Obverse

Inscription:

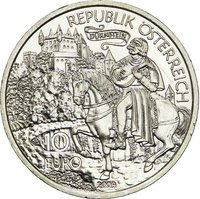

STIFT

KLOSTER-

NEUBURG

10 EURO

REPUBLIK ÖSTERREICH

2008

KLOSTER-

NEUBURG

10 EURO

REPUBLIK ÖSTERREICH

2008

Translation:

Abbey

Monastery-

Neuburg

10 Euro

Republic of Austria

2008

Monastery-

Neuburg

10 Euro

Republic of Austria

2008

Script: Latin

Language: German

Engraver: Thomas Pesendorfer

Reverse

Engraver: Thomas Pesendorfer

Edge

Plain

Categories

| Building> Religious building |

Mints

| Name | Mark |

|---|---|

| Münze Österreich | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2008 | — | 130,000 | ||

| 2008 | — | 60,000 | Proof | |

| 2008 | — | 40,000 | BU |

Historical background

In 2008, Austria was a member of the European Union and a full participant in the Eurozone, having adopted the euro as its official currency in 1999 (for accounting purposes) and introducing euro banknotes and coins in 2002. Consequently, the country did not have an independent national currency policy; its monetary policy was set by the European Central Bank (ECB) in Frankfurt. This meant that Austria's primary economic tools during the unfolding global financial crisis were fiscal policy and the management of its banking sector, rather than direct control over interest rates or currency valuation.

The currency situation was nonetheless critical, as the stability of the euro itself became a central concern. Austria's financial system was particularly exposed to the emerging markets of Central and Eastern Europe, as its banks (like Erste Group and Raiffeisen Bank International) had aggressively expanded there. As the crisis intensified in late 2008, fears grew about the solvency of these banks and the potential for massive capital outflows, which put indirect pressure on the euro. Austria's currency situation was thus intrinsically linked to the euro's strength and the perception of risk within the wider European banking system.

Domestically, the fixed exchange rate of the euro provided stability by eliminating currency risk with its main trading partners, but it also removed the option of devaluation to boost competitiveness. The government's focus turned to securing euro-denominated liquidity for its banks and participating in coordinated EU-wide rescue efforts. Ultimately, Austria navigated the 2008 crisis within the framework of the Eurozone, relying on ECB interventions and European solidarity to maintain currency stability, while confronting a severe banking crisis that was largely homegrown in its causes.

The currency situation was nonetheless critical, as the stability of the euro itself became a central concern. Austria's financial system was particularly exposed to the emerging markets of Central and Eastern Europe, as its banks (like Erste Group and Raiffeisen Bank International) had aggressively expanded there. As the crisis intensified in late 2008, fears grew about the solvency of these banks and the potential for massive capital outflows, which put indirect pressure on the euro. Austria's currency situation was thus intrinsically linked to the euro's strength and the perception of risk within the wider European banking system.

Domestically, the fixed exchange rate of the euro provided stability by eliminating currency risk with its main trading partners, but it also removed the option of devaluation to boost competitiveness. The government's focus turned to securing euro-denominated liquidity for its banks and participating in coordinated EU-wide rescue efforts. Ultimately, Austria navigated the 2008 crisis within the framework of the Eurozone, relying on ECB interventions and European solidarity to maintain currency stability, while confronting a severe banking crisis that was largely homegrown in its causes.

Series: Austria and its People

🌟 Limited