100 Francs – Cameroon

Cameroon

Context

Material

References

KM: #Click to copy to clipboard15

Numista: #2801

Value

Exchange value: 100 FCFA

Obverse

Description:

Three giant elands facing left.

Inscription:

REPUBLIQUE FEDERALE DU CAMEROUN

G.B.L.BAZOR

CR

G.B.L.BAZOR

CR

Translation:

FEDERAL REPUBLIC OF CAMEROUN

G.B.L.BAZOR

CR

G.B.L.BAZOR

CR

Script: Latin

Language: French

Engraver: Lucien Georges Bazor

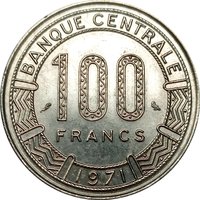

Reverse

Description:

Circle denomination.

Inscription:

BANQUE CENTRALE

100

FRANCS

1971

100

FRANCS

1971

Translation:

Central Bank

100

Francs

1971

100

Francs

1971

Script: Latin

Language: French

Engraver: Lucien Georges Bazor

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Monnaie de Paris | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1971 | — | 9,000,000 | ||

| 1972 | — | 3,000,000 |

Historical background

In 1971, Cameroon’s currency situation was defined by its membership in the Franc Zone and the use of the CFA franc, a colonial-era currency pegged to the French franc. This arrangement, managed by the Central Bank of Equatorial African States (BCEAO), provided monetary stability and guaranteed convertibility through the French Treasury. For the young republic, which had adopted a federal system in 1961 and was moving toward a unitary state in 1972, this meant low inflation and reduced exchange rate risk, which was seen as beneficial for planning and attracting foreign investment, particularly in its growing cocoa, coffee, and oil sectors.

However, this stability came with significant trade-offs. The fixed peg required Cameroon to hold a substantial portion of its foreign reserves in France, limiting its independent monetary policy. The country could not devalue its currency to boost export competitiveness, a tool often used by developing nations. Furthermore, the system was criticized for structurally favoring imports from France and the Franc Zone, potentially hindering the development of local industry and diversification. Economically, the early 1970s were a period of growth for Cameroon, but the currency regime meant its monetary sovereignty was largely delegated to a supranational institution backed by France.

Thus, the background of 1971 is one of a managed currency within a post-colonial framework. The CFA franc provided a predictable financial environment during a critical decade of nation-building and economic expansion under President Ahmadou Ahidjo. Yet, it also embedded Cameroon in a system of external dependency, sparking debates about economic sovereignty that would persist for decades. The situation was largely static that year, but it set the foundational monetary context for the country's ensuing oil boom and the challenges that would follow.

However, this stability came with significant trade-offs. The fixed peg required Cameroon to hold a substantial portion of its foreign reserves in France, limiting its independent monetary policy. The country could not devalue its currency to boost export competitiveness, a tool often used by developing nations. Furthermore, the system was criticized for structurally favoring imports from France and the Franc Zone, potentially hindering the development of local industry and diversification. Economically, the early 1970s were a period of growth for Cameroon, but the currency regime meant its monetary sovereignty was largely delegated to a supranational institution backed by France.

Thus, the background of 1971 is one of a managed currency within a post-colonial framework. The CFA franc provided a predictable financial environment during a critical decade of nation-building and economic expansion under President Ahmadou Ahidjo. Yet, it also embedded Cameroon in a system of external dependency, sparking debates about economic sovereignty that would persist for decades. The situation was largely static that year, but it set the foundational monetary context for the country's ensuing oil boom and the challenges that would follow.

🌱 Very Common