1000 escudos – Portugal

Add to wishlist

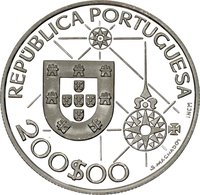

Portugal

Obverse

Description:

Portuguese shield centered, surrounded by Latin American and Spanish state shields along the border.

Inscription:

REPUBLICA PORTUGUESA

· 1000 ESC ·

· 1000 ESC ·

Translation:

PORTUGUESE REPUBLIC

· 1000 ESCUDOS ·

· 1000 ESCUDOS ·

Script: Latin

Language: Portuguese

Engravers: Isabel Carriço, Fernando Branco

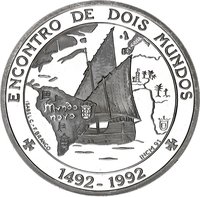

Reverse

Description:

Ship and map symbols in a circle.

Inscription:

ENCONTRO DE DOIS MUNDOS

1492 - 1992

ISABEL C.-F. BRANCO

INCM 91

1492 - 1992

ISABEL C.-F. BRANCO

INCM 91

Script: Latin

Engravers: Isabel Carriço, Fernando Branco

Edge

Reeded

Categories

| Symbols> Coat of Arms |

| Map |

| Transportation> Watercraft |

Mints

| Name | Mark |

|---|---|

| Imprensa Nacional - Casa da Moeda | INCM |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1992 | INCM | 50,000 | Proof |

Historical background

In 1992, Portugal's currency situation was defined by its pivotal and challenging integration into the European Exchange Rate Mechanism (ERM), the system designed to stabilize exchange rates ahead of the planned single currency. The Portuguese escudo had entered the ERM in April 1992, but at a central rate that many analysts considered overvalued, pegged within a narrow ±2.25% band against other European currencies. This entry was a political and economic statement of Portugal's commitment to European integration, following its accession to the European Community in 1986, but it immediately constrained monetary policy and required strict discipline to maintain the peg.

The year unfolded amidst severe turbulence in European currency markets. Speculative attacks, driven by doubts over economic convergence and political commitment to fixed parities, began in earnest in September 1992 with the crisis forcing the British pound and Italian lira out of the ERM. Portugal came under intense pressure as investors questioned the sustainability of the escudo's peg, particularly given the country's higher inflation and interest rates compared to its core European partners, especially Germany. The Banco de Portugal was forced to intervene heavily, spending billions in foreign reserves and raising short-term interest rates to extraordinary levels—at one point to over 100%—to defend the currency and maintain its ERM membership.

Ultimately, Portugal succeeded in staying within the ERM, but at a significant cost. In November 1992, it was compelled to devalue the escudo by 6%, a move that realigned its central rate to a more sustainable level and eased monetary pressure. This devaluation, while a tactical retreat, preserved Portugal's path toward Economic and Monetary Union (EMU). The 1992 crisis underscored the difficulties of convergence for peripheral economies and set the stage for the austerity and further economic reforms that would be necessary for Portugal to eventually adopt the euro in 1999.

The year unfolded amidst severe turbulence in European currency markets. Speculative attacks, driven by doubts over economic convergence and political commitment to fixed parities, began in earnest in September 1992 with the crisis forcing the British pound and Italian lira out of the ERM. Portugal came under intense pressure as investors questioned the sustainability of the escudo's peg, particularly given the country's higher inflation and interest rates compared to its core European partners, especially Germany. The Banco de Portugal was forced to intervene heavily, spending billions in foreign reserves and raising short-term interest rates to extraordinary levels—at one point to over 100%—to defend the currency and maintain its ERM membership.

Ultimately, Portugal succeeded in staying within the ERM, but at a significant cost. In November 1992, it was compelled to devalue the escudo by 6%, a move that realigned its central rate to a more sustainable level and eased monetary pressure. This devaluation, while a tactical retreat, preserved Portugal's path toward Economic and Monetary Union (EMU). The 1992 crisis underscored the difficulties of convergence for peripheral economies and set the stage for the austerity and further economic reforms that would be necessary for Portugal to eventually adopt the euro in 1999.

Series: System 1981-2001

🌟 Limited