1 Sovereign – United Kingdom

United Kingdom

Context

Years: 1911–1919

Issuer: United Kingdom

Ruler: George V

Currency:

(1158—1970)

Total mintage: 582,947

Material

References

Numista: #22059

Value

Bullion value: $1224.24

Obverse

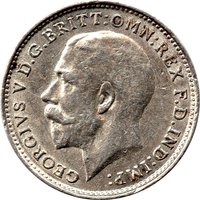

Description:

Uncrowned portrait of King George V left, circular legend.

Inscription:

GEORGIVS V D.G.BRITT:OMN:REX F.D.IND:IMP:

Translation:

George V, by the Grace of God, King of all the Britains, Defender of the Faith, Emperor of India.

Script: Latin

Language: Latin

Engraver: Edgar Bertram MacKennal

Reverse

Description:

St. George slaying the dragon. Date and engraver's initials in exergue; C mintmark under horse's rear hoof.

Inscription:

1917

B.P.

B.P.

Script: Latin

Engraver: Benedetto Pistrucci

Edge

Reeded

Categories

| Mythology> Fantastic animal |

| Animal> Horse |

Mints

| Name | Mark |

|---|---|

| Royal Canadian Mint of Ottawa | C |

Mintings

Historical background

In 1911, the United Kingdom operated under the classical Gold Standard, a system where the value of the pound sterling was directly convertible into a fixed quantity of gold. This framework, formally established in 1816 and solidified by the Bank Charter Act of 1844, ensured price stability and made London the undisputed centre of global finance. The currency in circulation consisted of gold sovereigns and half-sovereigns for larger transactions, alongside Bank of England notes, which were effectively "promises to pay" the bearer in gold upon demand. The system was deeply orthodox and enjoyed widespread confidence, underpinning both domestic economic stability and Britain's vast international trade and investment.

However, the monetary landscape was not without its tensions. While the Gold Standard provided long-term stability, it could also impose harsh short-term adjustments. The Bank of England managed the currency with the primary goal of maintaining gold reserves, often raising interest rates to attract gold inflows during periods of deficit. This could stifle domestic investment and exacerbate unemployment during economic downturns, a trade-off that was beginning to attract criticism from emerging social and political movements. Furthermore, the reliance on physical gold coinage was increasingly seen as somewhat anachronistic for a modern industrial economy, with growing use of cheques and bank deposits for everyday business.

The year 1911 itself was one of calm within this established system, but it stood on the precipice of profound change. The political and social unrest of the period, including severe industrial disputes, did not directly threaten the currency's integrity. Yet, the underlying pressures of maintaining gold convertibility amidst rising global competition and domestic social welfare demands were mounting. Within three years, the outbreak of the First World War in 1914 would force the UK to suspend the Gold Standard, ending this era of monetary orthodoxy and setting the stage for a century of financial transformation. The currency situation in 1911, therefore, represents the final chapter of a venerable but rigid system soon to be shattered by the forces of the modern world.

However, the monetary landscape was not without its tensions. While the Gold Standard provided long-term stability, it could also impose harsh short-term adjustments. The Bank of England managed the currency with the primary goal of maintaining gold reserves, often raising interest rates to attract gold inflows during periods of deficit. This could stifle domestic investment and exacerbate unemployment during economic downturns, a trade-off that was beginning to attract criticism from emerging social and political movements. Furthermore, the reliance on physical gold coinage was increasingly seen as somewhat anachronistic for a modern industrial economy, with growing use of cheques and bank deposits for everyday business.

The year 1911 itself was one of calm within this established system, but it stood on the precipice of profound change. The political and social unrest of the period, including severe industrial disputes, did not directly threaten the currency's integrity. Yet, the underlying pressures of maintaining gold convertibility amidst rising global competition and domestic social welfare demands were mounting. Within three years, the outbreak of the First World War in 1914 would force the UK to suspend the Gold Standard, ending this era of monetary orthodoxy and setting the stage for a century of financial transformation. The currency situation in 1911, therefore, represents the final chapter of a venerable but rigid system soon to be shattered by the forces of the modern world.

🌟 Limited