10 kroner (Ole Bull) – Norway

Add to wishlist

Circulating commemorative coins

Commemoration: Ole Bull 200 years

Norway

Context

Material

References

KM: #

Numista: #10941

Value

Exchange value: 10 NOK

Inflation-adjusted value: 15.12 NOK

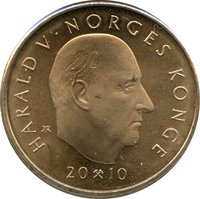

Obverse

Description:

King Harald V bust facing right. Engraver's initials behind bust. Inscription surrounds. Date split by mintmark below. Solid rim ring.

Inscription:

HARALD V · NORGES KONGE

IAR

20 ⚒ 10

IAR

20 ⚒ 10

Translation:

Harald V, Norway's King

20th Anniversary

20 · 10

20th Anniversary

20 · 10

Script: Latin

Engraver: Ingrid Austlid Rise

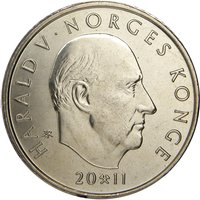

Reverse

Description:

Ole Bull’s portrait merges with his composition ”Seterjentens Søndag.” His name, the anniversary year, and denomination appear to the right, with the designer’s initials below. A solid ring encircles the rim.

Inscription:

OLE

BULL

200

ÅR

10 kr

BULL

200

ÅR

10 kr

Translation:

Ole

Bull

200

Years

10 kr

Bull

200

Years

10 kr

Script: Latin

Engraver: Ingrid Austlid Rise

Designer: Wenche Gulbransen

Edge

Segmented reeding.

Categories

| Art> Music |

| Event> Birth anniversary |

Mints

| Name | Mark |

|---|---|

| Norwegian Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2010 | — | 953,251 | ||

| 2010 | — | 1,673 | BU | |

| 2010 | — | 4,619 | Proof |

Historical background

In 2010, Norway's currency situation was characterized by the strength and stability of the Norwegian krone (NOK), heavily influenced by the country's robust petroleum sector. As a major oil and gas exporter, Norway benefited from high global oil prices, which averaged around $80 per barrel that year. This drove significant export revenues and foreign investment, creating sustained demand for the krone and keeping it strong against major currencies like the euro and the US dollar. This strength was a double-edged sword, bolstering national wealth but also posing challenges for non-oil exporters, whose goods became more expensive on the international market.

Domestically, Norway's economy had weathered the 2008-2009 global financial crisis better than most developed nations, thanks to its substantial sovereign wealth fund (the Government Pension Fund Global) and prudent fiscal policies. With low unemployment and solid growth, Norges Bank, the central bank, began a tightening cycle in 2010, raising its key policy rate from a historic low of 1.25% in January to 2.0% by December. These interest rate hikes, aimed at curbing domestic financial imbalances and inflation, further attracted foreign capital and contributed to the krone's appreciation.

The primary policy focus regarding the currency was managing its strength and the resulting economic imbalances. Authorities were cautious not to let the krone's appreciation hurt the competitiveness of traditional industries like manufacturing and fisheries. While there was no direct intervention to weaken the krone, Norges Bank's rate decisions carefully considered the exchange rate's impact. The overall situation in 0 was one of a commodity-driven, strong currency within a resilient and growing economy, setting the stage for continued debates about diversification and long-term economic structure beyond oil.

Domestically, Norway's economy had weathered the 2008-2009 global financial crisis better than most developed nations, thanks to its substantial sovereign wealth fund (the Government Pension Fund Global) and prudent fiscal policies. With low unemployment and solid growth, Norges Bank, the central bank, began a tightening cycle in 2010, raising its key policy rate from a historic low of 1.25% in January to 2.0% by December. These interest rate hikes, aimed at curbing domestic financial imbalances and inflation, further attracted foreign capital and contributed to the krone's appreciation.

The primary policy focus regarding the currency was managing its strength and the resulting economic imbalances. Authorities were cautious not to let the krone's appreciation hurt the competitiveness of traditional industries like manufacturing and fisheries. While there was no direct intervention to weaken the krone, Norges Bank's rate decisions carefully considered the exchange rate's impact. The overall situation in 0 was one of a commodity-driven, strong currency within a resilient and growing economy, setting the stage for continued debates about diversification and long-term economic structure beyond oil.

🌱 Common