1 Balboa – Panama

Circulating commemorative coins

Commemoration: Handover of the Canal by the US to the Panamenian government.

Panama

Context

Material

Diameter: 38.1 mm

Weight: 22.68 g

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #Click to copy to clipboard134

Numista: #16642

Value

Exchange value: 1 PAB

Obverse

Description:

Bust left of President Mireya Moscoso, flanked by her presidency dates and value, with legend around.

Inscription:

MIREYA MOSCOSO

1

UN BALBOA 22.68 gr.

1999 2004

PRESIDENTA DE PANAMA

1

UN BALBOA 22.68 gr.

1999 2004

PRESIDENTA DE PANAMA

Translation:

MIREYA MOSCOSO

1

ONE BALBOA 22.68 gr.

1999 2004

PRESIDENT OF PANAMA

1

ONE BALBOA 22.68 gr.

1999 2004

PRESIDENT OF PANAMA

Script: Latin

Language: Spanish

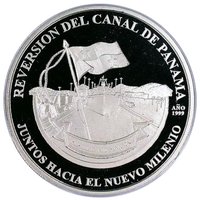

Reverse

Description:

Panamanian flag over a canal lock with a ship, encircled by legend.

Inscription:

REVERSION DEL CANAL DE PANAMA

AÑO

1999

REPUBLICA DE PANAMA

JUNTOS HACIA EL NUEVO MILENIO

AÑO

1999

REPUBLICA DE PANAMA

JUNTOS HACIA EL NUEVO MILENIO

Translation:

REVERSION OF THE PANAMA CANAL

YEAR

1999

REPUBLIC OF PANAMA

TOGETHER TOWARDS THE NEW MILLENNIUM

YEAR

1999

REPUBLIC OF PANAMA

TOGETHER TOWARDS THE NEW MILLENNIUM

Script: Latin

Language: Spanish

Edge

Reeded

Categories

| Transportation> Watercraft |

| Event> Treaty |

| Person> Politician |

| Symbol> Flag |

Mints

| Name | Mark |

|---|---|

| Royal Canadian Mint of Winnipeg | — |

Mintings

| Year | Mint Mark | Mintage | Quality | Collection |

|---|---|---|---|---|

| 2004 | — | 348,000 | ||

| 2004 | — | 2,000 | Proof |

Historical background

Panama's currency situation in 2004 was defined by its unique and long-standing monetary framework, which remained a cornerstone of its economic stability. Since 1904, the country has used the US dollar as its official legal tender, a system known as full dollarization. The Panamanian balboa existed only as a fractional coinage, pegged at a 1:1 parity with the dollar, with no paper balboa notes in circulation. This arrangement provided low inflation, eliminated exchange rate risk, and facilitated international trade and investment, which were vital for the Panama Canal and the large services sector.

The year 2004 fell within a period of steady economic growth following the full transfer of the Panama Canal from the United States at the end of 1999. The dollarized system provided macroeconomic stability, with inflation rates closely mirroring those of the United States. However, this framework also meant Panama relinquished control over its independent monetary policy; it could not print money or set interest rates to respond to domestic economic cycles. The country's financial stability was therefore heavily dependent on maintaining fiscal discipline and a robust banking sector, as it could not act as a lender of last resort in a traditional sense.

While generally viewed positively for its stability, dollarization was not without ongoing debates. Critics pointed to the loss of seigniorage revenue and the inability to devalue the currency to boost competitiveness. In 2004, these discussions were largely academic, as there was no serious political movement to abandon the system. The economy was performing well, and the dollar's role was deeply entrenched, providing a predictable environment for the significant foreign investment flowing into the country, particularly into the Canal expansion plans that were then in the advanced stages of approval.

The year 2004 fell within a period of steady economic growth following the full transfer of the Panama Canal from the United States at the end of 1999. The dollarized system provided macroeconomic stability, with inflation rates closely mirroring those of the United States. However, this framework also meant Panama relinquished control over its independent monetary policy; it could not print money or set interest rates to respond to domestic economic cycles. The country's financial stability was therefore heavily dependent on maintaining fiscal discipline and a robust banking sector, as it could not act as a lender of last resort in a traditional sense.

While generally viewed positively for its stability, dollarization was not without ongoing debates. Critics pointed to the loss of seigniorage revenue and the inability to devalue the currency to boost competitiveness. In 2004, these discussions were largely academic, as there was no serious political movement to abandon the system. The economy was performing well, and the dollar's role was deeply entrenched, providing a predictable environment for the significant foreign investment flowing into the country, particularly into the Canal expansion plans that were then in the advanced stages of approval.

🌱 Fairly Common