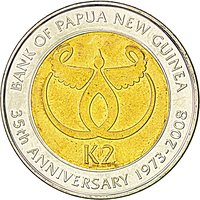

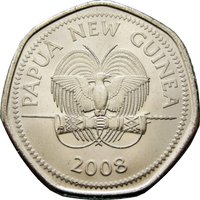

2 kina (Bank of Papua New Guinea) – Papua New Guinea

Add to wishlist

Circulating commemorative coins

Commemoration: 35th Anniversary of the Bank of Papua New Guinea

Papua New Guinea

Obverse

Reverse

Description:

Central logo with commemorative inscription encircling.

Inscription:

BANK OF PAPUA NEW GUINEA

K 2

35th ANNIVERSARY 1973 - 2008

K 2

35th ANNIVERSARY 1973 - 2008

Script: Latin

Edge

Milled

Categories

| Animal> Bird |

| Art> Music |

| Symbols> Coat of Arms |

| Object> Cold weapons |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2008 | — | — |

Historical background

In 2008, Papua New Guinea's currency, the kina (PGK), faced significant pressure, primarily driven by a sharp decline in global commodity prices in the latter half of the year. The economy was highly dependent on mineral and hydrocarbon exports, with high prices earlier in the year contributing to strong foreign exchange inflows and a period of relative stability. However, the onset of the Global Financial Crisis triggered a collapse in prices for key exports like copper, gold, and oil, drastically reducing the nation's export earnings and straining the foreign exchange reserves held by the Bank of Papua New Guinea (BPNG).

This external shock exposed underlying structural weaknesses in the country's foreign exchange market. A persistent imbalance existed, with demand for foreign currency (especially Australian and US dollars) from importers and investors consistently outstripping supply. The central bank managed a de facto peg, intervening to maintain the kina within a band, but this became unsustainable as reserves dwindled. Consequently, a significant backlog of unmet foreign currency orders developed within the commercial banking system, crippling business operations and creating a climate of uncertainty for foreign investment.

The government and central bank faced a difficult policy dilemma. There was strong political and social resistance to a formal devaluation, as it would increase the cost of essential imports and fuel inflation. Instead, BPNG initially focused on administrative measures, including tightening foreign exchange controls and rationing US dollar allocations to prioritize critical imports. These measures, however, were widely seen as inefficient and distortive, merely managing the symptoms rather than addressing the fundamental overvaluation of the kina. The currency pressures of 2008 thus set the stage for ongoing economic challenges and debates about exchange rate policy in the years that followed.

This external shock exposed underlying structural weaknesses in the country's foreign exchange market. A persistent imbalance existed, with demand for foreign currency (especially Australian and US dollars) from importers and investors consistently outstripping supply. The central bank managed a de facto peg, intervening to maintain the kina within a band, but this became unsustainable as reserves dwindled. Consequently, a significant backlog of unmet foreign currency orders developed within the commercial banking system, crippling business operations and creating a climate of uncertainty for foreign investment.

The government and central bank faced a difficult policy dilemma. There was strong political and social resistance to a formal devaluation, as it would increase the cost of essential imports and fuel inflation. Instead, BPNG initially focused on administrative measures, including tightening foreign exchange controls and rationing US dollar allocations to prioritize critical imports. These measures, however, were widely seen as inefficient and distortive, merely managing the symptoms rather than addressing the fundamental overvaluation of the kina. The currency pressures of 2008 thus set the stage for ongoing economic challenges and debates about exchange rate policy in the years that followed.

🌱 Very Common