1 Shilling – Kenya

Kenya

Context

Material

Diameter: 27.8 mm

Weight: 7.9 g

Thickness: 1.65 mm

Shape: Round

Composition: Copper-nickel

Standard: Silver quarter ounce

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #Click to copy to clipboard20

Numista: #2634

Value

Exchange value: 1 KES

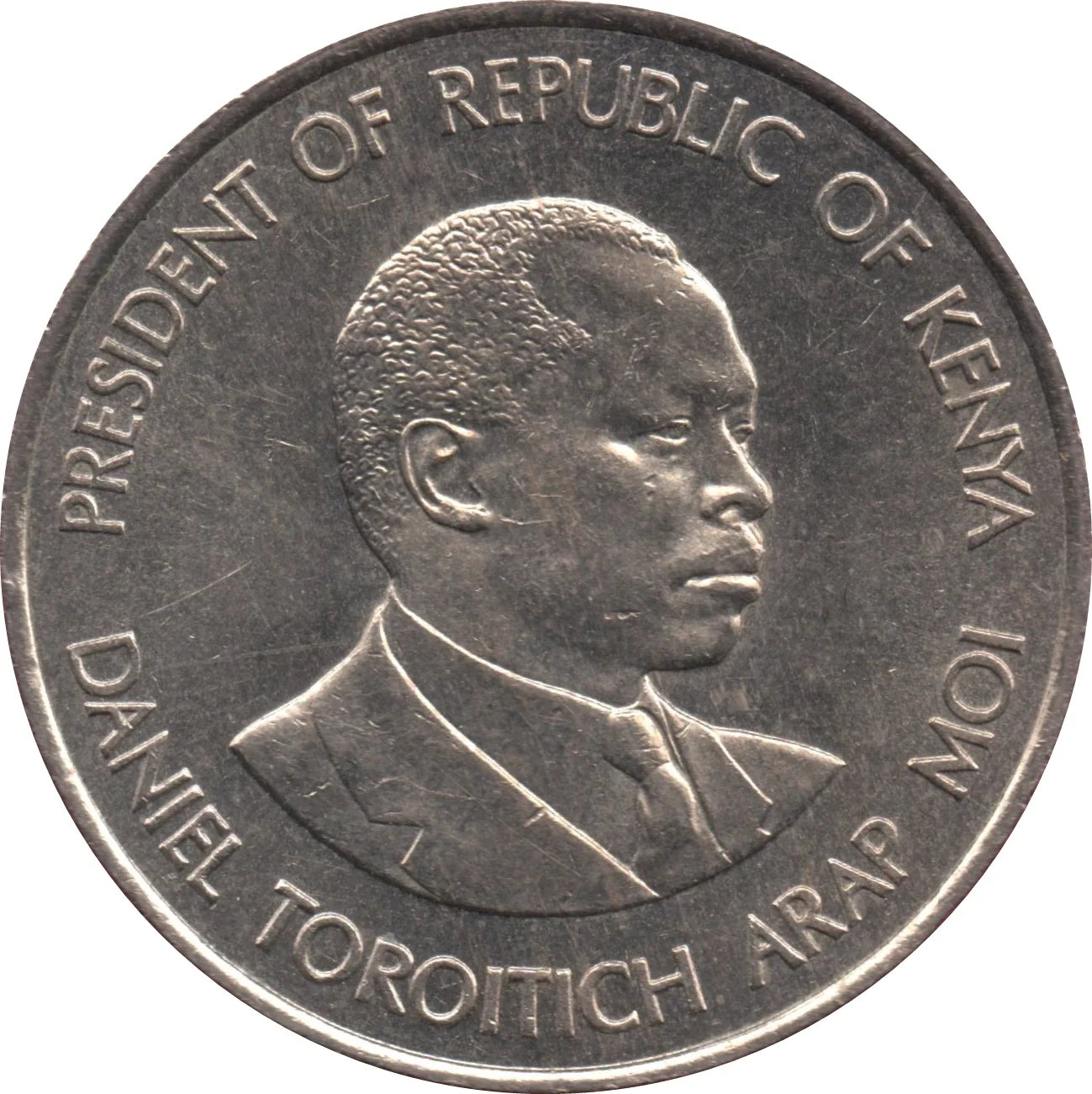

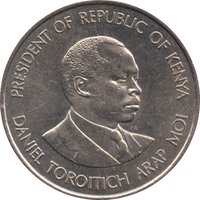

Obverse

Reverse

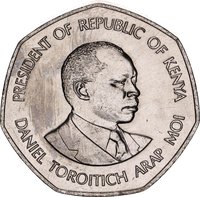

Description:

Bust of Daniel Arap Moi facing right.

Inscription:

PRESIDENT OF REPUBLIC OF KENYA

DANIEL TOROITICH ARAP MOI

DANIEL TOROITICH ARAP MOI

Script: Latin

Edge

Reeded

Categories

| Symbols> Coat of Arms |

| Person> Politician |

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1978 | — | — | Proof | |

| 1980 | — | — | ||

| 1981 | — | — | Proof | |

| 1989 | — | — |

Historical background

In 1978, Kenya's currency situation was characterized by relative stability under the managed framework of the Bretton Woods system, though it existed in the shadow of significant regional change. The Kenyan Shilling (KES), pegged to the U.S. Dollar through a fixed exchange rate, was considered a strong and stable currency within East Africa. This stability was underpinned by a period of consistent economic growth, a robust agricultural export sector (notably coffee and tea), and conservative fiscal management. The Central Bank of Kenya maintained strict control over foreign exchange, and the shilling's credibility was a point of national pride, contrasting with the economic turmoil experienced by some neighboring countries.

However, this apparent stability faced mounting pressures. The year was marked by the death of President Jomo Kenyatta in August and the succession of Daniel arap Moi, introducing political uncertainty. Economically, the first shocks of the late 1970s oil crises were being felt, widening the current account deficit and putting downward pressure on foreign reserves. Furthermore, the collapse of the East African Community in 1977 had severed the currency union with Tanzania and Uganda, making the Kenyan Shilling a distinctly national currency for the first time in over a decade. This necessitated a complex restructuring of regional trade and payments systems.

