUST

Script: Latin

Engraver: John R. Sinnock

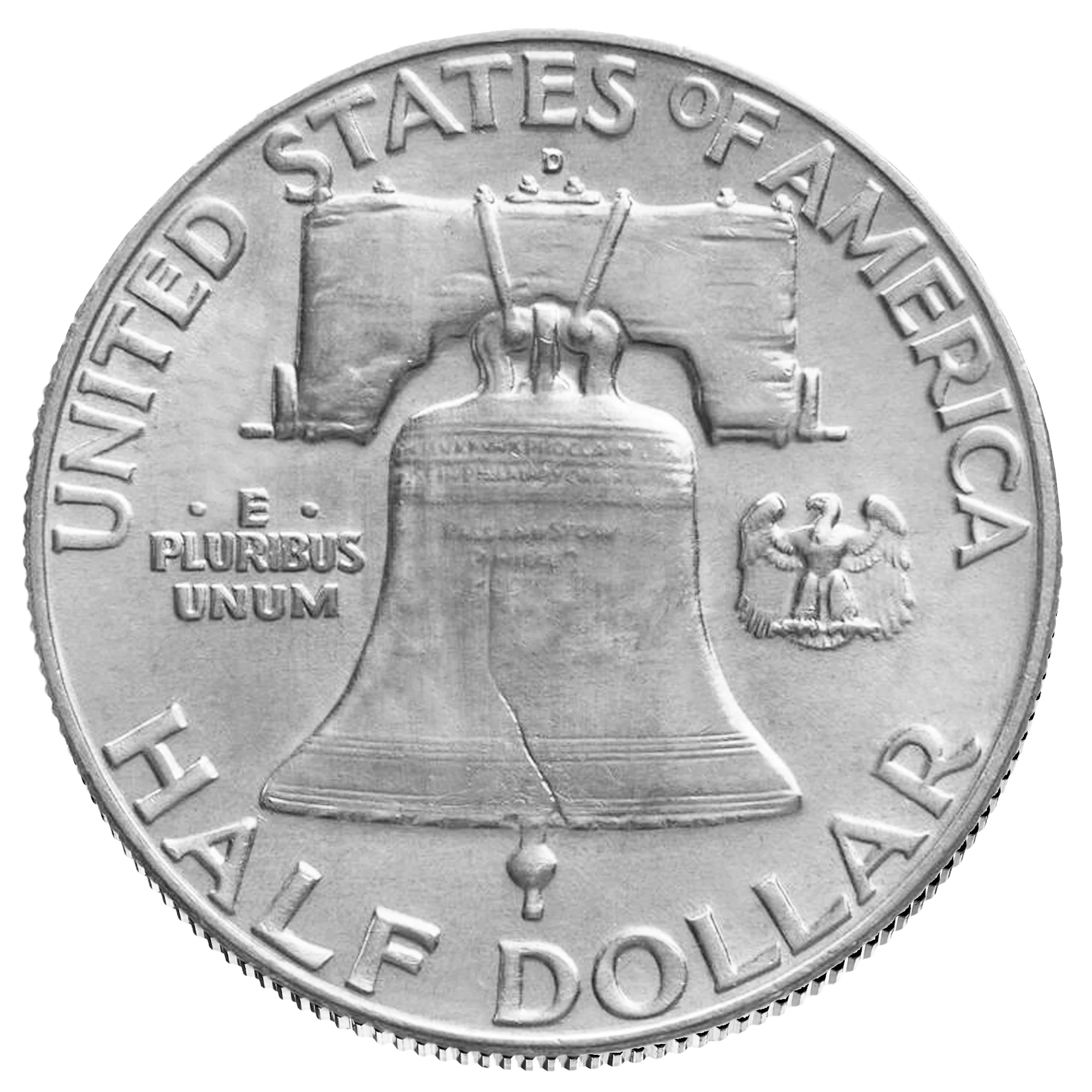

Reverse

Description:

Liberty Bell with eagle above denomination.

