Obverse

Description:

Inscription surrounds the royal monogram. Date beneath.

Inscription:

LEOPOLD PREMIER ROI DES BELGES

1845

1845

Translation:

Leopold the First King of the Belgians

1845

1845

Script: Latin

Language: French

Engraver: Joseph-Pierre Braemt

Reverse

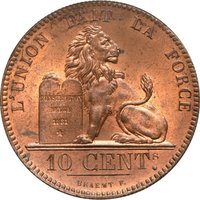

Description:

Belgian lion with paw on 1831 Constitution, surrounded by French motto. Value and designer below.

Inscription:

L'UNION FAIT LA FORCE

CONSTITUTION BELGE 1831 ⋆

1 CENT.

BRAEMT F.

CONSTITUTION BELGE 1831 ⋆

1 CENT.

BRAEMT F.

Translation:

Union makes strength

Belgian Constitution 1831 ⋆

1 Cent.

Braemt F.

Belgian Constitution 1831 ⋆

1 Cent.

Braemt F.

Script: Latin

Language: French

Engraver: Joseph-Pierre Braemt

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Royal Mint of Belgium | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1832 | — | — | ||

| 1833 | — | — | ||

| 1835 | — | 4,367,249 | ||

| 1836 | — | 4,255,720 | ||

| 1837 | — | — | ||

| 1838 | — | — | ||

| 1841 | — | — | ||

| 1844 | — | 1,821,947 | ||

| 1845 | — | 8,324,286 | ||

| 1846 | — | 8,240,951 | ||

| 1847 | — | 5,138,259 | ||

| 1848 | — | 383,031 | ||

| 1849 | — | 1,218,482 | ||

| 1850 | — | 2,308,509 | ||

| 1855 | — | — | ||

| 1856 | — | 2,428,036 | ||

| 1857 | — | 948,175 | ||

| 1858 | — | 916,441 | ||

| 1859 | — | 982,251 | ||

| 1860 | — | 1,580,603 | ||

| 1861 | — | 1,696,346 | ||

| 1862 | — | 11,906,967 | ||

| 1863 | — | — |

Historical background

In 1832, Belgium was navigating the complex monetary aftermath of its recent independence. The new nation, formally recognized just a year prior, inherited a chaotic currency landscape from the period of Dutch rule (1815-1830) and the subsequent revolution. Multiple coinage systems circulated simultaneously, including Dutch guilders, French francs, and older Austrian and regional issues, leading to confusion in commerce and hindering economic stability. The provisional government had taken initial steps by decreeing the French franc as the official monetary unit, but establishing a unified, sovereign currency system was a critical task for the fledgling state.

The situation was formally addressed with the Monetary Law of June 5, 1832, which established the Belgian franc. It was deliberately defined as equal to the French franc, facilitating trade with a powerful neighbor and reflecting the political and economic alignment of the new Belgian state with France rather than the Netherlands. The law aimed to simplify and standardize the monetary chaos by introducing a decimal system (1 franc = 100 centimes) and planning for the minting of new national coinage. However, the law also demonstrated pragmatism by allowing for a transition period where certain foreign coins, particularly French francs, remained legal tender to avoid economic disruption.

Thus, the currency situation in 1832 was one of transition from disorder to order. While the legal framework for a national currency was now in place, the practical reality was a mixed circulation. The success of the reform depended on the gradual production and distribution of new Belgian coins and the eventual withdrawal of foreign specie. This monetary consolidation was a fundamental pillar in building a functional national economy and asserting Belgium's sovereignty in the years following its independence.

The situation was formally addressed with the Monetary Law of June 5, 1832, which established the Belgian franc. It was deliberately defined as equal to the French franc, facilitating trade with a powerful neighbor and reflecting the political and economic alignment of the new Belgian state with France rather than the Netherlands. The law aimed to simplify and standardize the monetary chaos by introducing a decimal system (1 franc = 100 centimes) and planning for the minting of new national coinage. However, the law also demonstrated pragmatism by allowing for a transition period where certain foreign coins, particularly French francs, remained legal tender to avoid economic disruption.

Thus, the currency situation in 1832 was one of transition from disorder to order. While the legal framework for a national currency was now in place, the practical reality was a mixed circulation. The success of the reform depended on the gradual production and distribution of new Belgian coins and the eventual withdrawal of foreign specie. This monetary consolidation was a fundamental pillar in building a functional national economy and asserting Belgium's sovereignty in the years following its independence.

🌱 Common