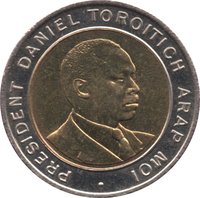

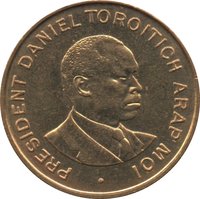

5 Shillings – Kenya

Kenya

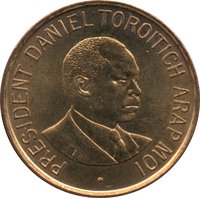

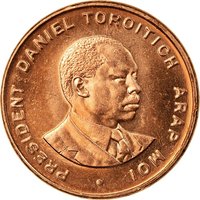

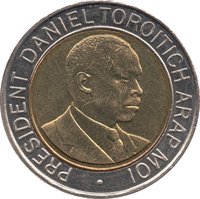

Obverse

Reverse

Description:

Bust of Daniel Arap Moi facing right.

Inscription:

PRESIDENT DANIEL TOROITICH ARAP MOI ·

Script: Latin

Edge

Reeded

Categories

| Person> Politician |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1995 | — | — | ||

| 1997 | — | — |

Historical background

In 1995, Kenya's currency situation was characterized by a managed float of the Kenyan shilling (KES) under significant pressure. Following the liberalization of the foreign exchange market in 1993, which abolished official fixed rates in favor of a market-driven interbank system, the shilling experienced a sharp and continuous depreciation. This was driven by classic macroeconomic imbalances: high inflation (averaging 28.8% in 1994 and 1.7% per month in early 1995), a substantial and growing current account deficit, and low foreign exchange reserves. The Central Bank of Kenya (CBK) intervened sporadically to smooth volatility, but lacked the reserves to defend a specific rate, leading to a steady decline in the shilling's value against major currencies.

The underlying economic context was one of structural adjustment programs prescribed by the International Monetary Fund (IMF) and World Bank, which emphasized liberalization but coincided with a period of political instability and governance challenges. While the float aimed to correct overvaluation and attract capital, it also contributed to a cost-of-living crisis. The depreciation made imports, particularly essential goods like petroleum and machinery, more expensive, fueling inflationary pressures in a vicious cycle. This eroded purchasing power and placed a heavy burden on the populace, with economic growth remaining sluggish.

Consequently, 1995 was a year of difficult adjustment. The government faced the dual challenge of stabilizing the currency and taming inflation while under international pressure to maintain reform momentum. Policy measures were often inconsistent, oscillating between monetary tightening and fiscal slippage. The currency volatility also created uncertainty for businesses and investors, hindering long-term planning. Thus, the shilling's trajectory in 1995 was less a isolated monetary event and more a reflection of the broader economic and governance struggles facing the nation during that era.

The underlying economic context was one of structural adjustment programs prescribed by the International Monetary Fund (IMF) and World Bank, which emphasized liberalization but coincided with a period of political instability and governance challenges. While the float aimed to correct overvaluation and attract capital, it also contributed to a cost-of-living crisis. The depreciation made imports, particularly essential goods like petroleum and machinery, more expensive, fueling inflationary pressures in a vicious cycle. This eroded purchasing power and placed a heavy burden on the populace, with economic growth remaining sluggish.

Consequently, 1995 was a year of difficult adjustment. The government faced the dual challenge of stabilizing the currency and taming inflation while under international pressure to maintain reform momentum. Policy measures were often inconsistent, oscillating between monetary tightening and fiscal slippage. The currency volatility also created uncertainty for businesses and investors, hindering long-term planning. Thus, the shilling's trajectory in 1995 was less a isolated monetary event and more a reflection of the broader economic and governance struggles facing the nation during that era.

Series: 1995 series

🌱 Very Common