Inscription:

UNITED STATES oF AMERICA

·E·

PLURIBUS

UNUM

HALF DOLLAR

·E·

PLURIBUS

UNUM

HALF DOLLAR

Translation:

Out of Many

One

Half Dollar

One

Half Dollar

Script: Latin

Engravers: John R. Sinnock, Gilroy Roberts

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| United States Mint of Philadelphia | — |

| United States Mint of Denver | D |

| United States Mint of San Francisco | S |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1948 | — | 3,006,814 | ||

| 1948 | D | 4,028,600 | ||

| 1949 | — | 5,614,000 | ||

| 1949 | D | 4,120,600 | ||

| 1949 | S | 3,744,000 | ||

| 1950 | — | 7,742,123 | ||

| 1950 | D | 8,031,600 | ||

| 1950 | — | 51,386 | Proof | |

| 1951 | — | 16,802,102 | ||

| 1951 | — | 57,500 | Proof | |

| 1951 | D | 9,475,200 | ||

| 1951 | S | 13,696,000 | ||

| 1952 | — | 21,192,093 | ||

| 1952 | — | 81,980 | Proof | |

| 1952 | D | 25,395,600 | ||

| 1952 | S | 5,526,000 | ||

| 1953 | — | 2,668,120 | ||

| 1953 | — | 128,800 | Proof | |

| 1953 | D | 20,900,400 | ||

| 1953 | S | 4,148,000 | ||

| 1954 | — | 13,188,202 | ||

| 1954 | D | 25,445,580 | ||

| 1954 | — | 233,300 | Proof | |

| 1954 | S | 4,993,400 | ||

| 1955 | — | 2,498,181 | ||

| 1955 | — | 378,200 | Proof | |

| 1955 | — | — | BU | |

| 1956 | — | 4,032,000 | ||

| 1956 | — | 33,469 | Proof | |

| 1957 | — | 5,114,000 | ||

| 1957 | — | 1,247,952 | Proof | |

| 1957 | D | 19,966,850 | ||

| 1958 | D | 23,962,412 | ||

| 1958 | — | 4,042,000 | ||

| 1958 | — | 875,652 | Proof | |

| 1959 | — | 6,200,000 | ||

| 1959 | — | 1,149,291 | Proof | |

| 1959 | D | 13,053,750 | ||

| 1960 | — | 6,024,000 | ||

| 1960 | — | 1,691,602 | Proof | |

| 1960 | D | 18,215,812 | ||

| 1961 | — | 8,290,000 | ||

| 1961 | — | 3,028,244 | Proof | |

| 1961 | D | 20,276,442 | ||

| 1962 | — | 3,218,019 | Proof | |

| 1962 | D | 35,473,281 | ||

| 1962 | — | 9,714,000 | ||

| 1963 | — | 25,239,645 | ||

| 1963 | — | 3,075,645 | Proof | |

| 1963 | D | 67,069,292 |

Historical background

In 1948, the United States operated under the Bretton Woods monetary system, established in 1944. This system fixed the U.S. dollar to gold at $35 per ounce and tied other major world currencies to the dollar within narrow bands. This made the dollar the world's primary reserve and transaction currency, granting the U.S. immense financial prestige and stability in the immediate post-war period. Domestically, citizens used Federal Reserve Notes, but these were technically redeemable in gold for international settlements, creating a gold-exchange standard that underpinned global trade.

However, this external strength masked significant domestic inflationary pressures. The immediate post-war lifting of price controls, pent-up consumer demand, and shortages of goods created a surge in prices. The inflation rate reached nearly 8% in 1948, causing concern for both households and policymakers. In response, the Federal Reserve and the Truman administration took contractionary measures; the Fed raised reserve requirements for banks, and the government ran a budget surplus to curb the money supply and cool the economy, leading to a mild recession in 1949.

Thus, the currency situation in 1948 was one of paradoxical duality: the U.S. dollar stood as the unchallenged pillar of the global financial order, providing stability for worldwide recovery, while domestically, the economy grappled with the disruptive aftershocks of war. This period highlighted the growing tension between America's international monetary obligations and its domestic economic priorities—a tension that would eventually lead to the collapse of the Bretton Woods system decades later.

However, this external strength masked significant domestic inflationary pressures. The immediate post-war lifting of price controls, pent-up consumer demand, and shortages of goods created a surge in prices. The inflation rate reached nearly 8% in 1948, causing concern for both households and policymakers. In response, the Federal Reserve and the Truman administration took contractionary measures; the Fed raised reserve requirements for banks, and the government ran a budget surplus to curb the money supply and cool the economy, leading to a mild recession in 1949.

Thus, the currency situation in 1948 was one of paradoxical duality: the U.S. dollar stood as the unchallenged pillar of the global financial order, providing stability for worldwide recovery, while domestically, the economy grappled with the disruptive aftershocks of war. This period highlighted the growing tension between America's international monetary obligations and its domestic economic priorities—a tension that would eventually lead to the collapse of the Bretton Woods system decades later.

🌱 Very Common