1 Lilangeni – Kingdom of Swaziland

Eswatini

Context

Years: 1995–2009

Country: Eswatini

Issuer: Kingdom of Swaziland

Ruler: Mswati III

Currency:

(1974—2018)

Demonetization: 1 February 2016

Material

References

KM: #Click to copy to clipboard45

Numista: #2273

Value

Exchange value: 1 SZL

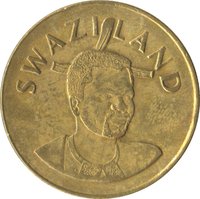

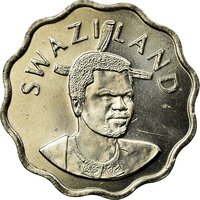

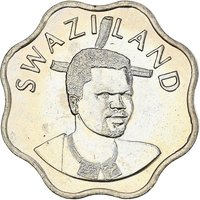

Obverse

Reverse

Edge

Reeded

Mints

| Name | Mark |

|---|---|

| Royal Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1995 | — | — | ||

| 1996 | — | — | ||

| 1998 | — | — | ||

| 2002 | — | — | ||

| 2003 | — | — | ||

| 2005 | — | — | ||

| 2008 | — | — | ||

| 2009 | — | — |

Historical background

In 1995, the Kingdom of Swaziland (renamed Eswatini in 2018) operated under a unique and long-standing monetary arrangement as a member of the Common Monetary Area (CMA) with South Africa, Lesotho, and Namibia. Established in 1986, the CMA effectively pegged the Swazi lilangeni (SZL) at par to the South African rand (ZAR), which circulated freely within the kingdom alongside the domestic currency. This meant Swaziland ceded control over its independent monetary policy to the South African Reserve Bank, anchoring its currency stability to the performance and policies of its much larger neighbor.

The year fell within a period of relative macroeconomic stability for Swaziland, but the currency situation was not without its challenges. The fixed parity and free circulation ensured minimal transaction costs with South Africa, its dominant trading partner, which accounted for the vast majority of its imports and exports. However, this also meant Swaziland imported South Africa's inflation and interest rates, limiting its policy tools to respond to domestic economic conditions. Furthermore, the reliance on the rand tied Swaziland's economic fortunes directly to South Africa, which was itself navigating the immediate post-apartheid transition and significant currency volatility in the mid-1990s.

Despite these constraints, the system was largely viewed as necessary and beneficial for Swaziland in 1995. The country lacked the economic mass and foreign reserves to support a credible independent currency, and the CMA provided a stable monetary framework that facilitated trade and investment. The primary focus for Swazi authorities was therefore not on currency reform, but on managing fiscal policy and structural economic issues within the confines of the fixed exchange rate regime, a reality that would define its monetary landscape for decades to come.

The year fell within a period of relative macroeconomic stability for Swaziland, but the currency situation was not without its challenges. The fixed parity and free circulation ensured minimal transaction costs with South Africa, its dominant trading partner, which accounted for the vast majority of its imports and exports. However, this also meant Swaziland imported South Africa's inflation and interest rates, limiting its policy tools to respond to domestic economic conditions. Furthermore, the reliance on the rand tied Swaziland's economic fortunes directly to South Africa, which was itself navigating the immediate post-apartheid transition and significant currency volatility in the mid-1990s.

Despite these constraints, the system was largely viewed as necessary and beneficial for Swaziland in 1995. The country lacked the economic mass and foreign reserves to support a credible independent currency, and the CMA provided a stable monetary framework that facilitated trade and investment. The primary focus for Swazi authorities was therefore not on currency reform, but on managing fiscal policy and structural economic issues within the confines of the fixed exchange rate regime, a reality that would define its monetary landscape for decades to come.

🌱 Very Common