5 centavos – Philippines

Add to wishlist

Philippines

Context

Years: 1937–1941

Issuer: Philippines

Period:

(1935—1946)

Currency:

(1857—1967)

Demonetized: Yes

Total mintage: 9,244,000

Material

Diameter: 19.1 mm

Weight: 4.8 g

Thickness: 2 mm

Shape: Round

Composition: Copper-nickel

Technique: Milled

Alignment: Coin alignment

flip

References

KM: #

Numista: #16638

Obverse

Description:

Man seated with hammer and anvil, volcano smoking at right.

Inscription:

FIVE CENTAVOS

FILIPINAS

FILIPINAS

Translation:

FIVE CENTAVOS

PHILIPPINES

PHILIPPINES

Script: Latin

Designer: Ambrosia Morales

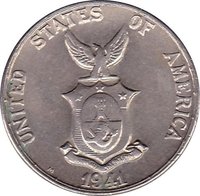

Reverse

Description:

Philippine coat of arms.

Inscription:

UNITED STATES OF AMERICA

COMMONWEALTH OF THE PHILIPPINES

1941

M

COMMONWEALTH OF THE PHILIPPINES

1941

M

Script: Latin

Designers: Melicio Figueroa, Charles Barber

Edge

Plain

Categories

| Geography> Mountain |

| Symbols> Coat of Arms |

Mints

| Name | Mark |

|---|---|

| Manila | M |

Historical background

In 1937, the currency situation in the Philippines was defined by its transitional status under the American colonial administration, operating under the Philippine Coinage Act of 1903. The official currency was the Philippine peso (or piso), which was pegged at a fixed rate of 2:1 to the United States dollar. This meant one US dollar was equivalent to two Philippine pesos, a stable but deliberately undervalued peg designed to closely integrate the islands' economy with that of the mainland U.S. and facilitate trade. The currency was issued by the Philippine Treasury and backed by a 100% gold reserve held in the United States, ensuring full convertibility and significant monetary stability.

This system provided notable benefits, including low inflation and a predictable environment for the dominant export industries like sugar, coconut, and abaca. However, the peg also created structural economic tensions. The fixed exchange rate made Philippine exports cheap for American buyers but made imports from non-dollar countries more expensive. Furthermore, monetary policy was entirely subservient to the needs of the U.S. economy, with the Philippines having no independent mechanism to adjust its money supply or interest rates in response to local economic conditions. Critics argued this stifled industrial diversification and kept the economy in a colonial pattern of agricultural commodity exports.

The year 1937 fell within a period of active political debate about the nation's monetary future, as the Philippines was in the final phase of a ten-year Commonwealth transition toward scheduled independence in 1946. A key economic issue was whether to maintain the dollar peg after independence or to establish a central bank and a more autonomous monetary system. This discussion would culminate in the recommendations of the Joint Preparatory Committee on Philippine Affairs in 1938 and eventually lead to the creation of the Central Bank of the Philippines in 1949, marking the end of the currency regime as it stood in 1937.

This system provided notable benefits, including low inflation and a predictable environment for the dominant export industries like sugar, coconut, and abaca. However, the peg also created structural economic tensions. The fixed exchange rate made Philippine exports cheap for American buyers but made imports from non-dollar countries more expensive. Furthermore, monetary policy was entirely subservient to the needs of the U.S. economy, with the Philippines having no independent mechanism to adjust its money supply or interest rates in response to local economic conditions. Critics argued this stifled industrial diversification and kept the economy in a colonial pattern of agricultural commodity exports.

The year 1937 fell within a period of active political debate about the nation's monetary future, as the Philippines was in the final phase of a ten-year Commonwealth transition toward scheduled independence in 1946. A key economic issue was whether to maintain the dollar peg after independence or to establish a central bank and a more autonomous monetary system. This discussion would culminate in the recommendations of the Joint Preparatory Committee on Philippine Affairs in 1938 and eventually lead to the creation of the Central Bank of the Philippines in 1949, marking the end of the currency regime as it stood in 1937.

Series: 1937 series

🌱 Common