20 kroner (Leif Ericson in North America) – Norway

Add to wishlist

Circulating commemorative coins

Commemoration: 1000th anniversary of Leif Ericson in North America

Norway

Context

Material

References

KM: #

Numista: #9779

Value

Exchange value: 20 NOK

Inflation-adjusted value: 38.04 NOK

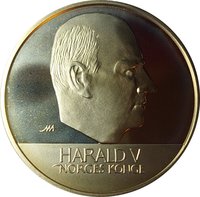

Obverse

Reverse

Description:

Ancient Viking longship, half boat design. Left: value and date. Right: three-line inscription. Bottom right: mintmark and initial. Solid rim ring.

Inscription:

20

KRONER

1999

MOT

UKJENT

LAND

⚒ JEJ

KRONER

1999

MOT

UKJENT

LAND

⚒ JEJ

Translation:

20 KRONER

1999

TOWARDS UNKNOWN LAND

⚒ JEJ

1999

TOWARDS UNKNOWN LAND

⚒ JEJ

Script: Latin

Language: Norwegian

Engraver: Nils Aas

Edge

Plain

Categories

| Transportation> Watercraft |

Mints

| Name | Mark |

|---|---|

| Norwegian Mint | — |

| Royal Canadian Mint of Ottawa | ⚒ |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 1999 | — | 1,048,700 | ||

| 1999 | — | 26,000 | BU | |

| 1999 | — | 2,500 | Proof |

Historical background

In 1999, Norway found itself in a unique and deliberate position regarding currency, as it was one of the few Western European nations outside the newly launched Eurozone. While its neighbours Sweden and Denmark also remained outside, Norway's situation was distinct due to its status as a non-EU member following the 1994 referendum. The country's economic policy was firmly anchored by the Norwegian krone (NOK) operating within a managed float exchange rate regime, overseen by Norges Bank. The primary objective was not to target a specific fixed rate but to maintain low and stable inflation, a framework that provided flexibility to manage the economic shocks inherent to its significant oil and gas exports.

The year was dominated by active management of the krone in the face of considerable volatility, largely driven by fluctuating global oil prices. After a sharp decline in oil prices in 1998, 1999 saw a strong recovery, which typically would lead to a stronger krone. However, Norges Bank intervened in the foreign exchange market on several occasions, selling kroner to prevent excessive appreciation that could harm the non-oil export sector. This period underscored the central challenge of balancing the wealth generated from petroleum resources with the need to maintain competitiveness for mainland industries, a duality often referred to as the "Dutch disease" concern.

Ultimately, the events of 1999 reinforced Norway's consensus to retain its independent monetary policy and its national currency. The krone regime allowed Norges Bank to tailor interest rates and interventions specifically to Norway's cyclical conditions, which were often out of sync with the Eurozone due to the oil sector's influence. This independent path, coupled with the sovereign wealth fund (the Government Pension Fund Global) established just a few years prior, was seen as the optimal toolkit for managing the nation's petroleum wealth without sacrificing economic stability, a stance that has remained fundamentally unchanged since.

The year was dominated by active management of the krone in the face of considerable volatility, largely driven by fluctuating global oil prices. After a sharp decline in oil prices in 1998, 1999 saw a strong recovery, which typically would lead to a stronger krone. However, Norges Bank intervened in the foreign exchange market on several occasions, selling kroner to prevent excessive appreciation that could harm the non-oil export sector. This period underscored the central challenge of balancing the wealth generated from petroleum resources with the need to maintain competitiveness for mainland industries, a duality often referred to as the "Dutch disease" concern.

Ultimately, the events of 1999 reinforced Norway's consensus to retain its independent monetary policy and its national currency. The krone regime allowed Norges Bank to tailor interest rates and interventions specifically to Norway's cyclical conditions, which were often out of sync with the Eurozone due to the oil sector's influence. This independent path, coupled with the sovereign wealth fund (the Government Pension Fund Global) established just a few years prior, was seen as the optimal toolkit for managing the nation's petroleum wealth without sacrificing economic stability, a stance that has remained fundamentally unchanged since.

🌱 Fairly Common