Consequently, while the shilling's formal peg held in 1978, the groundwork for future devaluation was being laid. The fixed exchange rate, combined with rising import costs and inflationary pressures, began to overvalue the currency, hurting export competitiveness. The government and central bank were thus navigating a delicate transition, committed to stability but increasingly aware that the existing monetary policy would become difficult to sustain. The challenges of 1978 set the stage for the difficult economic adjustments and the eventual shift to a crawling peg and later a floating exchange rate regime in the 1980s.

However, this apparent stability faced mounting pressures. The year was marked by the death of President Jomo Kenyatta in August and the succession of Daniel arap Moi, introducing political uncertainty. Economically, the first shocks of the late 1970s oil crises were being felt, widening the current account deficit and putting downward pressure on foreign reserves. Furthermore, the collapse of the East African Community in 1977 had severed the currency union with Tanzania and Uganda, making the Kenyan Shilling a distinctly national currency for the first time in over a decade. This necessitated a complex restructuring of regional trade and payments systems.

Consequently, while the shilling's formal peg held in 1978, the groundwork for future devaluation was being laid. The fixed exchange rate, combined with rising import costs and inflationary pressures, began to overvalue the currency, hurting export competitiveness. The government and central bank were thus navigating a delicate transition, committed to stability but increasingly aware that the existing monetary policy would become difficult to sustain. The challenges of 1978 set the stage for the difficult economic adjustments and the eventual shift to a crawling peg and later a floating exchange rate regime in the 1980s.

Series: 1978 Kenya circulation coins

🌱 Very Common