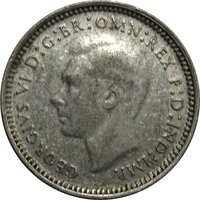

Obverse

Description:

King George VI, left-facing portrait.

Inscription:

GEORGIVS VI D:G:BR OMN:REX F:D:IND:IMP.

Translation:

George VI by the Grace of God King of all the Britains Defender of the Faith Emperor of India.

Script: Latin

Language: Latin

Designer: Thomas Humphrey Paget

Reverse

Description:

Three Wheat Stalks, Ribbon-Tied

Inscription:

AUSTRALIA

19 48

K G

THREE PENCE

19 48

K G

THREE PENCE

Script: Latin

Designer: George Kruger Gray

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1947 | — | 4,176,000 | ||

| 1948 | — | 26,208,000 |

Historical background

In 1947, Australia’s currency situation was fundamentally shaped by its membership in the Sterling Area and the Bretton Woods system of fixed exchange rates. The Australian pound was pegged to the British pound sterling at parity (A£1 = £1 sterling), which itself was fixed to the US dollar at a rate of US$4.03. This arrangement tightly linked Australia’s economy and monetary policy to that of the United Kingdom, ensuring a ready market for primary exports and facilitating capital flows, but also limiting independent monetary control.

The post-World War II period presented significant challenges, including high domestic inflation and a severe shortage of US dollars within the Sterling Area. Australia faced a growing balance of payments crisis, as the demand for imported capital goods for reconstruction and consumer items far exceeded export earnings. In response, the Chifley Labor government maintained and intensified wartime currency controls and import licensing to conserve scarce foreign exchange, particularly US dollars, and to protect sterling reserves. These restrictive measures were deemed necessary to manage the dollar gap and direct resources toward national development.

Furthermore, 1947 was a year of transition and debate regarding the national banking system. The government was actively pursuing the controversial policy of bank nationalisation, which sought to give the Commonwealth Bank full control over monetary policy and credit creation. While this political battle centred on the banking system rather than the exchange rate itself, it underscored the government’s desire for greater economic sovereignty and control over financial flows—a theme directly connected to managing the constrained currency situation of the Sterling Area in a challenging global economic landscape.

The post-World War II period presented significant challenges, including high domestic inflation and a severe shortage of US dollars within the Sterling Area. Australia faced a growing balance of payments crisis, as the demand for imported capital goods for reconstruction and consumer items far exceeded export earnings. In response, the Chifley Labor government maintained and intensified wartime currency controls and import licensing to conserve scarce foreign exchange, particularly US dollars, and to protect sterling reserves. These restrictive measures were deemed necessary to manage the dollar gap and direct resources toward national development.

Furthermore, 1947 was a year of transition and debate regarding the national banking system. The government was actively pursuing the controversial policy of bank nationalisation, which sought to give the Commonwealth Bank full control over monetary policy and credit creation. While this political battle centred on the banking system rather than the exchange rate itself, it underscored the government’s desire for greater economic sovereignty and control over financial flows—a theme directly connected to managing the constrained currency situation of the Sterling Area in a challenging global economic landscape.

🌱 Common