20 kroner – Norway

Add to wishlist

Circulating commemorative coins

Commemoration: Year 2000

Norway

Context

Material

References

KM: #

Numista: #10675

Value

Exchange value: 20 NOK

Inflation-adjusted value: 37.16 NOK

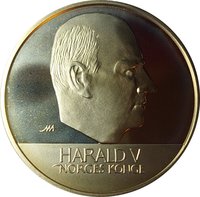

Obverse

Description:

Bust of King Harald V facing right, encircled by inscription. Mintmark and mintmaster's initials below. Solid rim ring.

Inscription:

HARALD V · NORGES KONGE

⚒ JEJ

⚒ JEJ

Translation:

Harald V, Norway's King

By the Grace of God

By the Grace of God

Script: Latin

Engraver: Marit Wiklund

Reverse

Description:

Road to unknown landscape. Value and date in three lines. Engraver's initials at right. Solid rim ring.

Inscription:

20

KRONER

ÅR 2000

MW

KRONER

ÅR 2000

MW

Translation:

20 Kroner Year 2000 MW

Script: Latin

Engraver: Marit Wiklund

Edge

Plain

Mints

| Name | Mark |

|---|---|

| Norwegian Mint | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2000 | — | 1,032,307 | ||

| 2000 | — | 13,000 | Proof | |

| 2000 | — | 10,000 | BU |

Historical background

In the year 2000, Norway's currency situation was characterized by a managed float of the Norwegian krone (NOK) within a defined bandwidth. Following the collapse of a fixed exchange rate regime in 1992, Norges Bank had adopted an inflation-targeting framework in March 2001, but the transitional period around the turn of the millennium still saw the central bank actively using interest rates to stabilize the krone's value. The primary policy tool was a "currency regulation" system, where Norges Bank aimed to keep the krone stable against a trade-weighted basket of currencies, though with less rigidity than a pure peg.

The period was heavily influenced by Norway's status as a major oil and gas exporter. High global oil prices in 2000, driven by strong demand, bolstered the country's trade surplus and fiscal revenues, which in theory should have strengthened the krone. However, the currency also faced significant downward pressure at times due to large capital outflows. Norwegian investors and institutions were actively diversifying into foreign assets, particularly European equities and bonds, a trend that accelerated following the domestic pension fund reform of the late 1990s. This created a dynamic where petrodollar inflows and private-sector outflows often offset each other.

Ultimately, Norges Bank's focus was shifting from direct exchange rate management to controlling domestic inflation, a transition formally cemented the following year. In 2000, however, the bank still intervened in foreign exchange markets to smooth excessive volatility. The key challenge was balancing the inflationary risks from a strong krone (which made imports cheaper) against the need to maintain competitiveness for non-oil exports. This delicate balancing act set the stage for the pure inflation-targeting regime that would define Norwegian monetary policy in the decades to come.

The period was heavily influenced by Norway's status as a major oil and gas exporter. High global oil prices in 2000, driven by strong demand, bolstered the country's trade surplus and fiscal revenues, which in theory should have strengthened the krone. However, the currency also faced significant downward pressure at times due to large capital outflows. Norwegian investors and institutions were actively diversifying into foreign assets, particularly European equities and bonds, a trend that accelerated following the domestic pension fund reform of the late 1990s. This created a dynamic where petrodollar inflows and private-sector outflows often offset each other.

Ultimately, Norges Bank's focus was shifting from direct exchange rate management to controlling domestic inflation, a transition formally cemented the following year. In 2000, however, the bank still intervened in foreign exchange markets to smooth excessive volatility. The key challenge was balancing the inflationary risks from a strong krone (which made imports cheaper) against the need to maintain competitiveness for non-oil exports. This delicate balancing act set the stage for the pure inflation-targeting regime that would define Norwegian monetary policy in the decades to come.

🌱 Fairly Common