2 paisas – Bombay Presidency

Add to wishlist

India

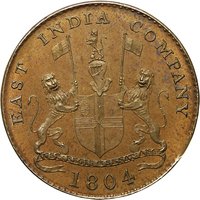

Obverse

Description:

East India Company coat of arms, encircled by "EAST INDIA COMPANY" and "Auspicio Regis Et Senatus Anglia" on a ribbon, with date below, within a raised toothed rim.

Inscription:

EAST INDIA COMPANY

AUSPICIO REGIS & SENATUS ANGLIAE

1804

AUSPICIO REGIS & SENATUS ANGLIAE

1804

Translation:

Under the Auspices of the King and Senate of England

Script: Latin

Language: Latin

Reverse

Description:

Balanced scales within a toothed rim, Persian legend with date AH 1219 below.

Inscription:

عدل

١٢١٩

١٢١٩

Translation:

Justice

1219

1219

Script: Persian (nastaliq)

Language: Arabic

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Soho Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1804 | — | — |

Historical background

In 1804, the Bombay Presidency was grappling with a severe and complex currency crisis, a direct consequence of the East India Company's expanding territorial control and its struggle to impose a unified monetary system. The region was a mosaic of circulating currencies, including Mughal silver rupees (like the Surat rupee), gold pagodas from the south, and various local and foreign coins. This proliferation led to chaotic exchange rates, widespread forgery, and significant transactional inefficiency, hampering both commerce and the Company's own revenue collection. The problem was exacerbated by a global shortage of silver following the Napoleonic Wars, which drove up the value of silver rupees and caused economic dislocation.

The Company's response, initiated under Governor Jonathan Duncan, was the ambitious "Bombay Gold Standard" experiment of 1800-1801. This policy aimed to replace silver with a gold standard, fixing the value of the gold mohur. However, by 1804, this experiment had catastrophically failed. The fixed rate overvalued gold against the market and against the silver-based currencies of Bengal and Madras, leading to arbitrage, the flight of silver from the presidency, and severe economic hardship. Merchants and the public lost confidence, and the system proved unworkable.

Therefore, in 1804, the Presidency was in a state of monetary limbo and distress. The gold standard was discredited but not yet fully abandoned, while the underlying scarcity of specie and the jungle of old currencies persisted. This crisis set the stage for a decisive shift back to a silver standard, which would culminate in the major recoinage of 1806-07 that finally established the Bombay rupee as a stable, unified currency, aligning the presidency with the monetary systems of Bengal and Madras.

The Company's response, initiated under Governor Jonathan Duncan, was the ambitious "Bombay Gold Standard" experiment of 1800-1801. This policy aimed to replace silver with a gold standard, fixing the value of the gold mohur. However, by 1804, this experiment had catastrophically failed. The fixed rate overvalued gold against the market and against the silver-based currencies of Bengal and Madras, leading to arbitrage, the flight of silver from the presidency, and severe economic hardship. Merchants and the public lost confidence, and the system proved unworkable.

Therefore, in 1804, the Presidency was in a state of monetary limbo and distress. The gold standard was discredited but not yet fully abandoned, while the underlying scarcity of specie and the jungle of old currencies persisted. This crisis set the stage for a decisive shift back to a silver standard, which would culminate in the major recoinage of 1806-07 that finally established the Bombay rupee as a stable, unified currency, aligning the presidency with the monetary systems of Bengal and Madras.

💎 Extremely Rare