1000 yuan – People's Republic of China

Add to wishlist

Non-circulating coins

Series: Panda Bullion

China

Context

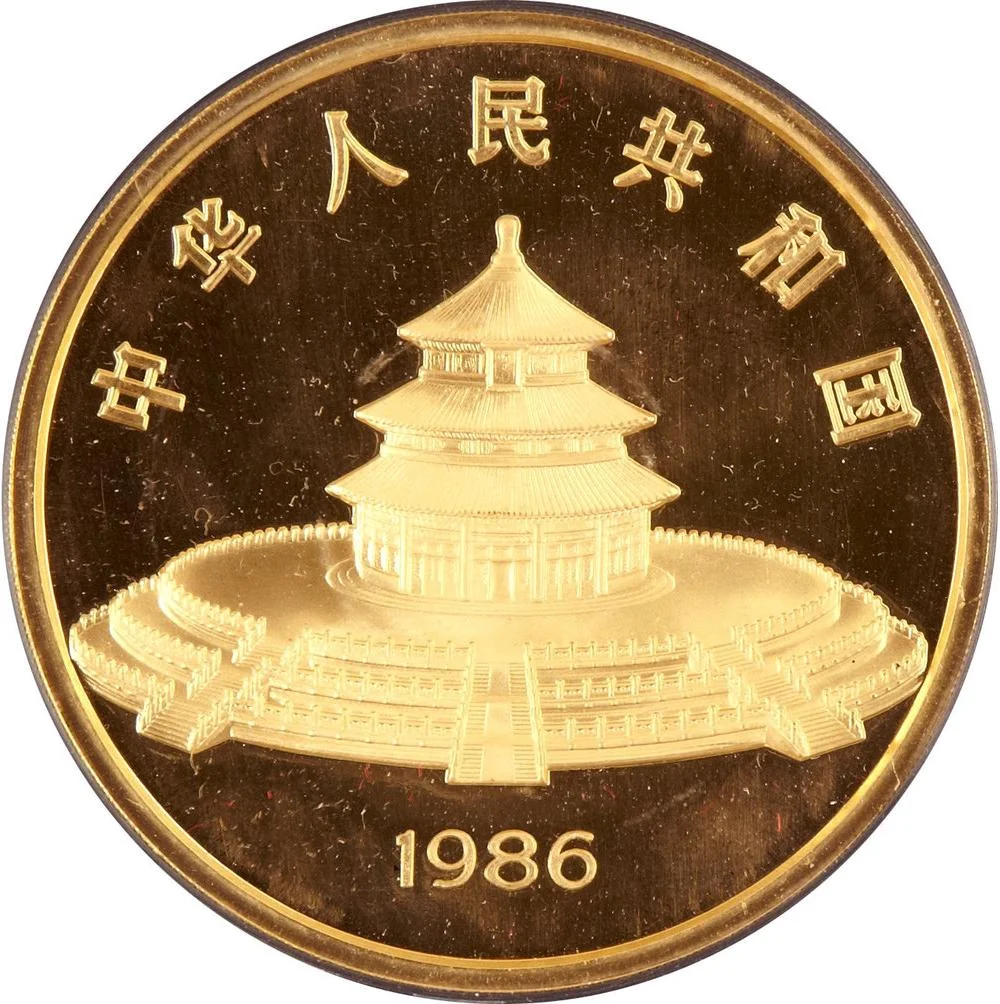

Year: 1986

Country: China

Issuer: People's Republic of China

Period:

(since 1949)

Currency:

(since 1955)

Total mintage: 2

Material

References

KM: #

Numista: #17599

Value

Exchange value: 1000 CNY

Bullion value: $56845.59

Obverse

Edge

Reeded

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1986 | — | 2 | Proof |

Historical background

In 1986, the People's Republic of China was navigating a critical phase of its economic reform program initiated under Deng Xiaoping. The currency, the Renminbi (RMB), operated under a complex dual-track system. Officially, it was pegged to a basket of currencies at a strong, overvalued rate for state-planned transactions. However, a parallel and vibrant foreign exchange certificate (FEC) system and a burgeoning black market existed for most practical trade and personal use, where the RMB traded at a much weaker, market-influenced rate. This disconnect reflected the tension between a receding command economy and the forces of liberalization and foreign investment the reforms sought to attract.

The primary economic focus was on controlling inflation and managing the trade balance, rather than making the RMB a convertible currency. The overvalued official rate subsidized imports of crucial machinery and technology for modernization but hurt export competitiveness. To address this, China had established "swap centres" in special economic zones like Shenzhen, where enterprises could trade foreign exchange at negotiated rates closer to market value. This year was part of a gradual, controlled experiment in moving toward a more realistic exchange rate, but full convertibility was deemed too risky for the still-fragile economic system.

Overall, the 1986 currency situation was characterized by managed inconsistency. It was a transitional tool, deliberately distorting prices to protect and guide domestic industries while cautiously opening a window to global market forces. The arrangements were cumbersome and fostered arbitrage, but they served the broader strategic goal of shielding the vast domestic economy from external shocks while selectively integrating with global trade, setting the stage for the more unified exchange rate reforms that would follow in the early 1990s.

The primary economic focus was on controlling inflation and managing the trade balance, rather than making the RMB a convertible currency. The overvalued official rate subsidized imports of crucial machinery and technology for modernization but hurt export competitiveness. To address this, China had established "swap centres" in special economic zones like Shenzhen, where enterprises could trade foreign exchange at negotiated rates closer to market value. This year was part of a gradual, controlled experiment in moving toward a more realistic exchange rate, but full convertibility was deemed too risky for the still-fragile economic system.

Overall, the 1986 currency situation was characterized by managed inconsistency. It was a transitional tool, deliberately distorting prices to protect and guide domestic industries while cautiously opening a window to global market forces. The arrangements were cumbersome and fostered arbitrage, but they served the broader strategic goal of shielding the vast domestic economy from external shocks while selectively integrating with global trade, setting the stage for the more unified exchange rate reforms that would follow in the early 1990s.

Series: Panda Bullion

✨ Legendary