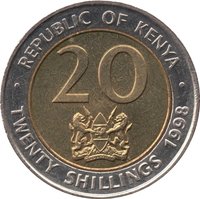

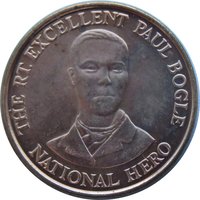

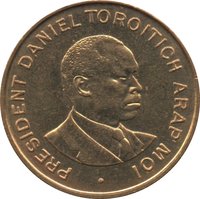

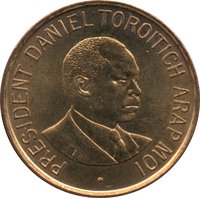

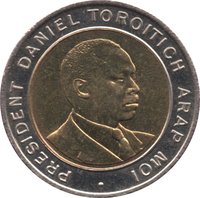

20 shillings – Kenya

Add to wishlist

Kenya

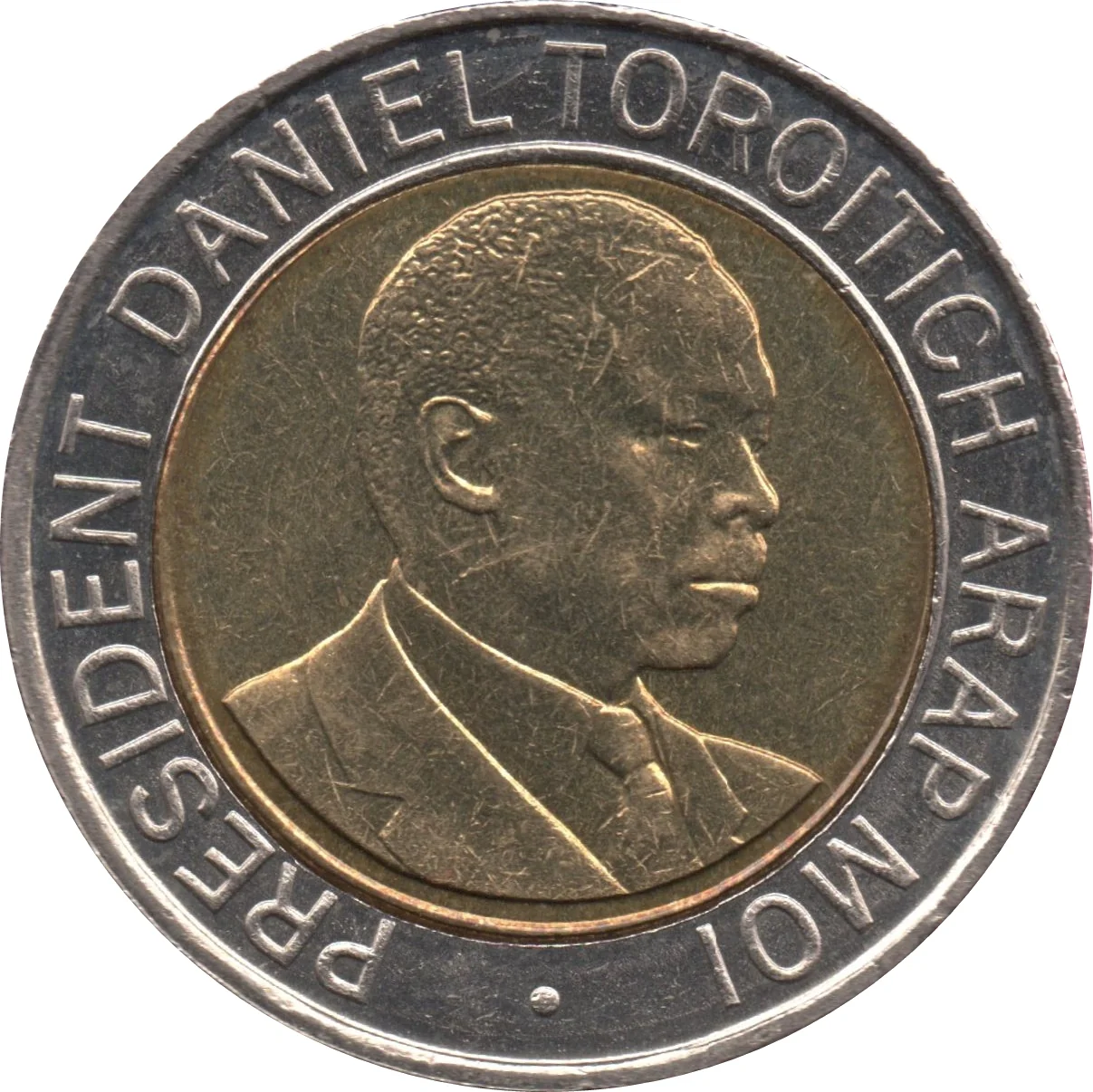

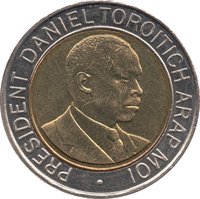

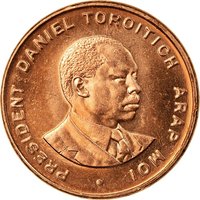

Obverse

Reverse

Description:

Bust of Daniel Arap Moi facing right.

Inscription:

PRESIDENT DANIEL TOROITICH ARAP MOI ·

Script: Latin

Edge

Segmented reeding

Categories

| Person> Politician |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1998 | — | — |

Historical background

In 1998, Kenya's currency situation was characterized by a managed float of the Kenyan Shilling (KES) under significant pressure, following a period of economic liberalization. The Central Bank of Kenya (CBK) had shifted from a fixed exchange rate regime in the early 1990s, but continued to intervene heavily to control volatility. This period was marked by a gradual but persistent depreciation of the shilling, driven by a combination of structural economic weaknesses, including a widening trade deficit, declining agricultural exports (notably coffee), and low foreign exchange reserves. The CBK's tight monetary policy aimed to curb inflation and support the currency, but high-interest rates also constrained economic growth.

The year was particularly challenging due to both domestic and external shocks. Domestically, political uncertainty surrounding the 1997 general elections and subsequent governance concerns undermined investor confidence, leading to capital flight. Externally, the devastating El Niño rains in late 1997 and early 1998 damaged infrastructure and key agricultural sectors, straining the economy further. Most significantly, the August 1998 US embassy bombings in Nairobi had an immediate and severe impact, crippling the vital tourism industry—a major source of foreign exchange—and further eroding international confidence in the country's stability.

