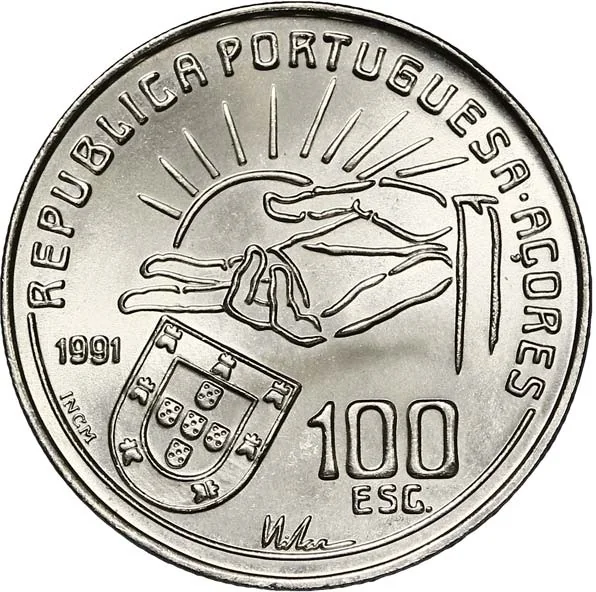

100 Escudos (Antero de Quental) – Portugal

Non-circulating coins

Commemoration: 100th Anniversary - Death of Poet Antero de Quental

Portugal

Obverse

Inscription:

REPUBLICA PORTUGUESA·AÇORES

1991

INCM

100 ESC.

1991

INCM

100 ESC.

Translation:

PORTUGUESE REPUBLIC·AZORES

1991

INCM

100 ESC.

1991

INCM

100 ESC.

Script: Latin

Language: Portuguese

Reverse

Description:

Poet's portrait, dates, and legend.

Inscription:

ANTERO DE QUENTAL

1842/1891

1842/1891

Script: Latin

Edge

Reeded

Categories

| Symbols> Coat of Arms |

| Art> Literature |

| Event> Death anniversary |

Mints

| Name | Mark |

|---|---|

| Imprensa Nacional - Casa da Moeda | INCM |

Historical background

In 1991, Portugal's currency situation was defined by its pivotal role within the European Monetary System (EMS) and its strategic path toward European Economic and Monetary Union (EMU). The Portuguese escudo (PTE) was a member of the EMS Exchange Rate Mechanism (ERM), which required maintaining its value within a narrow band of fluctuation against other member currencies, most importantly the Deutsche Mark. This commitment served as a crucial anchor for monetary policy, imposing discipline to control inflation and stabilize the economy after the turbulent years following the 1974 revolution. The Banco de Portugal managed the escudo within this framework, prioritizing exchange rate stability as a cornerstone for economic integration with its European partners.

The domestic economic context was one of convergence, but with significant challenges. Portugal had joined the European Community in 1986, triggering a period of rapid modernization and growth fueled by structural funds and foreign investment. However, inflation, though falling, remained persistently higher than the European average, and public finances were under strain. Maintaining the ERM parity sometimes required high interest rates and intervention in currency markets to defend the escudo, creating a tension between supporting domestic growth and fulfilling the stringent convergence criteria outlined in the Maastricht Treaty, which was signed that very year.

Thus, 1991 was a year of determined transition, where the escudo's management was explicitly in service of a larger political and economic goal: full participation in a single European currency. The currency situation was not an end in itself but a disciplined mechanism to align Portugal's economy with the core of Europe. Every policy decision regarding the escudo was evaluated through the lens of meeting the Maastricht criteria on inflation, interest rates, budget deficits, and debt, setting the stage for the escudo's eventual—and successful—replacement by the euro in 1999.

The domestic economic context was one of convergence, but with significant challenges. Portugal had joined the European Community in 1986, triggering a period of rapid modernization and growth fueled by structural funds and foreign investment. However, inflation, though falling, remained persistently higher than the European average, and public finances were under strain. Maintaining the ERM parity sometimes required high interest rates and intervention in currency markets to defend the escudo, creating a tension between supporting domestic growth and fulfilling the stringent convergence criteria outlined in the Maastricht Treaty, which was signed that very year.

Thus, 1991 was a year of determined transition, where the escudo's management was explicitly in service of a larger political and economic goal: full participation in a single European currency. The currency situation was not an end in itself but a disciplined mechanism to align Portugal's economy with the core of Europe. Every policy decision regarding the escudo was evaluated through the lens of meeting the Maastricht criteria on inflation, interest rates, budget deficits, and debt, setting the stage for the escudo's eventual—and successful—replacement by the euro in 1999.

⭐ Somewhat Rare