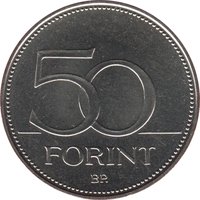

50 forint (Treaty of Rome) – Hungary

Add to wishlist

Circulating commemorative coins

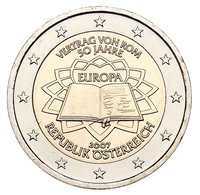

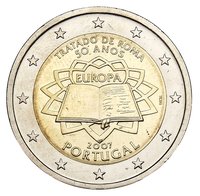

Commemoration: Celebrating 50 Years of the Treaty of Rome

Series: Treaty of Rome

Hungary

Context

Material

Diameter: 27.4 mm

Weight: 7.7 g

Thickness: 1.8 mm

Shape: Round

Standard: Silver quarter ounce

Technique: Milled

Alignment: Medal alignment

flip

References

KM: #

Numista: #2571

Value

Exchange value: 50 HUF

Inflation-adjusted value: 118.39 HUF

Obverse

Description:

Roman motif; Treaty of Rome book with issue date below.

Inscription:

MAGYAR KÖZTÁRSASÁG

"EURÓPA"

50 ÉVES

A RÓMAI SZERZŐDÉS

2007

"EURÓPA"

50 ÉVES

A RÓMAI SZERZŐDÉS

2007

Translation:

HUNGARIAN REPUBLIC

"EUROPA"

50TH ANNIVERSARY

THE TREATY OF ROME

2007

"EUROPA"

50TH ANNIVERSARY

THE TREATY OF ROME

2007

Script: Latin

Language: Hungarian

Designer: István Kósa

Reverse

Description:

Value underlined, mintmark below.

Inscription:

50

FORINT

BP.

FORINT

BP.

Script: Latin

Designer: István Bartos

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Hungarian mint | BP. |

Historical background

In 2007, Hungary's currency situation was characterized by significant volatility and pressure on the Hungarian forint (HUF), stemming from a challenging combination of domestic fiscal imbalances and shifting global risk sentiment. The country was grappling with the aftermath of large fiscal deficits and high public debt, which had prompted the imposition of an unprecedented austerity program in 2006. This "széleskörű kiigazítás" (comprehensive adjustment) aimed to rein in the budget deficit but also slowed economic growth, undermining investor confidence and leading to a "risk premium" on Hungarian assets.

The forint, which traded in a managed float against the euro, was particularly sensitive to shifts in global liquidity and investor appetite for emerging market assets. Throughout the year, the currency experienced sharp fluctuations, often weakening on political uncertainty or broader financial market jitters. The National Bank of Hungary (MNB) faced a difficult policy dilemma: it needed to maintain relatively high interest rates to support the forint and combat stubbornly high inflation, but doing so also risked further dampening domestic economic activity and increasing the debt servicing costs for households with foreign-currency loans.

By the end of 2007, the situation was growing increasingly precarious as the early tremors of the global financial crisis began to emerge. While the forint had not yet entered a full-blown crisis, the underlying vulnerabilities—a large twin deficit, high external debt, and a heavy burden of Swiss franc and euro-denominated loans in the private sector—had created a fragile equilibrium. This set the stage for the severe currency stress that would erupt in 2008 when the global financial crisis fully hit, forcing Hungary to seek a joint rescue package from the IMF, the EU, and the World Bank.

The forint, which traded in a managed float against the euro, was particularly sensitive to shifts in global liquidity and investor appetite for emerging market assets. Throughout the year, the currency experienced sharp fluctuations, often weakening on political uncertainty or broader financial market jitters. The National Bank of Hungary (MNB) faced a difficult policy dilemma: it needed to maintain relatively high interest rates to support the forint and combat stubbornly high inflation, but doing so also risked further dampening domestic economic activity and increasing the debt servicing costs for households with foreign-currency loans.

By the end of 2007, the situation was growing increasingly precarious as the early tremors of the global financial crisis began to emerge. While the forint had not yet entered a full-blown crisis, the underlying vulnerabilities—a large twin deficit, high external debt, and a heavy burden of Swiss franc and euro-denominated loans in the private sector—had created a fragile equilibrium. This set the stage for the severe currency stress that would erupt in 2008 when the global financial crisis fully hit, forcing Hungary to seek a joint rescue package from the IMF, the EU, and the World Bank.

Series: Treaty of Rome

🌱 Common