Consequently, the shilling faced sustained downward pressure against major currencies like the US dollar throughout the year. The CBK's interventions to defend the shilling depleted its limited foreign reserves, creating a cycle that was difficult to break. This environment of depreciation, coupled with high inflation (which averaged 6.7% for the year), increased the cost of imports and servicing foreign debt, placing a heavy burden on businesses and consumers. The currency dynamics of 1998 thus reflected a struggling economy in transition, grappling with the demands of a liberalized market amidst severe internal and external crises.

The year was particularly challenging due to both domestic and external shocks. Domestically, political uncertainty surrounding the 1997 general elections and subsequent governance concerns undermined investor confidence, leading to capital flight. Externally, the devastating El Niño rains in late 1997 and early 1998 damaged infrastructure and key agricultural sectors, straining the economy further. Most significantly, the August 1998 US embassy bombings in Nairobi had an immediate and severe impact, crippling the vital tourism industry—a major source of foreign exchange—and further eroding international confidence in the country's stability.

Consequently, the shilling faced sustained downward pressure against major currencies like the US dollar throughout the year. The CBK's interventions to defend the shilling depleted its limited foreign reserves, creating a cycle that was difficult to break. This environment of depreciation, coupled with high inflation (which averaged 6.7% for the year), increased the cost of imports and servicing foreign debt, placing a heavy burden on businesses and consumers. The currency dynamics of 1998 thus reflected a struggling economy in transition, grappling with the demands of a liberalized market amidst severe internal and external crises.

Series: 1995 series

🌱 Very Common