100 Francs – France

France

Context

Years: 1982–2001

Issuer: France

Period:

(since 1958)

Currency:

(1960—2001)

Demonetization: 17 February 2002

Total mintage: 11,918,768

Material

References

KM: #Click to copy to clipboard951.1

Numista: #11

Value

Exchange value: 100 FRF

Bullion value: $37.83

Inflation-adjusted value: 296.26 FRF

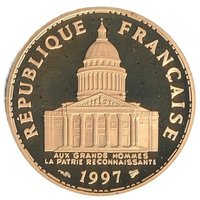

Obverse

Description:

The Panthéon in Paris bears the inscription "AUX GRANDS HOMMES LA PATRIE RECONNAISSANTE" and is encircled by "REPUBLIQUE FRANÇAISE."

Inscription:

RÉPUBLIQUE FRANÇAISE

AUX GRANDS HOMMES

LA PATRIE RECONNAISSANTE

1983

AUX GRANDS HOMMES

LA PATRIE RECONNAISSANTE

1983

Translation:

TO GREAT MEN

THE GRATEFUL HOMELAND

1983

THE GRATEFUL HOMELAND

1983

Script: Latin

Language: French

Engravers: Jean-Claude Dieudonné, Atelier de Gravure (A.G.M.M.)

Reverse

Description:

A large tree bearing the face value and a French hexagon, encircled by the motto "LIBERTE • EGALITE • FRATERNITE".

Inscription:

LIBERTÉ · ÉGALITÉ · FRATERNITÉ

100 F

100 F

Translation:

LIBERTY · EQUALITY · FRATERNITY

100 FRANCS

100 FRANCS

Script: Latin

Language: French

Engravers: Daniel Gédalge, Atelier de Gravure (A.G.M.M.)

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Monnaie de Paris | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1982 | — | — | ||

| 1983 | — | 5,000,961 | ||

| 1984 | — | 5,000,647 | ||

| 1985 | — | 999,711 | ||

| 1986 | — | 501,411 | BU | |

| 1987 | — | 92,967 | BU | |

| 1988 | — | 95,576 | BU | |

| 1989 | — | 96,449 | BU | |

| 1990 | — | 15,011 | ||

| 1991 | — | 5,011 | ||

| 1991 | — | 6,232 | Proof | |

| 1992 | — | 4,938 | Proof | |

| 1993 | — | 5,309 | Proof | |

| 1994 | — | 4,566 | Proof | |

| 1995 | — | 4,011 | ||

| 1995 | — | 4,796 | Proof | |

| 1996 | — | 2,013 | ||

| 1996 | — | 5,319 | Proof | |

| 1997 | — | 6,436 | Proof | |

| 1998 | — | 7,404 | Proof | |

| 1999 | — | 10,000 | Proof | |

| 2000 | — | 15,000 | Proof | |

| 2001 | — | 35,000 | Proof |

Historical background

In 1982, France found itself grappling with a severe currency crisis within the broader context of the European Monetary System (EMS). The newly elected Socialist government of President François Mitterrand, which had come to power in 1981, had embarked on an ambitious program of economic reflation—increasing public spending, nationalizing industries, and raising wages and social benefits. This "Keynesianism in one country" approach, however, clashed with the restrictive monetary policies of major trading partners like the United States and West Germany, leading to soaring trade deficits and capital flight as investors lost confidence.

The franc came under intense speculative pressure, forcing three devaluations within the EMS in just over a year: in October 1981, June 1982, and March 1983. Each devaluation was a negotiated realignment meant to restore French competitiveness, but they were politically humiliating and economically painful, failing to resolve the underlying issues. By the 1982 devaluation, the government had already begun a sharp policy pivot known as the "tournant de la rigueur" (turn to austerity), freezing prices and wages and beginning to curb public spending in an attempt to defend the currency and remain within the European exchange rate mechanism.

This currency turmoil of 1982 thus represented a critical juncture. It exposed the impossibility of pursuing a unilateral expansionist policy while tied to a fixed exchange rate system with Germany's dominant, stability-oriented Bundesbank. The crisis set the stage for the decisive choice in March 1983 to fully commit to the EMS and European integration, prioritizing monetary stability and competitiveness over domestic stimulus—a foundational moment that would shape French economic policy for decades and ultimately lead to the euro.

The franc came under intense speculative pressure, forcing three devaluations within the EMS in just over a year: in October 1981, June 1982, and March 1983. Each devaluation was a negotiated realignment meant to restore French competitiveness, but they were politically humiliating and economically painful, failing to resolve the underlying issues. By the 1982 devaluation, the government had already begun a sharp policy pivot known as the "tournant de la rigueur" (turn to austerity), freezing prices and wages and beginning to curb public spending in an attempt to defend the currency and remain within the European exchange rate mechanism.

This currency turmoil of 1982 thus represented a critical juncture. It exposed the impossibility of pursuing a unilateral expansionist policy while tied to a fixed exchange rate system with Germany's dominant, stability-oriented Bundesbank. The crisis set the stage for the decisive choice in March 1983 to fully commit to the EMS and European integration, prioritizing monetary stability and competitiveness over domestic stimulus—a foundational moment that would shape French economic policy for decades and ultimately lead to the euro.

🌱 Very Common