1 Pound – Egypt

Non-circulating coins

Commemoration: Silver Jubilee of Ain Shams University

Egypt

Context

Year: 1978

Islamic (Hijri) Year: 1398

Issuer: Egypt

Period:

(since 1971)

Currency:

(since 1916)

Total mintage: 50,000

Material

References

KM: #Click to copy to clipboard481

Numista: #26362

Value

Exchange value: 1 EGP

Bullion value: $30.89

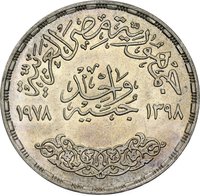

Obverse

Description:

Denominations split dates.

Inscription:

جمهورية مصر العربية

جنيه واحد

١٣٩٨-١٩٧٨

جنيه واحد

١٣٩٨-١٩٧٨

Translation:

Arab Republic of Egypt

One Pound

1398-1978

One Pound

1398-1978

Script: Arabic (naskh)

Language: Arabic

Reverse

Description:

University emblem, name, and anniversary.

Inscription:

العيد الفضي

جامعة عين شمس

۱۹۷۷-١٩٥٢

جامعة عين شمس

۱۹۷۷-١٩٥٢

Translation:

The Silver Jubilee

Ain Shams University

1952-1977

Ain Shams University

1952-1977

Script: Arabic (kufic)

Language: Arabic

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Egyptian Mint Authority | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1978 | — | 50,000 |

Historical background

In 1978, Egypt’s currency situation was defined by a critical transition, caught between the legacy of a state-controlled economy and the pressures of liberalization. Following the 1973 war and the subsequent shift in foreign policy toward the West, President Anwar Sadat’s Infitah (economic opening) policy sought to attract foreign investment and stimulate growth. However, this created a severe duality in the currency system. The official exchange rate was fixed at an overvalued level of approximately E£0.40 to the US dollar, while a rampant black market saw rates soar to nearly E£1.20, reflecting a severe shortage of foreign exchange and a lack of confidence in the Egyptian pound.

This parallel market emerged due to a combination of factors: a chronic trade deficit, heavy reliance on imports (including subsidized food staples), and insufficient earnings from key exports like oil and cotton. Remittances from Egyptians working abroad, which had become a vital source of hard currency, largely bypassed the official banking system, flowing into the black market for a much higher return. The government, burdened by vast subsidies and a bloated public sector, struggled to maintain the artificial official rate, leading to periodic devaluations that failed to close the widening gap with market realities.

Consequently, 1978 represented a year of mounting strain just before a significant policy shift. The currency distortion was a symptom of deeper structural economic problems, discouraging official investment and creating widespread distortions. The unsustainable situation set the stage for the more aggressive reforms and a major devaluation that would follow in the early 1980s, as Egypt moved haltingly toward a more unified and market-driven exchange rate under agreements with the International Monetary Fund.

This parallel market emerged due to a combination of factors: a chronic trade deficit, heavy reliance on imports (including subsidized food staples), and insufficient earnings from key exports like oil and cotton. Remittances from Egyptians working abroad, which had become a vital source of hard currency, largely bypassed the official banking system, flowing into the black market for a much higher return. The government, burdened by vast subsidies and a bloated public sector, struggled to maintain the artificial official rate, leading to periodic devaluations that failed to close the widening gap with market realities.

Consequently, 1978 represented a year of mounting strain just before a significant policy shift. The currency distortion was a symptom of deeper structural economic problems, discouraging official investment and creating widespread distortions. The unsustainable situation set the stage for the more aggressive reforms and a major devaluation that would follow in the early 1980s, as Egypt moved haltingly toward a more unified and market-driven exchange rate under agreements with the International Monetary Fund.

⭐ Somewhat Rare